TODAY’S S&P 500 SET-UP – February 2, 2012

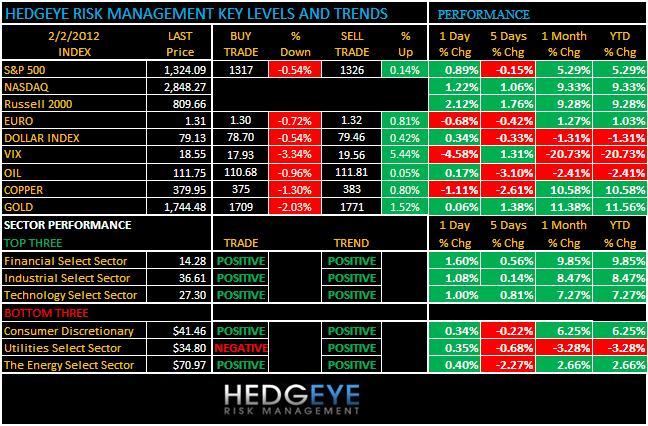

As we look at today’s set up for the S&P 500, the range is 9 points or -0.54% downside to 1317 and 0.14% upside to 1326.

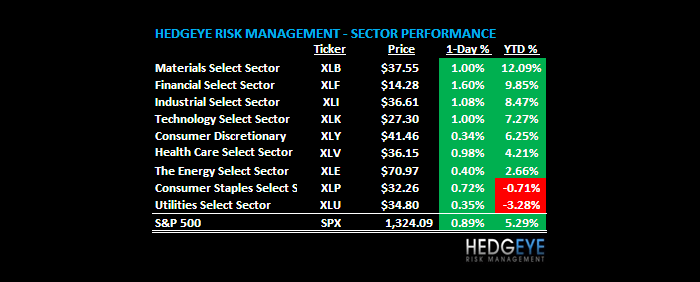

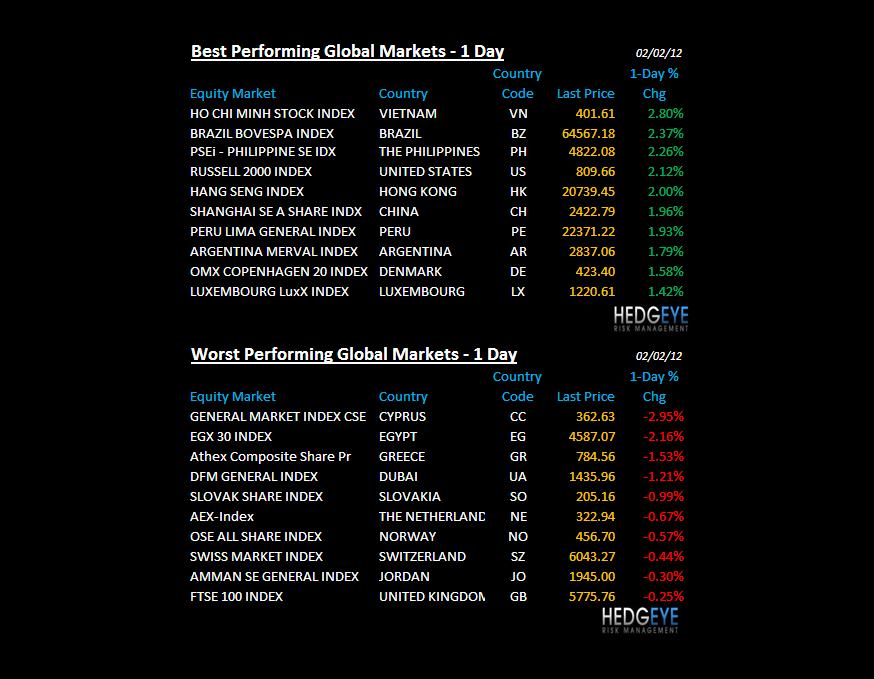

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1973 (1456)

- VOLUME: NYSE 892.64 (-13.69%)

- VIX: 18.55 -4.58% YTD PERFORMANCE: -20.73%

- SPX PUT/CALL RATIO: 1.68 from 1.56 (7.69%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – if you only bet with the bond market for the last year on its implied growth slowing/accelerating signals, you’d have not been sucked into any of the lower-highs in US Equities (FEB 2011, APR 2011, JAN 2012). We bought the long-bond back yesterday as the 10yr yield looks like it wants to make lower-lows for the YTD.

- TED SPREAD: 48.12

- 3-MONTH T-BILL YIELD: 0.06%

- 10-Year: 1.83 from 1.83

- YIELD CURVE: 1.61 from 1.60

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: Challenger Job Cuts (Y/y), Jan.

- 8:30am: Nonfarm Productivity (4Q P), est. 0.8% (prior 2.3%)

- 8:30am: Jobless Claims, wk of Jan. 28, est. 370k (prior 377k)

- 9am: Fed’s Evans speaks to reporters in Chicago

- 9:45am: Bloomberg Consumer Comfort, week of Jan. 29

- 10am: Fed’s Bernanke testifies before House Budget Committee

- 7:15pm: Fed’s Fisher speaks in Austin, Texas

GOVERNMENT:

- President Obama attends 60th National Prayer Breakfast, 7:30am

- Fed Chairman Ben Bernanke testifies on U.S. economy before House Budget Cmte., 10am

- Fannie Mae Chief Economist Douglas Duncan gives outlook for housing market to National Economists Club, noon

- House transportation committee considers 5-yr, $260b highway construction bill

- House, Senate in session:

- House Energy and Commerce subcommittee receives report of blue-ribbon commission on America’s nuclear future, 9:30am (Will hear from FDA Commissioner Margaret Hamburg on reauthorization of the prescription drug user fee act) 10am

- House-Senate payroll tax cut conference committee meets, 10am

- House Budget Committee hears from CBO Director Doug Elmendorf on the economic outlook, 10am

WHAT TO WATCH:

- ECB is likely to refuse to show its hand on how it will help cut Greece’s debt burden until investors and the govt. have agreed to a deal, economists said

- U.S. retailers inc. Macy’s, Gap report Jan. comp sales; Retail Metrics est. 2% gain, would be weakest monthly sales growth since Oct. 2010

- Glencore offered to buy outstanding $35b stake Xstrata that it doesn’t already own

- Facebook filed to raise $5b in largest Internet IPO on record

- IPO may value Mark Zuckerberg’s stake at $28.4b

- MF Global risk chief switch stalled euro debt cut by 6 mos.

- Ex-Credit Suisse CDO chief charged in scheme to boost bonuses

- Deutsche Bank reported 76% drop in 4Q profit as sovereign debt crisis curbed trading

- Sony Corp. more than doubled its annual loss forecast to $2.9b

- AstraZeneca to cut 7,300 jobs

- Deadline for states whether to join a proposed nationwide foreclosure settlement with banks to Feb. 6 from Feb. 3, Iowa’s Attorney General said

EARNINGS:

- Cigna (CI) 6 a.m., $1.19

- Diamond Offshore Drilling (DO) 6 a.m., $0.99

- Starwood Hotels & Resorts Worldwide (HOT) 6 a.m., $0.57

- Dow Chemical Co/The (DOW) 6:30 a.m., $0.31

- PulteGroup (PHM) 6:30 a.m., $0.07

- Roper Industries (ROP) 6:30 a.m., $1.21

- Spectra Energy (SE) 6:30 a.m., $0.49

- Boston Scientific (BSX) 7 a.m., $0.08

- Cardinal Health (CAH) 7 a.m., $0.76

- CME Group (CME) 7 a.m., $3.64

- International Paper Co (IP) 7 a.m., $0.61

- Merck & Co (MRK) 7 a.m., $0.95

- National Oilwell Varco (NOV) 7 a.m., $1.30

- Snap-on (SNA) 7 a.m., $1.18

- Viacom (VIAB) 7 a.m., $1.05

- Wisconsin Energy (WEC) 7 a.m., $0.47

- Xcel Energy (XEL) 7 a.m., $0.30

- Alliance Data Systems (ADS) 7 a.m., $1.49

- Elizabeth Arden (RDEN) 7:04 a.m., $1.39

- Goodrich (GR) 7:25 a.m., $1.57

- Cummins (CMI) 7:30 a.m., $2.24

- Sara Lee (SLE) 7:30 a.m., $0.25

- TECO Energy (TE) 7:30 a.m., $0.28

- Ryder System (R) 7:55 a.m., $0.97

- Kellogg Co (K) 8 a.m., $0.62

- Mastercard (MA) 8 a.m., $3.91

- Cameron International (CAM) 8:15 a.m., $0.76

- Blackstone Group (BX) 8:30 a.m., $0.40

- New York Times (NYT) 8:30 a.m., $0.42

- Royal Caribbean Cruises Ltd (RCL) 8:32 a.m., $0.16

- Allergan (AGN) 9 a.m., $1.00

- CareFusion (CFN) 4 p.m., $0.44

- Edwards Lifesciences (EW) 4 p.m., $0.59

- Principal Financial Group (PFG) 4 p.m., $0.75

- Wynn Resorts Ltd (WYNN) 4 p.m., $1.29

- Trimble Navigation Ltd (TRMB) 4 p.m., $0.48

- Vertex Pharmaceuticals (VRTX) 4 p.m., $0.72

- Fiserv (FISV) 4:01 p.m., $1.27

- Sunoco (SUN) 4:01 p.m., $(0.29)

- Stericycle (SRCL) 4:02 p.m., $0.74

- Novellus Systems (NVLS) 4:04 p.m., $0.45

- Con-way (CNW) 4:05 p.m., $0.36

- Gilead Sciences (GILD) 4:05 p.m., $1.05

- PerkinElmer (PKI) 4:05 p.m., $0.51

- Take-Two Interactive Software (TTWO) 4:05 p.m., $0.23

- Genworth MI Canada (MIC CN) 4:07 p.m., $0.78

- Genworth Financial (GNW) 4:10 p.m., $0.19

- Validus Holdings Ltd (VR) 4:15 p.m., $0.78

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor finally breaking its most immediate-term price momentum level of support of $3.83/lb this morning at the same time that Singaporean Stocks back off and moved red into the close. Stealth signals, but they’re leading ones that matter in our model. Copper’s long-term TAIL of 3.98/lb resistance intact – lower-highs.

- Copper Falls on Signals Demand May Be Poised to Slow in China

- Oil Falls to Six-Week Low as Stockpiles Rise, Fuel Demand Slips

- Gold May Advance as European Debt Crisis Concerns Spur Demand

- Glencore Makes Approach for Remaining $35 Billion Xstrata Stake

- Colombia Drug Lords’ Cattle Theft Rob Rally Benefit: Commodities

- Wheat Falls as Rain in U.S. Boosts Crop Prospects; Corn Drops

- Coffee Falls for Sixth Session on Ample Supplies; Sugar Retreats

- North Sea Oil Exports to Asia at 8-Year High: Energy Markets

- Impala Fires 17,200 Workers at World’s Biggest Platinum Mine

- Kinder Morgan Lapping Enbridge in Canadian Pipeline Race: Energy

- Rail Bottlenecks Thwart India Efforts to End Blackouts: Freight

- YPF Nationalization Concern Spurs Bond Plunge: Argentina Credit

- Emerging Nations’ Buying to Drive Gold to Record, JPMorgan Says

- Gold at Eight-Week High on Output, Dollar

- Shell to Boost Dividend for First Time Since 2009 on Projects

- EU Biofuels Targets to Cost Consumers $166 Billion, Study Says

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – all of the high-frequency economic data (inflation accel, growth decel) looks primed to slow in FEB as both the Shanghai Comp (+2% last night) and the Hang Seng (+12.5% YTD!) move to immediate-term TRADE overbought signals. Plenty of Johnny come lately pundits, who we didn’t hear a peep from when we bought China in DEC, going bullish.

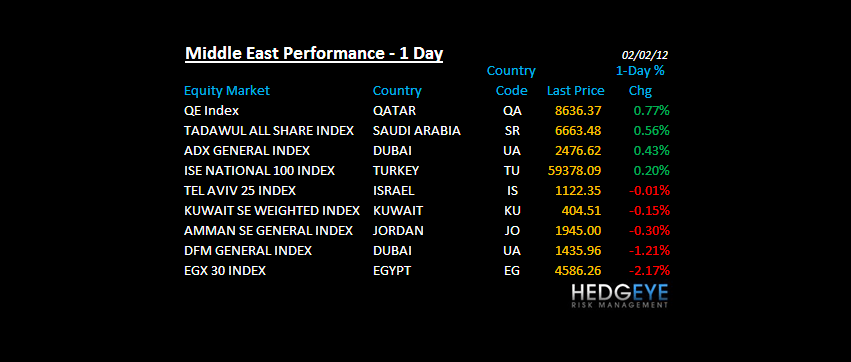

MIDDLE EAST

The Hedgeye Macro Team