THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

#TheBernank Tax = rising inflation expectations and slowing growth expectations – the market now agrees:

- ASIA – the Chinese came back from holidays and just sold (we’re long Chinese Equities). They should have because Bernanke just jammed them w/ a commodity inflation tax and that’s the #1 thing, on the margin, that slows Chinese, Indian, etc growth. India’s Sensex(we’re short) failed at its TAIL line of 17,643 resistance and the Nikkei (we’re short) closed down for 3rd consecutive day.

- GERMANY – if the Greeks think they’re going to play a game of chicken w/ the Germans, I’ll take the Germans. Critically, the DAX backs off its long-term TAIL line of 6503 hard this morning as European stocks and bonds finally have a down day of consequence.

- TREASURIES – rising inflation expectations slow growth expectations – the 10yr yield is getting smoked this morning down to 1.86% and is right back into what we call a Bearish Formation. The Yield Spread has compressed 13bps in a week with Bernanke leaning on the long-end. Jaime Dimon won’t be pleased; neither will US Equity investors looking for rotation out of bonds.

On a snap of 1313, I have no support in the SP500 to 1297.

SUBSECTOR PERFORMANCE

<chart2>

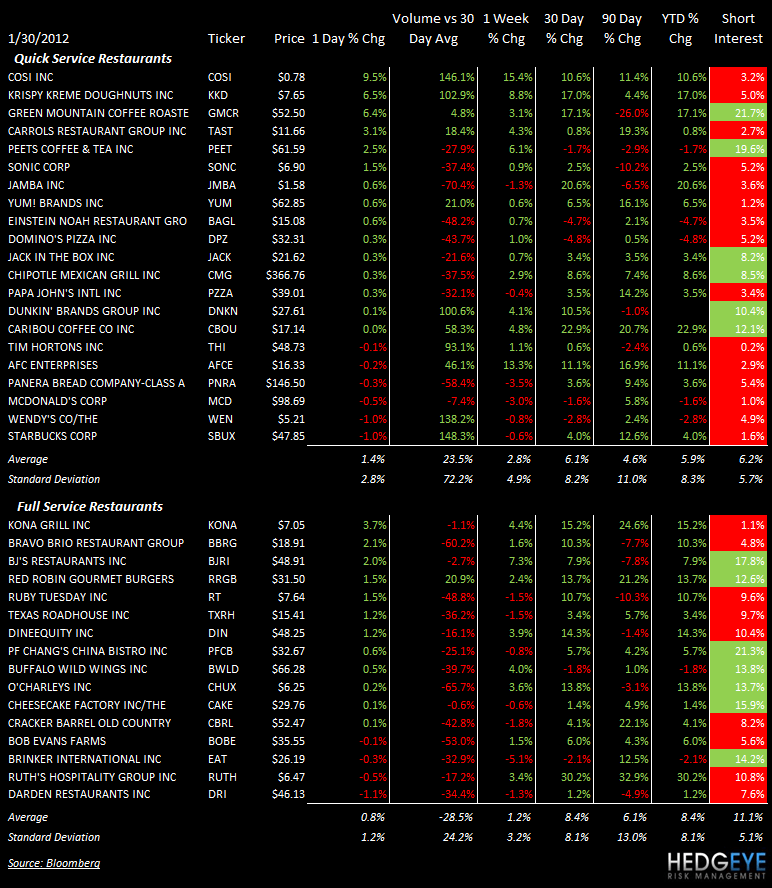

QUICK SERVICE

WEN: Wendy’s reported preliminary 4Q results this morning. EPS came in at $0.04, in line with consensus. North America systemwide comparable restaurant sales came in at +4.4%. The Analyst Day taking place today in New York is an important event for Emil Brolick, the new CEO, and we will be waiting to hear if he is lowering expectations for the company.

SBUX: Starbucks and Tata Global Beverages have formed an equal Joint Venture which will operate Starbucks cafes in India. The first store in India will open by August.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

COSI: Cosi put up some strong sales numbers last week

KKD: The breakfast daypart is performing well

GMCR: The bull/bear battle rages on

TAST: The split cometh

YUM: TACO Bell and PH in the USA had a better than bad quarter

WEN: Analyst day is today in NYC – this is Emil Brolick’s real coming out party. Will he lower the bar?

SBUX: Expectations were a little too high going into the quarter

Howard Penney

Managing Director

Rory Green

Analyst