“The only thing I’m addicted to is winning. This bootleg cult, arrogantly referred to as Alcoholics Anonymous, reports a 5 percent success rate. My success rate is 100 percent.”

-Charlie Sheen

I’m not sure Keith realized that today was my birthday when he asked me to write the Early Look, rather he was likely focused on the fact that I’m Hedgeye’s resident political analyst and last night was President Obama’s fourth state of the union address. This was also Obama’s last state of the union address ahead of the 2012 elections.

For those of you who aren’t active on the Twitter-sphere (my handle is @HedgeyeDJ if you are), the expression “#winning” was popularized by actor Charlie Sheen early last year when he started a one man campaign against the traditional world of entertainment. In effect, he was saying he wasn’t going to conform to Hollywood 1.0 any longer. He also announced on twitter that he would continue to win and, amongst other things, the term #winning started trending in dramatic fashion.

Watching the state of the union address last night on Twitter was fascinating to say the least. Keith has called twitter the new tape many times, and I think it’s also the new political pundit. In terms of markets for opinion, at least in 140 characters, twitter is about as efficient as it gets. If you make comments of interest and insight, your followers will increase and so will your influence via your Klout score.

Last night as people were watching President Obama’s address, the key term that was trending on twitter was #fairshare and it is still trending this morning. This morning I searched #fairshare on Twitter to get a sense for the consensus view of the speech and the general concept of #fairshare. Here are the top tweets that came up:

@ewmonster: The defining issue of our time, is how to keep the American Dream alive. THAT is a paraphrase worth making! #fairshare #sotu

@EconBrothers : Obama is right. Everyone should pay their “fair share” of taxes, even those who currently pay no federal income taxes. #FairShare #SOTU

@MonicaCrowley : And here we go again w/ the Warren Buffett warfare tax BS. #FairShare

@IAmSoSmart : I am thoroughly convinced that if democrats understood how hard I worked for my money, it would blow their tiny mind. #FairShare

@KeithMcCullough : #SOTU Word Score: #FairShare = 5, #Capitalism = 0

And my personal favorite:

@EricComedy : If Obama uses the phrase #FairShare one more time, I’m going to stomp on a live gerbil. #SOTU

In all seriousness, Obama clearly used this address to launch the key theme of his campaign, which is that he wants to, at least rhetorically, level the playing field for all Americans. Whether that practically, or economically, makes sense is somewhat beside the point. Certainly, in his speech last night President Obama didn’t offer much beyond platitudes. If you don’t believe me on that last point, here is the New York Times’ interpretation:

“Mr.Obama presented a somewhat modest list of initiatives he could enact through executive authority coupled with more ambitious proposals unlikely to advance in Congress.”

In effect, there was nothing in his speech that would practically move the needle from an economic perspective. Nonetheless, President Obama appears to be #winning.

According to InTrade this morning, President Obama’s chances of re-election have increased to 56%. For the last eight months, this probability has been mired below or just above 50%, but in the last two weeks the election markets at InTrade are pricing in an increasing likelihood of an Obama re-election. This is in part due to the increasingly heated rhetoric and dysfunction emanating from the Republican primary. That said, the economy has started to improve on the margin which benefits the incumbent and the President’s messages are broadly appealing. #FairShare in 2012 is the #Hope and #Change of 2008.

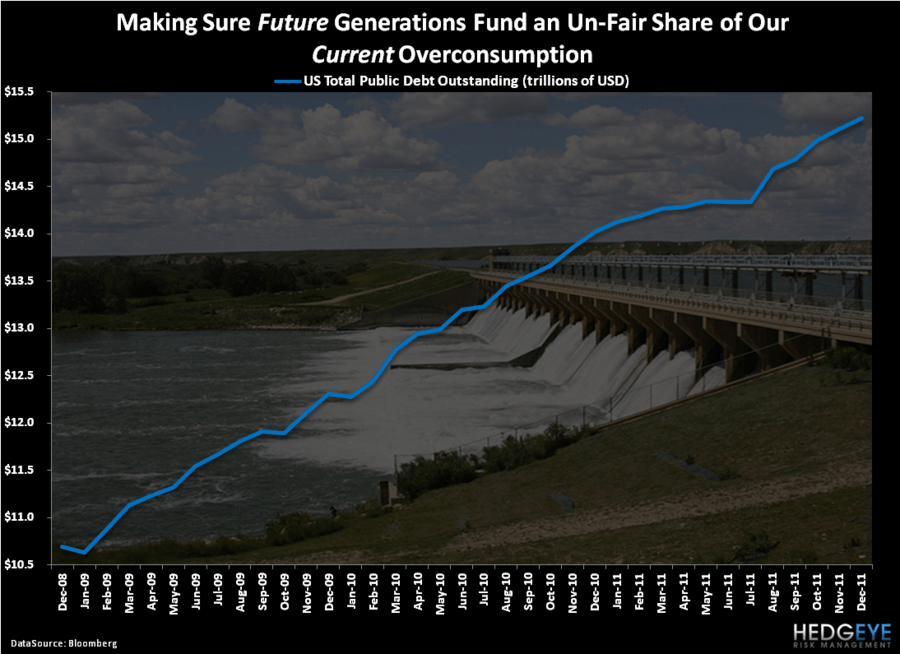

One of our key criticisms of both the Obama and the George W. Bush Presidencies were their carte blanche backing of Keynesian economic policies. In the Chart of the Day, we show the notional expansion of U.S. federal government debt under President Obama. Under President Obama, the United States experienced the largest one year federal debt increase ever and in his first term, when complete, the United States will likely have added more than $6 trillion in debt to the national balance sheet. This is more than both of George W. Bush’s terms combined.

The key risk of an Obama second term and a Fair Share agenda is that the growth of the federal government and its obligations continue to accelerate. Already, the U.S. is beyond the 90% debt-to-GDP line in which long term economic growth becomes structurally impaired accorded to more than 200 years of data from Reinhart and Rogoff. In the shorter term, a view by the markets that the federal government is less focused on fiscal prudence is negative for the dollar and detrimental to our thesis that a strong dollar will increase the 70% of GDP that is consumption.

In the chart of the day, I’ve actually included a picture of the Bassano Dam, which is a large irrigation dam south of my hometown of Bassano, Alberta. When it was constructed in 1915, the Bassano Dam was the largest man made irrigation dam in the world and a game changer for the agricultural community of southern Alberta. It was a project that was funded by the government. The point being that not all government funded projects are negative for the economy. On the other hand, government spending for the sake of ambiguous goals that lack an ROI, like #FairShare, is only likely to add to our debt balance and constrain future consumption and growth.

Since both parties like to channel Ronald Reagan these days, I’ll end with a quote from the Gipper:

“We must not look to government to solve our problems. Government is the problem.”

Indeed.

Our immediate-term TRADE ranges of support and resistance for Gold, Oil (Brent), EUR/USD, US Dollar Index, German DAX, and the SP500 are now $1, $109.44-110.85, $1.28-1.31, $79.41-80.43, 6, and 1, respectively.

Keep your head up and your stick on the ice,

Daryl G. Jones

Director of Research