Claims Tailwind Persists

Weekly initial jobess claims for last week fell 10k WoW to 367k (down 12k after a 2k upward revision to last week’s data). 4-week rolling claims fell 2k to 376k. On a non-seasonally-adjusted basis, reported claims fell 2k WoW to 415k.

This obviously represents continued progress. The big question is whether claims have reached self-reinforcing levels yet. We've chirped endlessly about 375-400k being the threshold that, below which, unemployment begins to fall, which allows autocorrelation to take hold. In other words, falling unemployment inspires confidence which begets further declines in unemployment. This is an extremely powerful force and it's important to understand that its different from the move from 650k to 400k that we've seen from early 2009 through year-end 2011. That move was catalyzed on the back of monetary and fiscal stimulus alone.

As we highlighted last week, the Fed's significant easing last week has thrown cold water on what had been a strengthening US dollar. As our Macro team makes clear daily, a strong dollar is good for America as it makes gas, food and lots of other less perceptible things cheaper for the average American. The opposite of this, inflation, is a tax and markets hate new taxes. So it will be interesting to watch the interplay between self-reinforcing claims and this inflationary tax. For now, claims are trending lower, which bodes well for the Financials on two fronts: credit quality and loan growth.

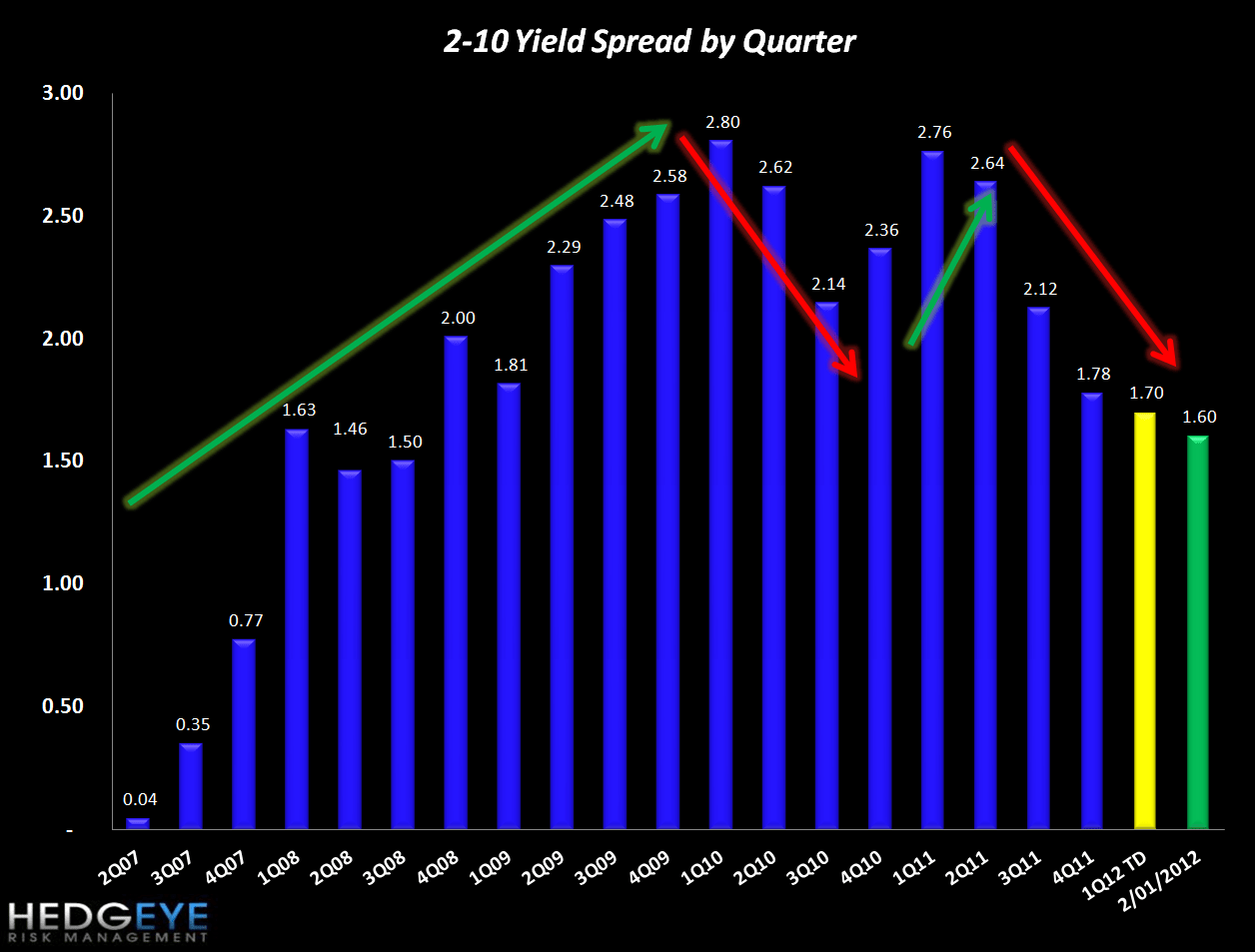

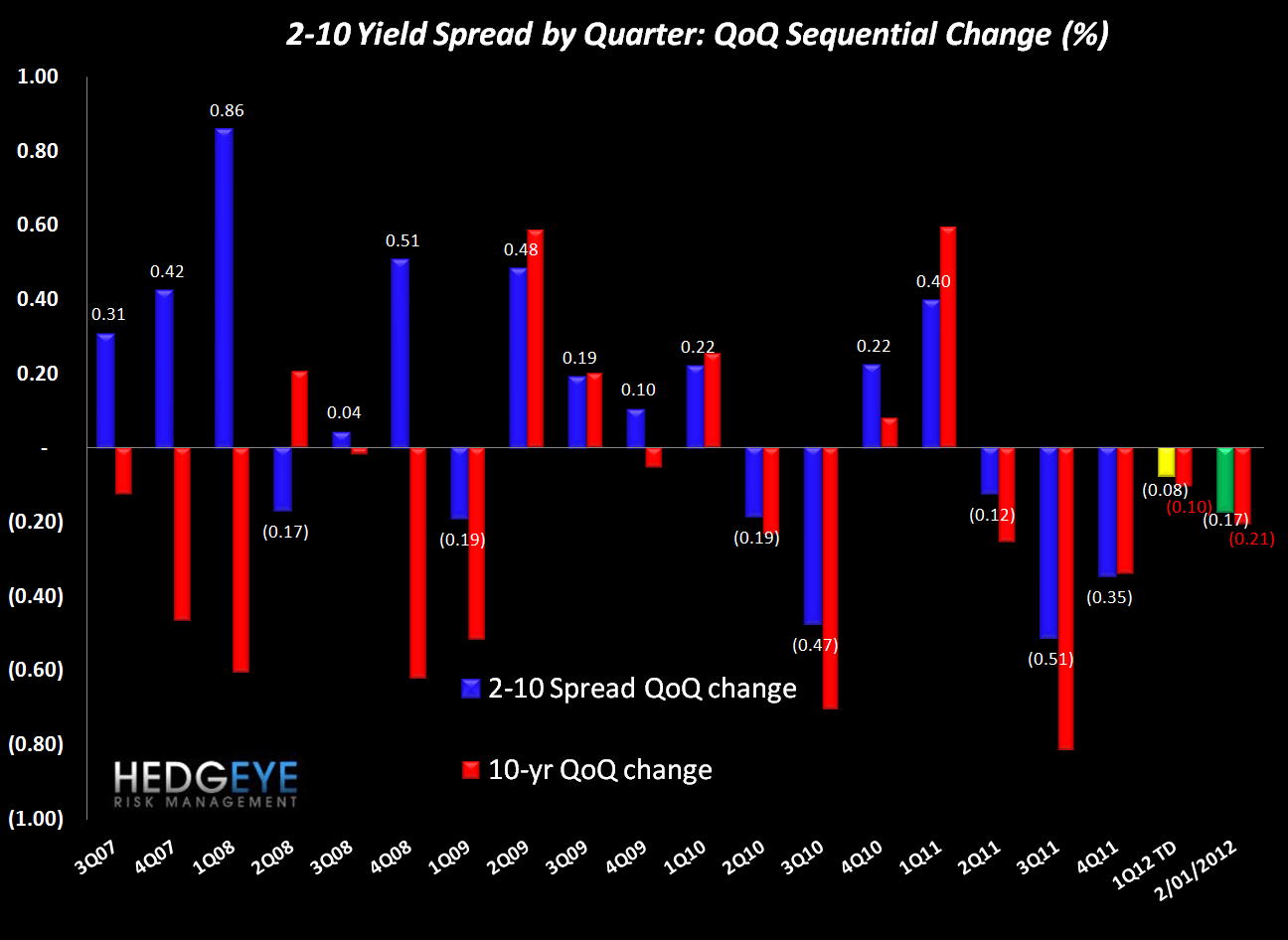

2-10 Spread

The 2-10 spread tightened 17 bps versus last week to 160 bps as of yesterday. The ten-year bond yield also decreased 17 bps to 183 bps.

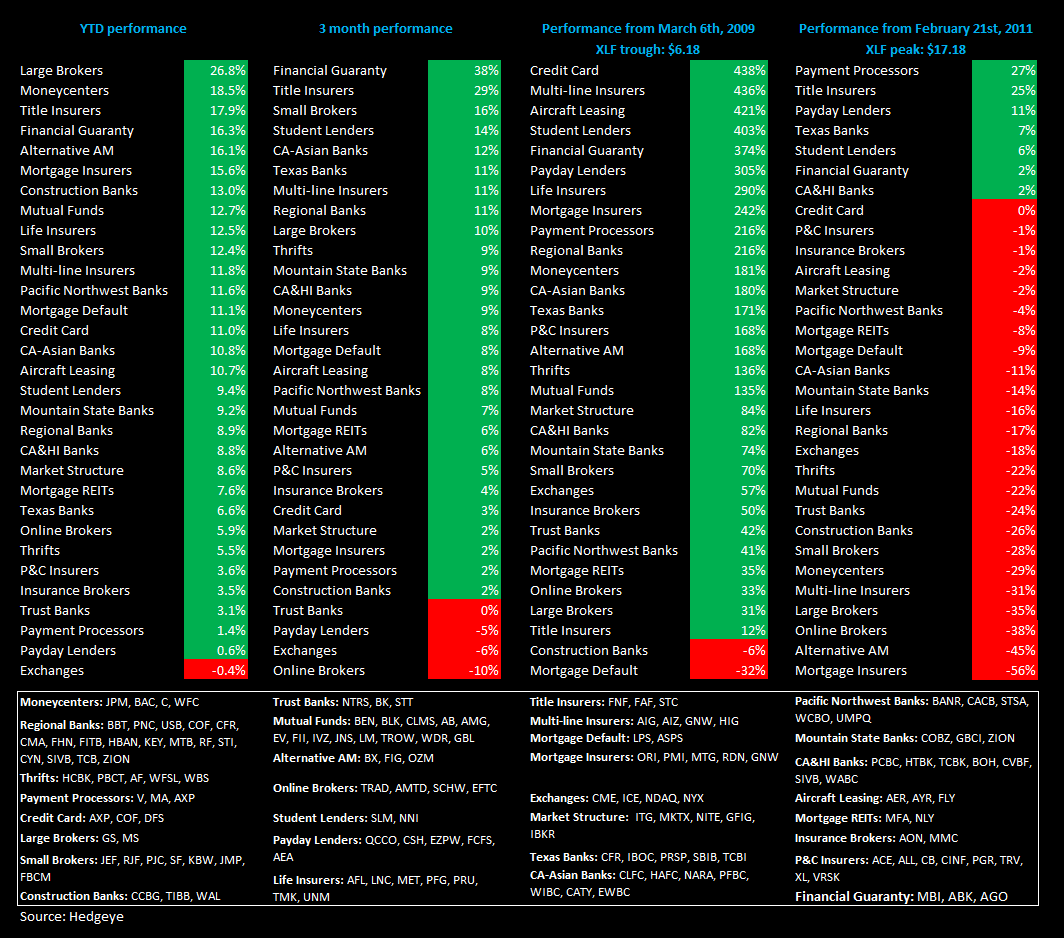

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link below.