We feel even better about our long-term positive thesis after the Q.

We will have a more detailed note out when we are done with the model. As you know, BYI is one of our favorite long-term and intermediate names. However, had we known the quarter was going to be this good we would have been on the trading side of this call too. Shame on me. However, the quarter did provide us with comfort on our longer term thesis. Certainly, more comfort than we thought.

Here are some comments from our slot expert, Anna Massion:

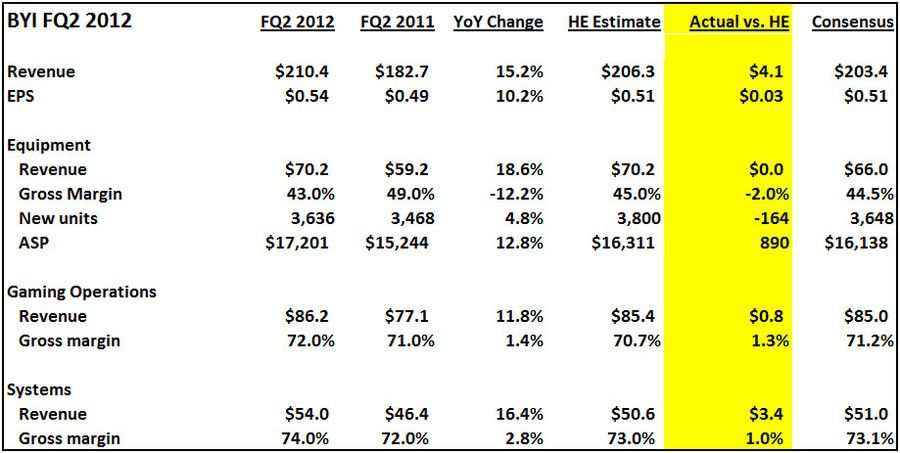

- It was a good quarter. New unit sales were as expected but ASPs were better and margins lower.

- Their ship share was 17% - including WMS’s deferred units (which were not immaterial – but we look at ship share on a what’s shipped basis). Even so, that 17% is a 2% QoQ improvement and a 3% YoY improvement.

- Systems and Game ops were just better than expected and will continue to improve in the coming quarters

- While Italy continues to disappoint, that will be more than offset by early shipments to Scotia Downs

- Our projections don’t even include the other 5 Ohio racetracks (8-10k slots) or IL VLTs, so plenty of upside potential.

- Growth in BYI’s WAP install base was better and that’s before Grease and Michael Jackson. We’re not really giving them much credit there either, so more upside potential.

- You can see the impact of gaming ops on the balance sheet with the increase in jackpot liabilities

- Backlog may have grown - an increase in customer deposits while A/R declined.