Top Line Problems Are Harder to Fix

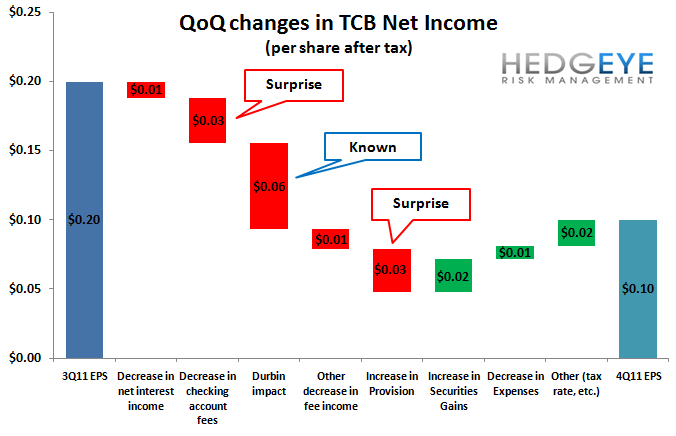

TCF Financial (TCB) put their revenue issues front and center in their 4Q11 report yesterday. Separate from the expected $15M decline in card income from Durbin, fee and service charge revenue fell $7M as the new fee product that management had hyped turned out to be a debacle. In all, the company saw a 21% sequential decline in total fee income (excluding gain on sale of securities and loans), a reduction of $25M. This top line weakness led to the company reporting a $0.10 quarter vs. expectations for $0.14.

TCB's "innovation" (as they persisted in calling it in their remarks) was to charge depositors $28 per day whenever the customer has a negative balance, rather than a per-item NSF charge. Management has spent the last several quarters talking up their new system, including how much customers "love" it. As it turns out, some customers dislike the fees so much that they're "changing their behavior" to avoid them and closing their accounts. The potential for bad press from the "innovation" is also high. For example, the Chicago Tribune carried a story last month about a teenager whose savings account balance of $4.85 had turned into a -$229.10 deficit after TCB assessed a monthly maintenance fee of $9.95 followed by a daily $28 fee for the next 8 days.

The company had been running a pilot program in certain areas earlier in the year, then rolled out the initiative to everyone in 4Q, only to be met with a resoundingly negative reaction, as evidenced by the sequential revenue decline. Where do they go from here? Clearly, TCB could backpedal completely and revert to the old structure. However, closed accounts are unlikely to come back. The company promised additional "innovations" in 1Q12 (hopefully revenue-positive this time around) and expects the fee income to rise starting in 2Q12. We expect that a new baseline has been established, and incremental revenue gains will be as challenging as ever.

Other items from the quarter:

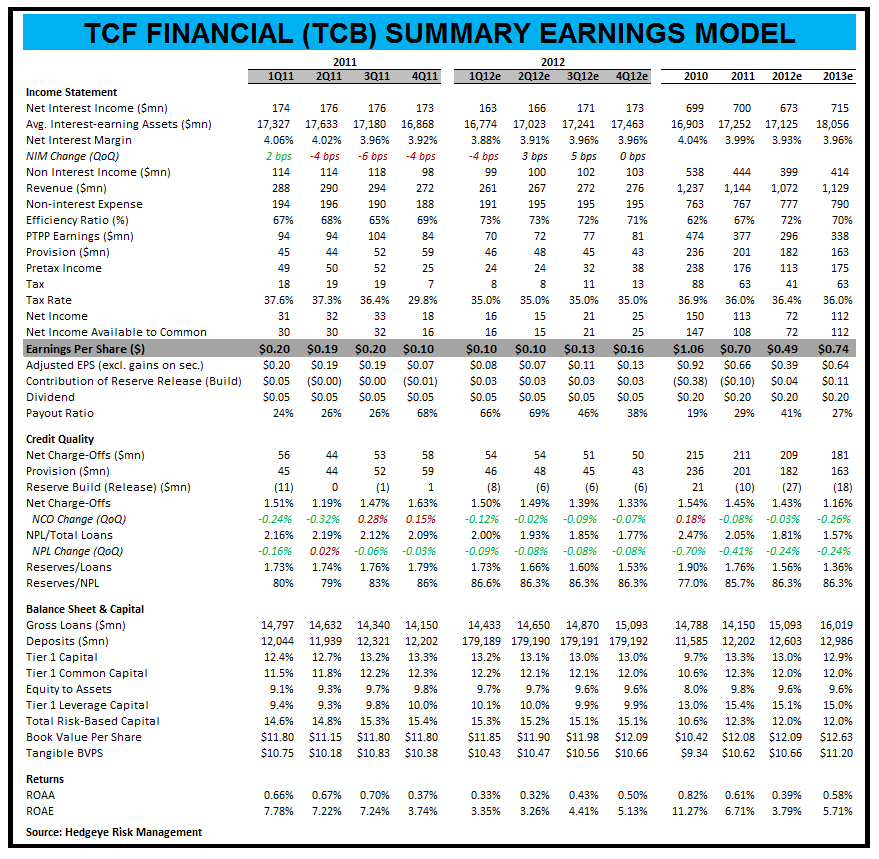

- Net income fell slightly in the quarter, with 4 bps of NIM pressure. TCB was able to squeak out 9 bps of decline in deposit interest costs, driving an 8 bps reduction in total cost of interest-bearing liabilities, plus a further 4 bps decline from increased volume of non-interest-bearing deposits. Thus, they were largely able to offset the 8 bps of yield pressure they faced. This is largely consistent with the rest of the space, and underscores how hard the banks need to work to offset asset yield declines.

- Credit remains an issue at TCB, despite the company's choice of accounting. Since 1Q11, the company has been shifting delinquent borrowers into short-term modifications, and then rolling them into long-term modifications when the original modifications expire. The long-term modifications can be up to 5 years. In 4Q, residential TDRs increased to a new high of $433M, up $54M QoQ. We believe that the company ultimately will bear credit costs on these loans, the vast majority of which will not cure and resume paying the higher amount. With the use of TDR accounting, TCB postpones the costs and drags them out over a long period. It's a good strategy for optical earnings, but doesn't change the true earnings power.

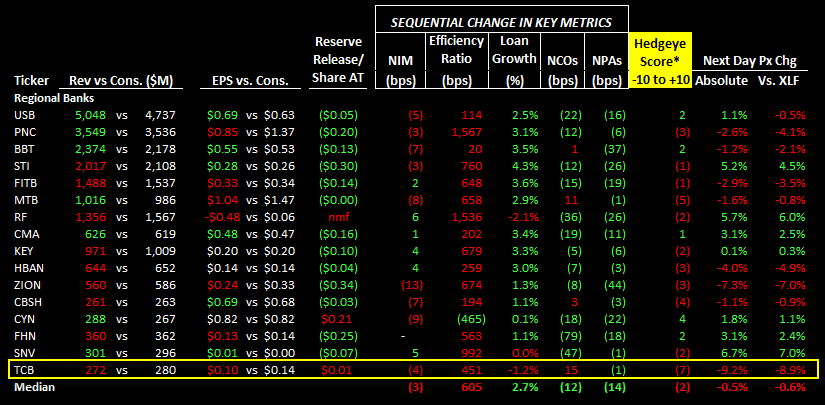

- Loan growth is also an issue. TCB reported the second-worst loan growth of all the regionals that have reported so far. The following table demonstrates.

Lowering Our Estimate

In light of this loss of revenue, we are lowering our 2012 earnings expectations to $0.49 from $0.73. We are decreasing our estimate of their ability to offset lost Durbin revenue, efforts which management had promised in 1Q12. TCB is talking a good game about its need to reinvent itself, as its regional model has been hit hard by credit costs, legislation, and interest rate policy over the last five years. However, such things take time, and we ultimately believe that 2012 earnings estimates need to come down significantly. Prior to this morning's report, consensus expected $0.84 in 2012 - a high bar when the current run rate is $0.40.

The Stock

While negative throughout 2011, we previewed the fourth quarter on January 12th with a relatively neutral disposition, as our estimate was more or less in-line with consensus, even though our full-year 2012 estimate was below the Street at $0.73 (vs consensus $0.87). Our argument at the time was that we didn't expect the company to lose money and with the stock was trading at 105% of tangible book value, downside in the stock was limited. Shame on us. The reality is that when estimates need to come down, the stock has downside, as this quarter clearly showed. Given the 4% sequential decline in tangible book value per share due to the goodwill brought on from the closing of the Gateway acquisition, the stock, even after the sell-off yesterday is trading at 101% of tangible book value. However, we are still below the Street. While we expect estimates will come down in the wake of the quarter, we'd be surprised if they come down to our $0.49 level. Until they do, we will maintain our bearish bias.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.