THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

Contrast the Top 2 US Headlines this morn: 1. "Apple Profit More Than Doubles" vs. 2. "Fair Share" – I don’t get it – markets don’t either:

- US DOLLAR – I #SOTU Word Scored the entire speech last night and the US Dollar was not mentioned once. #FairShare had 5 mentions and #Capitalism = 0. Just words, but they matter – Even the NYT and BBC ran #FairShare in their headline this morning. It’s just not good for my Strong Dollar case. Clinton and Regan both rolled w/ Strong Dollar, Strong Consumption (ie 71% of US GDP)

- TREASURIES – stocks lost all of their Pre-#SOTU speech Apple momentum and have gone red this morning as UST Bond Yields fall a few beeps and the Yield Curve compresses by 3 basis points d/d. If you had to score the speech on Growth, it didn’t score well either. 10yr UST Yields of 2.03% is the most important Global Macro line in my model right now. If we snap it, I’ll get more defensively positioned.

- GLOBAL EQUITIES – at about 6PM last night I thought the futures had it right and Apple was going to bust a move taking the SP500 to a fresh YTD high – no dice. Instead we are looking at what’s called an Outside Reversal from Monday (testing new highs intraday of 1322, failing, and closing at/below prior closing high). Asian, European, and Latin American stocks at risk of doing the same.

My bullish Strong Dollar, Strong America tone is changing this morn, because globally interconnected prices have.

SUBSECTOR PERFORMANCE

QUICK SERVICE

MCD: A McDonald's restaurant in Dickinson, N.D., is offering $300 signing bonuses for prospective employees. The move comes as North Dakota's unemployment rate hovers around 3.4 percent, the lowest in the nation (NRN.com).

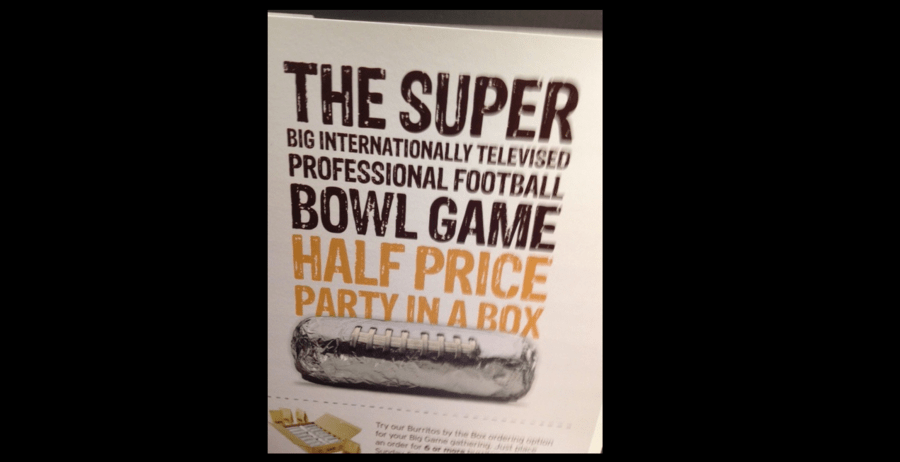

CMG: Chipotle is running a promotion on Super Bowl Sunday offering half-off burrito boxes. The promotion is generating publicity for the company because of the ad itself.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

TAST: Working diligently on the separation of the two companies

DPZ: On a relative basis it was a good day for DPZ

CASUAL DINING

EAT: Brinker was raised to Buy from Hold at KeyBanc Capital.

Other Casual Dining News

Del Frisco Restaurant Group LLC filed registration papers for an IPO.

Howard Penney

Managing Director

Rory Green

Analyst