This note was originally published at 8am on January 17, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Expert intuition strikes us as magical, but it is not.”

-Daniel Kahneman

This weekend I finally started reading Daniel Kahneman’s “Thinking, Fast and Slow” and was pleasantly surprised to see him cite one of my favorite American thinkers, Herbert Simon (read “Models of My Life”), in the Introduction:

“The situation has provided a cue; this cue has given the expert access to information stored in memory, and the information provides the answer. Intuition is nothing more and nothing less than recognition.” (Thinking, Fast and Slow, page 11)

Pattern recognition is the fulcrum principle of Chaos Theory. While neither Kahneman nor Simon have drawn that parallel to Global Macro Risk Management, if they did what we do every day I think they probably would have.

Back to the Global Macro Grind…

While consensus has spent 2012 caught in the vacuum of 2011’s news (European Crisis and Growth Slowing), we’ve been letting this globally interconnected marketplace of colliding factors give us cues on Growth Slowing’s Bottom (Q1 Hedgeye Macro Theme):

- Strong US Dollar = Stronger US Consumption, Confidence, and Employment

- Deflating The Inflation = Growth Slowing at a slower rate in Asia (China in particular)

- German Fiscal Conservatism = Bullish German Stocks on both our TRADE and TREND durations

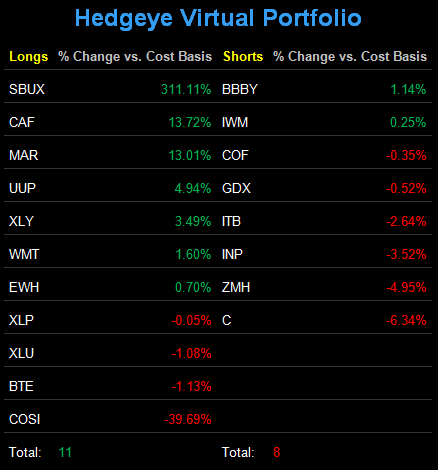

There should be no surprises about what’s happening in US, Chinese, or German stocks this morning. Our leading indicators have been giving us Crystal Clear Cues for the last 3 weeks. That’s why we have our largest asset allocation to US Equities in over a year. That’s why we’re long Chinese and Hong Kong Equity exposures. That’s why we’ll open this morning with no European shorts.

In the order that these Expert Cues appear in my notebook this morning:

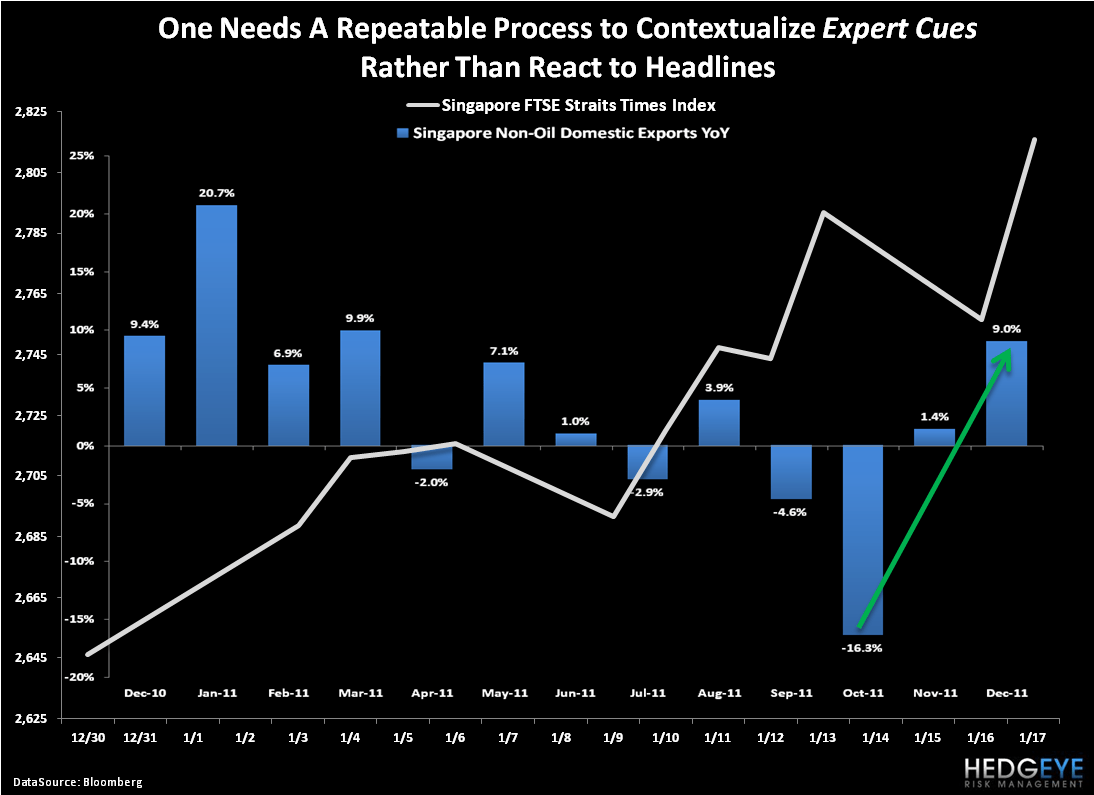

1. CHINA – closing up +4.2% overnight, the Shanghai Composite had its best move since October of 2009. Growth Slowing in China is a 2-year stale story that we have signaled in real-time. Looking at the higher-frequency economic data that was reported closest to now (the December data, not the quarterly), China appears to be seeing Growth Slow at a Slower Rate. Chinese Industrial Production for DEC accelerated to +12.8% y/y (vs +12.4% in NOV). Meanwhile, Singapore’s Export Growth for DEC jumped to +9% y/y (vs +1.4% in NOV). You’ll recall we use Singapore as a leading indicator for Eastern demand.

2. GERMANY – trading up another +1.7% to an impressive +7.2% for 2012 YTD, the German DAX is proving that this morning’s concurrent indicator of confidence (the German ZEW reading) was better than bad for good reason. It was actually the biggest 1-month pop in the ZEW reading ever – and ever is a long time. Germany is proving that fiscal conservatism can support strong domestic employment (6.8% vs USA’s 8.6%). Not pandering to the political winds of the Keynesian bailout beggars should also be commended.

3. USA – holding above both my long-term TAIL line (1267 support) and the closing high of October 29th, 2011 (1285), the SP500 is proving that Strong Dollar = Strong Consumption works where it matters in the American economy – on 71% of US GDP Growth. Neither we (nor the US Treasury Bond Market) are suggesting US Growth is great, but the US Currency and Equity markets aren’t signaling a US recession either. Provided that the US Dollar remains strong (Romney winning in South Carolina this week will continue to help), we think US Growth’s Bottom could very well be happening in Q411 through Q112.

With Expert Cues in hand, we derive our summary positioning in the Hedgeye Asset Allocation Model:

- Cash 58% = down from 70% at the end of 2011

- US Equities = 18% (Consumer Discretionary, Consumer Staples, Utilities – XLY, XLP, and XLU)

- Int’l Currency = 15% (US Dollar – UUP)

- Int’l Equities = 9% (China and Hong Kong – CAF and EWH)

- Fixed Income = 0%

- Commodities = 0%

That’s a very different mix in my asset allocation than what I was carrying from April-November of 2011. I’ve moved from a big allocation to Growth Slowing at an accelerating rate (Long Fixed Income) to long Growth Slowing’s Bottom (Long Equities).

What hasn’t changed is my position in the US Dollar and Commodities. I still think that Strong Dollar = Deflates The Inflation, so look for me to potentially short some Commodities today.

Having a repeatable risk management process isn’t magical. Neither is it perfect. It’s just what we do.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, US Dollar Index, Shanghai Comp, German DAX, and the SP500 are now $1626-1678, $110.20-114.33, $1.25-1.28, $80.72-81.97, 2220-2301, 6151-6329, and 1284-1302, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer