1Q12 Senior Loan Officer Survey Takeaways

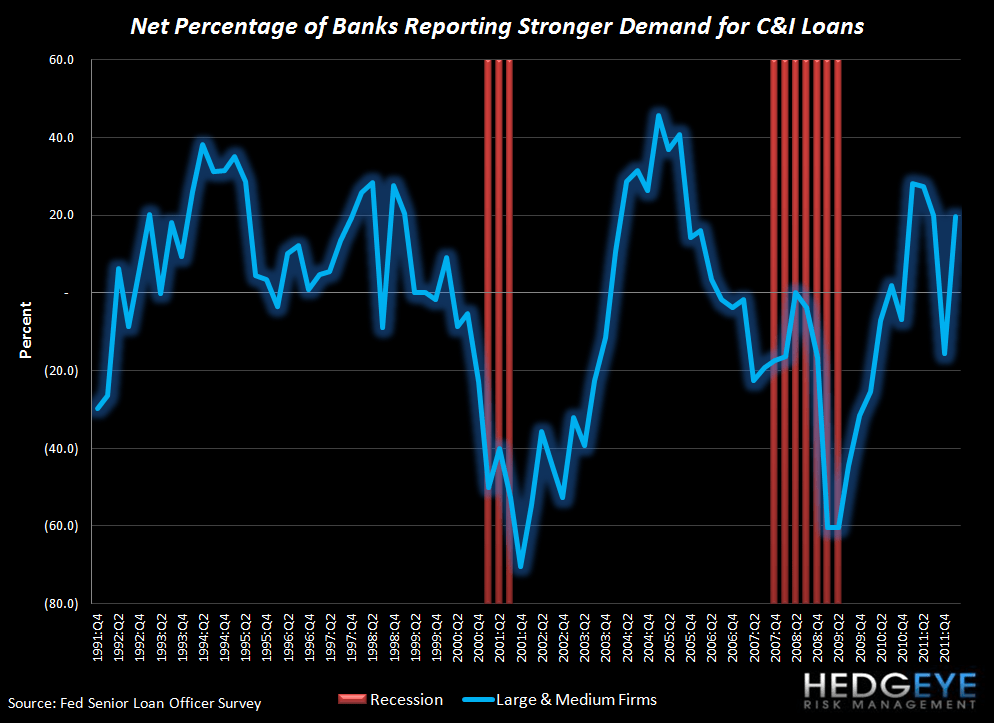

C&I Loan Demand Remains a Bright Spot

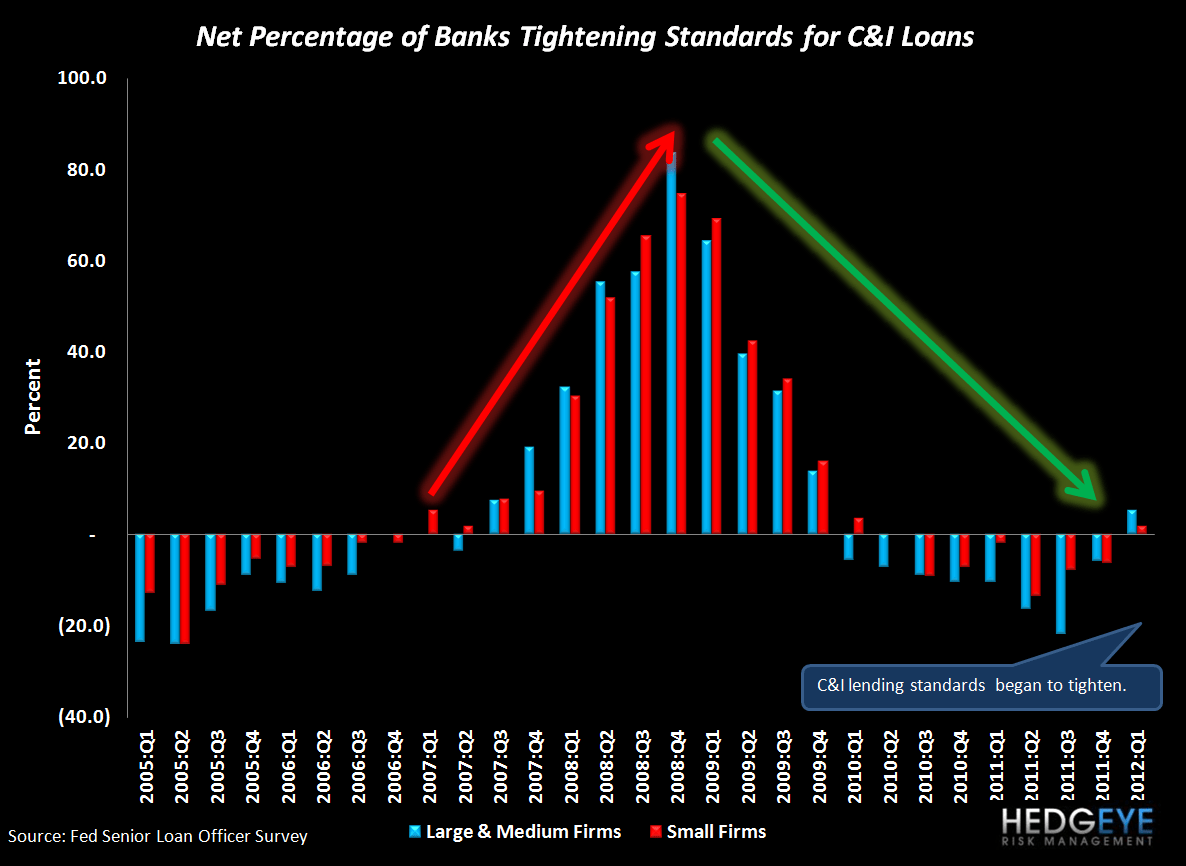

C&I showed sequential demand increase at both large and small size firms. After taking a stutter-step in 4Q with a sequential decline in demand, 1Q12's survey results showed that 19.6% of net respondents reported increasing demand for large and mid-size C&I loan demand as well as a net 15.1% of lenders reporting stronger demand for C&I loans from small borrowers. On the flip side, however, lenders also reported the first net tightening of standards since 4Q09. Though lenders reported only a net tightening of 5.4% on large borrowers and 1.9% on small borrowers, this is an inflection. Commentary from the report indicated that global US banks are reporting stronger demand in Europe reflecting the pullback from Europe's lenders. As a reminder, 4Q11 was the first quarter in which we saw broad-based sequential loan growth from the banks. It's fair to point out that the quality of this loan growth is somewhat circumspect from the Moneycenters to the Regionals.

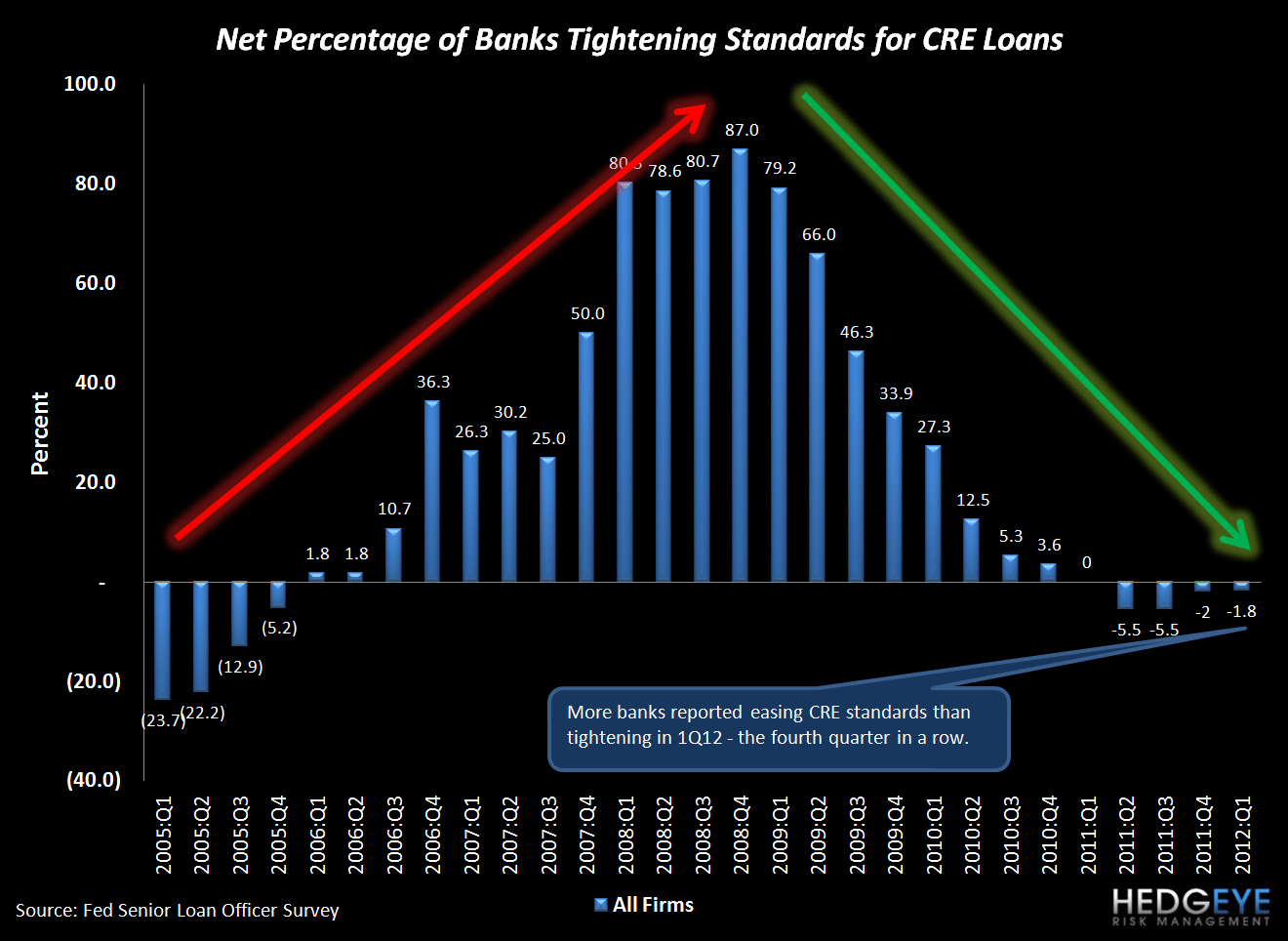

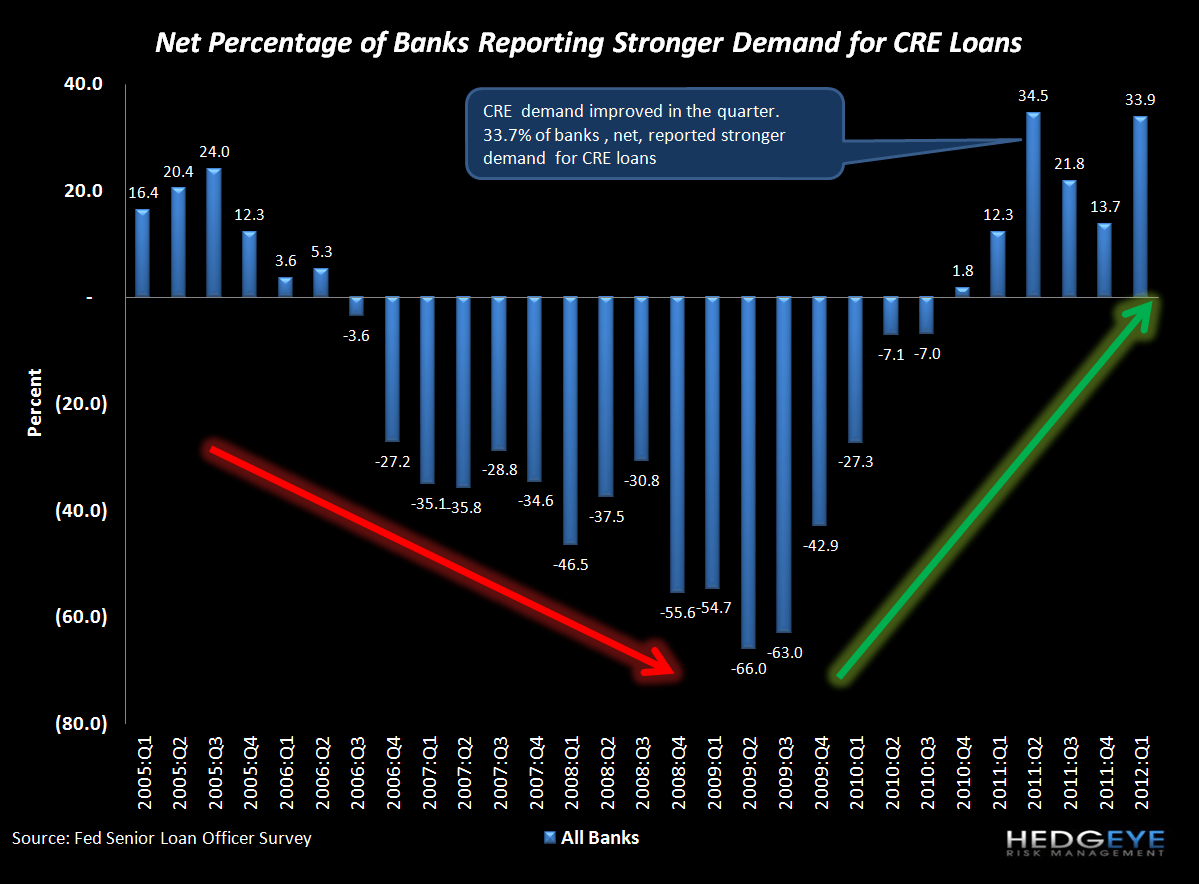

CRE Loan Demand Picks Up but Lenders Remain Cautious

CRE loan demand rose sharply in 1Q12. 33.9% of net respondents reporting increased demand. However, standards were essentially flat sequentially (-1.8% QoQ). It's worth noting that 2012 and 2013 will see significant increases in CRE loan maturities, much of which goes back to the frothy days of 2005/2006. As such, it's not surprising to see rising demand. The real question is whether the lenders will bite.

Residential Real Estate - Further Separating Prime from "Nontraditional"

Prime borrowers are facing with slightly relaxed terms, on the margin, while 3.8% of banks reported stronger demand for mortgages compared to 14.6% in the prior quarter. This is in contrast to nontraditional borrowers, who showed a sequential decline in demand and had banks tighten underwriting even further in the quarter.

Consumer Loans - Are Cards and Auto Frothy Yet?

This is the seventh consecutive quarter of easing standards on credit card loans and the fourth consecutive quarter (perhaps longer, but the data only goes back four quarters) of easing standards on auto loans. Meanwhile, demand for both categories of credit has been rising steadily for the past year - also the extent of the data under the Fed's new reporting format. For reference, the cumulative easing cycle in cards has been 77.2% from 3Q10 through 1Q12. That compares with the prior record of 43.4% from 4Q04 through 3Q07. To be fair, the bang up from 4Q07 through 2Q10 was severe, and as such you'd expect there to be significant easing on the other side. The question, however, is how close to frothy are we? Clearly competition for prime borrowers has been escalating for many quarters and the industry is finally now starting to see loan growth. Especially given the lack of growth in other areas, we think standards around card lending are likely getting quite lax.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link below to view in your browser.