THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Employment

Jobless Claims came in at 377k versus 370k consensus and a revised 356k for the week prior (revised from 352k).

Beef Prices

We called this out in our Commodity Chartbook last night but it’s worth noting again that the U.S. cattle herd is expected to show a 1.4% drop in cattle numbers from a year ago. Cattle prices could be given another boost by this data point when it is released.

Comments from CEO Keith McCullough

You can take everything I have been bullish about (Global Equities) for 6 wks and turn it as upside down as Bernanke’s policy to inflate is:

- US DOLLAR – with the back-to-back US Dollar Debauchery statements from Obama and Bernanke, the US Dollar has broken its immediate-term TRADE line of support; now the question is will it hold its $78.03 intermediate-term TREND line of support (EUR/USD TREND resist = 1.34)? Last night when I was on Kudlow, Romney said he’d fire Bernanke – I would too. Enter the debate.

- INFLATION – Bernanke fans can say whatever they want; bottom line is that market prices don’t lie; Keynesians do – Bernanke telling savers 0% is their rate-of-return until he gets fired has created an absolute 24hr meltup in both Inflation Expectations (TIPS) + Commodity Inflation –Copper and Gold just went vertical to $3.90/lb and $1720/oz en route to test bubble highs?

- 91% CASH – I obviously had very little patience for Qe2’s policy to inflate and got very bearish on this Feb-Apr of 2011 because INFLATION SLOWS GROWTH. If oil, copper, and cattle prices keep ripping like this, there is a very high probability that all of Global Growth slows, sequentially, in late JAN early FEB. Not good.

As these policies change, I have. My process has not. Before I retire, I can only hope we have a Fed that changes as the data does.

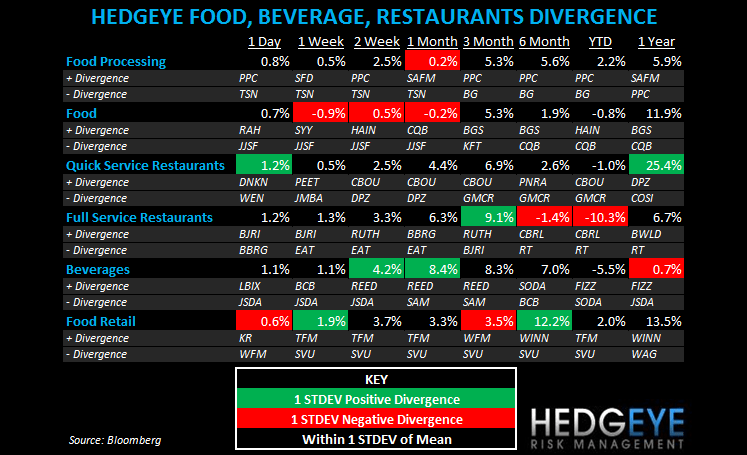

SUBSECTOR PERFORMANCE

QUICK SERVICE

SBUX: Starbucks reports after the close today. The company needs to put up a 10% comp in the USA and 8% internationally to keep two year trends flat sequentially from 4QFY11. With McDonald’s reporting a 9.8% and weather helping, it’s not out of the realm of possibility. As we said in our MCD note the phrase “expectations are the root of all heartache” comes to mind. It’s hard to see that SBUX is going to put up numbers that are going to beat already bullish same-store sales numbers. Due to higher coffee costs and margin pressure on the CPG business, the Street is expecting 8% EPS growth on 12% revenue growth.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

DNKN: Reporting EPS on Monday

CBOU: On the BofA M&A list for 2012

COSI: Hearing positive things about the new CEO

AFCE: Reported strong 4Q performance after the close

OTHER QSR NEWS

Better-burger segment player Smashburger Wednesday said it grew its restaurant base by 55 percent and entered 12 new markets in 2011 to end the year with 143 locations. The Denver-based chain, which is owned by Consumer Capital Partners, said its 51 new restaurants and a 3-percent increase in same-store sales at existing locations pushed annual systemwide sales to $115.7 million. - NRN

FULL SERVICE

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

BWLD: Somebody does not agree with me

EAT: Recovered nicely from Tuesday’s sales miss

Howard Penney

Managing Director

Rory Green

Analyst