TODAY’S S&P 500 SET-UP – January 27, 2012

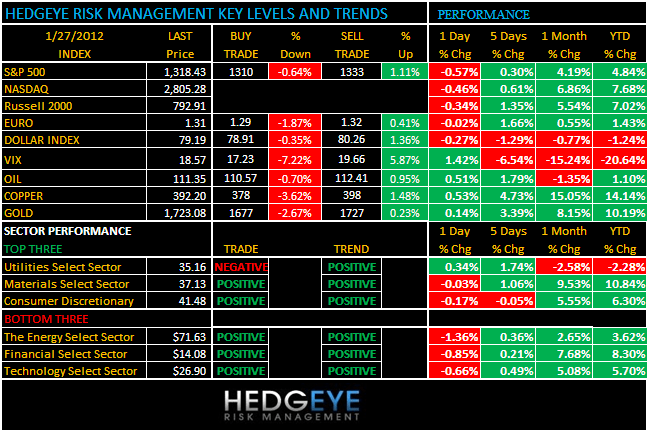

As we look at today’s set up for the S&P 500, the range is 23 points or -0.64% downside to 1310 and 1.11% upside to 1333.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -61 (-1622)

- VOLUME: NYSE 866.56 (4.35%)

- VIX: 18.57 1.42% YTD PERFORMANCE: -20.64%

- SPX PUT/CALL RATIO: 2.03 from 1.87 (8.56%)

CREDIT/ECONOMIC MARKET LOOK:

The Bernank Tax – Good morning America; you’re still seeing zero on the rate of return on your savings accounts and everything you put in your mouth or car is going up in price – try not to chomp on too many shiny rocks. Copper is up +14% for the YTD! Brent Oil prices are pushing for $112 and US Consumption stocks did not act well either yesterday or on good news (MCD and SBUX eps).

- TED SPREAD: 50.73

- 3-MONTH T-BILL YIELD: 0.04%

- 10-Year: 1.95 from 1.93

- YIELD CURVE: 1.74 from 1.72

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: GDP (Q/q) (Annualized), est. 3.0% (prior 1.8%)

- 8:30am: GDP Price Index, 4Q A, est. 1.9% (prior 2.6%)

- 8:30am: Core PCE (Q/q), 4Q A, est. 0.9 (prior 2.1%)

- 8:30am: Personal Consump, 4Q A, est. 2.4% (prior 1.7%)

- 9:55am: U.Mich, Jan. F, est. 74.0 (prior 74)

- 10am: Fed’s Dudley to speak on regional economy in NY

- 1pm: Baker Hughes Rig Count

GOVERNMENT:

- President Obama, VP Biden to address House Democratic Caucus annual retreat in Cambridge, Md.

- 8am: Quinnipiac University releases results of poll of likely voters in Florida’s Republican primary on Jan. 31

- 10am: Labor Dept. releases annual data on U.S. union membership

- House meets in pro forma session, Senate in session

WHAT TO WATCH:

- U.S. economy probably expanded in 4Q by 3%, fastest pace of 2011, as consumer spending picked up and companies rebuilt stockpiles, economists est.

- Former U.S. Treasury Secretary Larry Summers said in interview in Davos the recovery in the U.S. economy is underway, though it is not yet at “escape velocity.”

- Omnicare PharMerica bid unlikely to get U.S. approval, NY Post says

- FDA decision possible today on Amylin/Alkermes’s diabetes drug Bydureon

- More than 70% of investors said attack on Iran’s nuclear facilities would create only a short-term disruption in oil markets: Bloomberg Global Poll

- World Economic Forum

EARNINGS:

- Newell Rubbermaid (NWL) 6:30 a.m., $0.38

- Altria Group (MO) 6:58 a.m., $0.49

- Alliance Holdings GP (AHGP) 7 a.m., $0.83

- AO Smith (AOS) 7 a.m., $0.64

- Alliance Resource Partners (ARLP) 7 a.m., $1.78

- DR Horton (DHI) 7 a.m., $0.05

- Ford Motor (F) 7 a.m., $0.25

- Honeywell International (HON) 7 a.m., $1.04

- IDEXX Laboratories (IDXX) 7 a.m., $0.63

- Legg Mason (LM) 7 a.m., $0.25

- Procter & Gamble (PG) 7 a.m., $1.08

- Dominion Resources (D) 7:30 a.m., $0.64

- NextEra Energy (NEE) 7:31 a.m., $0.91

- T Rowe Price Group (TROW) 7:32 a.m., $0.69

- Moog (MOG/A) 8 a.m., $0.74

- Chevron (CVX) 8:30 a.m., $2.85

- NuStar GP Holdings LLC (NSH) 8:43 a.m., $0.31

- NuStar Energy (NS) 8:45 a.m., $0.31

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Bulls Ascendant Amid Biggest Rally Since 1980: Commodities

- Copper Advances as Stockpile Orders Jump to Eight-Year High

- Crude Heads for Weekly Gain; Total Sees $100 Support for Brent

- Cocoa Extends Gains in London After Stockpiles Drop; Sugar Rises

- Rubber Drops, Paring Weekly Gain, as Data Raise Growth Concern

- Gold May Rise in London as Low Interest Rates Support Demand

- Commodities Open Interest Dropped Most in Three Years in 2011

- Rusal May Cut Aluminum Output 6% in Next 18 Months, CEO Says

- Rubber Seen Driven by China Demand Recovery, StanChart Says

- Indonesia’s Kharisma Sells 4,500 Tons of Palm Oil (Table)

- Cattle Herd Drop to 1958 Low Boosting Cost for McDonald’s, Tyson

- Palm Oil Seen Declining 5.2% by February: Technical Analysis

- Copper to Stall as Record Prices Spur Mining: Chart of the Day

- Commodities Daybook: Oil Heads for First Weekly Gain in Three

- Corn Heads for Biggest Weekly Gain in Five; Soybeans Advance

- Palm Oil Posts Weekly Decline on Concern Over Malaysia Exports

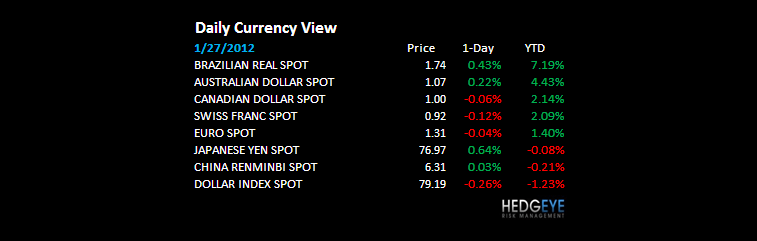

CURRENCIES

EUROPEAN MARKETS

GERMANY – these guys have to be smiling from ear-to-ear; they effectively gave the world’s Keynesian central planners the bird for 6 months and now the German DAX is up +11.1% YTD, busting a move above my long-term TAIL line of 6503 (DAX). Import Prices in Germany dropped in DEC to 3.9% y/y vs +6.0% NOV, so look for that price pressure to come back in Jan/Feb (BernankTax).

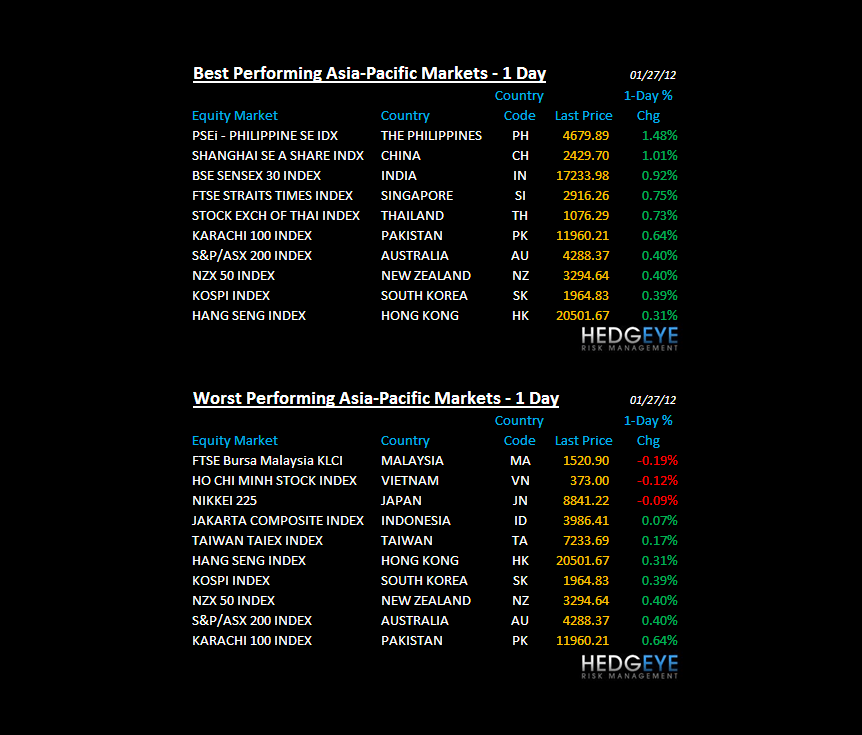

ASIAN MARKETS

JAPAN – how’s that 20yr Keynesian experiment treating you? We’ll have an in depth research note out on Japan again today; JGBs and Yens are not acting like we should be ignoring this risk like the Old Wall has – may be a bigger risk than Europe’s sovereign debt within 6 months. Shorting both Japanese Yen and the Nikkei on green days (FXY and EWJ).

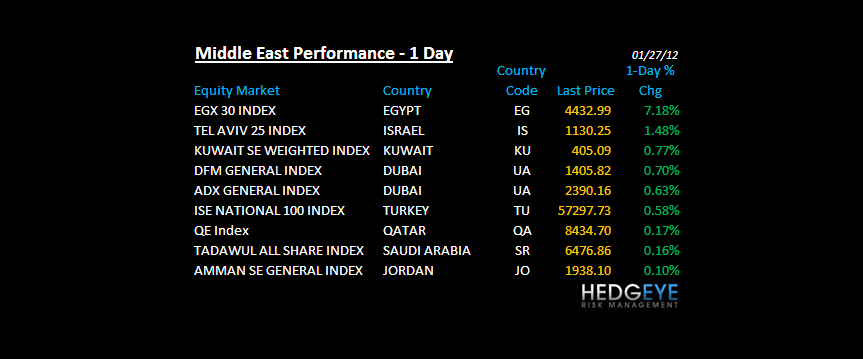

MIDDLE EAST

The Hedgeye Macro Team