This note was originally published at 8am on January 31, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“How soon ‘not now’ becomes never.”

-Martin Luther

Don’t worry, I’m not going to go off on the Protestant Reformation of 16thcentury Europe this morning. I’m going to give some much simpler advice re: chasing any asset price higher today – Not Now. Most things will get marked-up into month-end.

That’s not to say I didn’t think yesterday at 9:51 AM wasn’t a good time to buy. With the SP500 testing 1301 (down 32 points, or -2.4% from last Thursday morning’s 1333 high), that’s where I bought Energy (XLE), taking my Cash position down from 91% to 85% and taking up my US Equity position in the Hedgeye Asset Allocation Model from 0% to 6%.

Some people get all fired-up about this whole TimeStamping thing we do. It’s really nothing to get emotional about. It’s just what we do. We like to make calls and be held accountable to the timing of those calls. We call it the score.

Back to the Global Macro Grind…

These German dudes and dudettes have to be right fired-up this morning. In the face of the entire world begging them to bail out the dysfunctional; and after watching the American media chastise them for not being able to do the “right thing” – they just kept saying Not Now to just about everyone who no longer needs Luther’s Latin translation for the word never.

How is the economic model of German fiscal conservatism scoring? Here it is, head-to-head, versus Italy:

- Germany Unemployment = 6.7% JAN vs 6.8% DEC = 20-year low

- Italy Unemployment = 8.9% JAN vs 8.8% DEC = 8-year high

What’s in your wallet?

Again and again and again, we’ve tried to remind our audience that the strength of a country is not explicitly reflected by the daily moves of her stock market. Ask the Germans who lived through a 1920s stock market hyper-inflation about that.

If you don’t have a policy to fear-monger your citizenry into believing that saving is evil, you might just build a national confidence and pride that reflexively equates to more stable employment and consumption.

In the US, we’re getting closer to figuring this out. Or are we? Romney’s monetarily conservative message seems to be picking up some momentum in Florida and, at the same time, it still looks like President Obama can change fiscally.

Yes We Can. But will he?

Instead of being politically polarized by the debate, I think the world’s vote on this will continue to be on the tape each and every day, ticking, via the sequential momentum in the US Dollar Index.

If you haven’t noticed, in the last few weeks, the US Dollar has lost a statistically significant amount of momentum:

- US Dollar Index = down -3.1% since its intermediate-term top of $81.53 in mid-January 2012

- US Dollar Index = up +8.2% since testing a 40-year low during the thralls of Qe2’s policy to inflate (April 2011)

To be crystal clear on this, the correlation to asset prices between the US Dollar Index and everything else in Global Macro right now is unclear.

In sharp contrast to April 2011, when the inverse correlation between US stocks and the USD was tracking in the -0.8-0.9 range, today’s 120-day correlation is actually a positive +0.44 and US Equity Volatility (VIX) has an inverse correlation to USD of -0.59.

In other words, before The Bernank Tax last week, the Fed was out of the way and we saw a stabilization/strengthening of the US Dollar over the course of the last 3-6 months that:

A) firmed up US Confidence, Employment, and Consumption (71% of GDP)

B) started to tone down one of the biggest risks to returns in any business – expected price volatility

American Progress by simply having Bernanke and Geithner out of the way – fancy that. Americans were/are getting it done without the heavy hand of government help. No matter what your politics, that’s just good.

What would not be good for the US economy or stock market (again, two very different things) would be a breakdown in the US Dollar Index of $78.03 intermediate-term TREND support and a breakout in US Equity Volatility (VIX) above TRADE line resistance of 20.86. That would really fire up the price of oil. Copper is already up +12.5% YTD!

Not Good. Not Now.

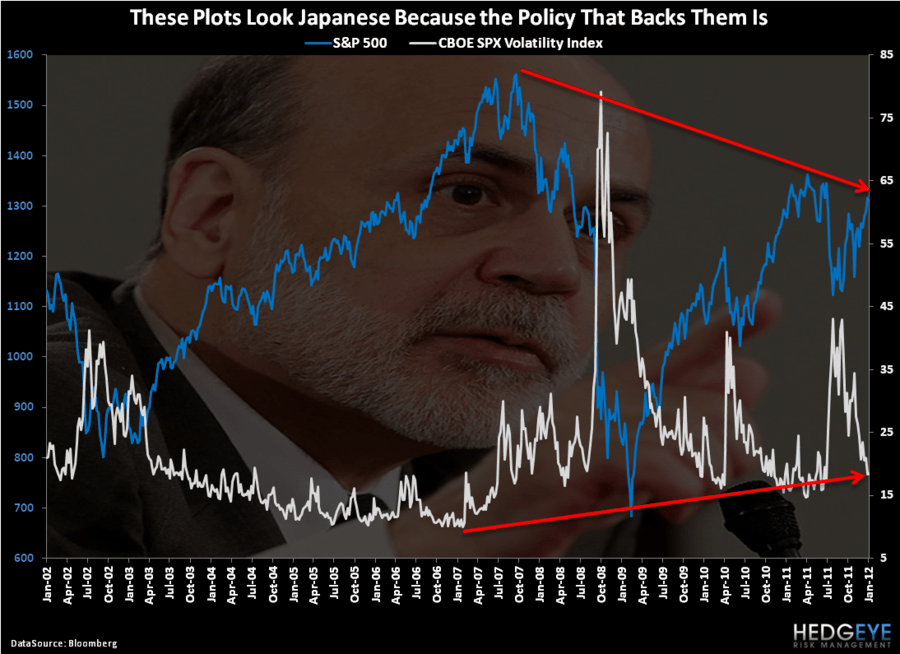

As you can see in the long-term chart of US Stocks (SPX) vs Equity Volatility (VIX):

- The SP500 is making a series of lower long-term highs

- The VIX is making a series of higher long-term lows

The charts look Japanese because the long-term Bush/Obama Keynesian Policies have been. That chart also summarizes the societal American Zeitgeist about markets and the central planners infecting them.

Is President Obama prepared to tell Ben Bernanke to get out of the way and let American Savers earn a rate of return on their fixed incomes? Not Now. While hope is not a risk management process, I can only pray that doesn’t mean never.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, US Dollar Index, German DAX, and the SP500 are now $1691-1751, $110.61-111.89, $1.30-1.32, $78.70-79.75, 6456-6503, and 1306-1324, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer