This note was originally published at 8am on January 26, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“There is nothing wrong with change, if it is in the right direction.”

-Winston Churchill

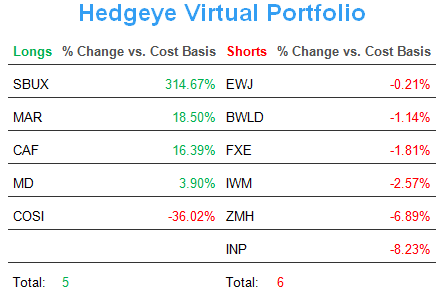

When they were both green yesterday, I sold my entire US Dollar (UUP) and US Equity positions (XLY and XLU) in both the Hedgeye Portfolio and the Hedgeye Asset Allocation Model. That takes me to 91% Cash.

What changed?

- Growth Expectations

- Inflation Expectations

- Fiscal and Monetary Policy

Very rarely do all 3 core fundamental research factors (Growth, Inflation, and Policy) change in a 24 hour period. Very rarely has the United States of America had both its President and Federal Reserve Chief delivering US Dollar Debauchery messages on back to back days.

Rather than listen to some Keynesian Quack tell you how yesterday’s Fed message isn’t inflationary or have another Washington “forecaster” tell you that inflation doesn’t slow growth, listen to what the market is telling you this morning:

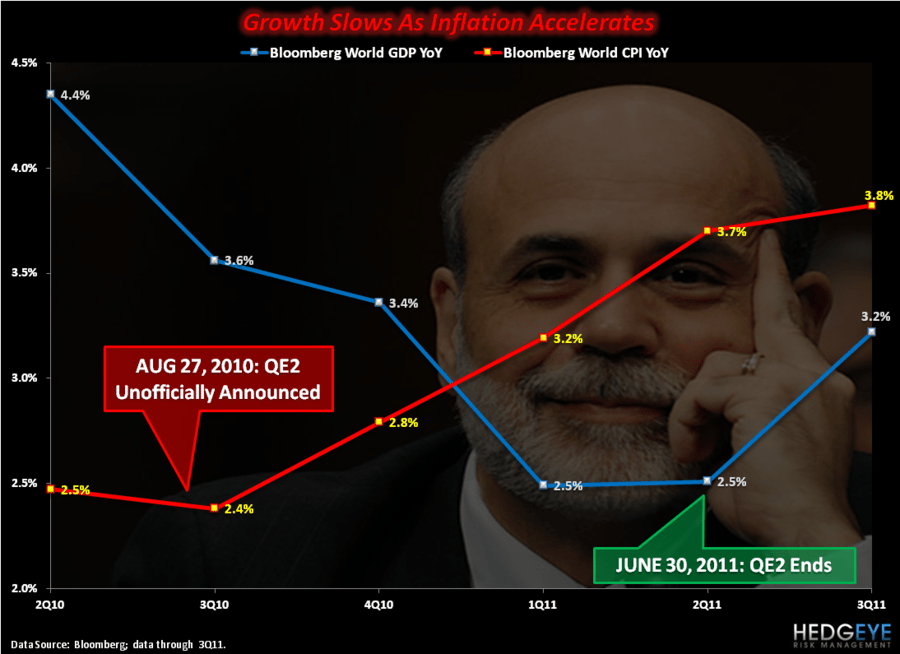

- Growth Expectations are falling (10-year US Treasury Yield snaps my 2.03% TREND support; Yield Spread compresses 6bps day/day)

- Inflation Expectations are rising (Gold, Copper, TIPs, etc. all went vertical post The Bernank’s 1230PM 1/25/12 USD Debauchery)

- The Growth Slowing TRADE (US Treasury Flattener, FLAT) is ripping – that’s what pancaking free market pricing of bond yields does

Now Masters of The Obvious will be quick to point out, as they tend to during any short-term hyper-inflationary move for stocks and commodities (German stocks looked awesome during the hyper-inflation of the 1920s) that this is good. No doubt it’s good for those who are long of the inflation policy – but really bad for the other 99% who get the inflation bill at the pump or in their food.

I’m not going to re-hash everything about my Globally Interconnected Economic Risk Management Model that got us to make the Growth Slowing call at this time of 2011. The model hasn’t changed. Big Government Interventions in markets have. *Reminder: they A) Shorten Economic Cycles and B) Amplify Market Volatilities.

Oh, and by the way – it’s not just a non-bank bailout Independent Research firm in New Haven, CT that gets it at this point:

- Jaime Dimon is explicitly calling out Bernanke for lowering long-term yields and compressing the Yield Curve

- Mitt Romney told Larry Kudlow last night that he’ll fire Bernanke and bring in his “own guy”

- The American Institute of Economic Research (www.aier.org) has already quantified what 0% means to the 99%

Just to recap the headline calculations out of the AIER that were released after Qe2 failed (July of 2011) in a paper titled “The Steep Cost of Cheap Money”:

- Zero Percent rate of return on American Savings accounts is huge income tax (it’s called interest income, confiscated)

- GDP lost (due to the interest income you could have spent) = upwards of $587B in US Consumption

- US Jobs lost (due to lost Consumption) = 2.4-4.6 million and “shaved between 1.75-3.32% to gross-domestic-product growth”

Oh, and by the way Part II – unlike the Fed who is completely politicized and dogmatized at this point, the American Institute of Economic Research is independent (neither politically or academically partisan).

Whenever the names of politicians are included in economic analysis, partisan people get emotional paralysis. Bush’s fiscal and monetary policies were as bad as Obama’s inasmuch as Jimmy Carter’s were as bad Nixon’s.

Nixon had no problems lying to the American People, but he actually told the truth on this score when he admitted “we are all Keynesians now.” Neither Bush nor Obama have been brave enough (or advised by someone analytically competent enough) about globally interconnected markets to say the same about the 1 thing they had in common – Bernanke.

To recap how the Global Macro market actually work:

- GROWTH: US and Emerging Market Growth is highly dependent on 71% of the US GDP number (Consumption Growth)

- INFLATION: Policies to Inflate (devalue the world’s Reserve Currency) slow real (inflation adjusted) growth

- SLOPES: since Qe2, the sequential rate of change in Growth has been highly affected by the rate of change in inflation (prices)

Bernanke and his boys will tell you inflation is “low” when it’s up and down. How else could a man tell you with a straight face that during all-time highs in the price of Oil, Food, and Gold that there is no inflation?

Since 2006, this guy hasn’t tightened monetary policy once. Whether his Qe2 Policy To Inflate slowed US GDP Growth to 0.36% in Q1 of 2011 or if it’s +733% higher at 3% GDP Growth today, he will not change as the data does. This is an embarrassment to the American flag. In order for Bernanke to have every last lemming who remains willfully blind enough to the math to believe him, he needs to fear-monger.

Fear-Mongering just when Strong Dollar = Stronger Employment = Stronger Confidence… just when things were getting better by simply having him out of the way – he’s back.

He’s telling American savers to go lever themselves up with stocks after a +96.2% run off the March 2009 lows. He’s telling Obama to give a “Mega Refi” to every one of your neighbors who levered themselves up and crushed the value of your home. He’s telling you to take 0% rate or return on your hard earned savings until 2014 and like it.

I’m telling you I’m Changing Direction. This country’s said political and academic leadership should too.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, and the SP500 are now $1676 (big TREND breakout level)-1721, $110.11-111.98, $1.29-1.31, and 1308-1331.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer