TODAY’S S&P 500 SET-UP – January 19, 2012

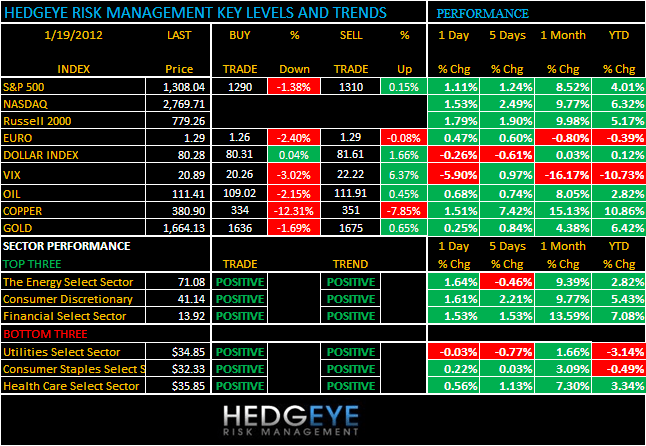

As we look at today’s set up for the S&P 500, the range is 20 points or -1.38% downside to 1290 and 0.15% upside to 1310.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1773 (1092)

- VOLUME: NYSE 797.74 (-1.58%)

- VIX: 20.89 -5.90% YTD PERFORMANCE: -10.73%

- SPX PUT/CALL RATIO: 1.67 from 1.42 (+17.61%)

CREDIT/ECONOMIC MARKET LOOK:

RATE CYCLE – this is something we talked about a lot in clients meetings in NYC for the last 2-days. This is very bullish for the US Dollar in terms of monetary policy differentials – all of Asia and Latin America are in easing mode after being hawkish while Bernanke should have been (throughout 2010). Brazil just cut by another 50bps; Philippines cut for 1st time since 09 (joining Indonesia, Thailand, Australia, etc). Bullish for Global Equities vs 2011.

- TED SPREAD: 54.09

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 1.89 from 1.90

- YIELD CURVE: 1.67 from 1.67

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: ECB president Draghi press conference with Sultan Bin Nasser al-Suwaidi of United Arab Emirates central bank

- 8:30am: CPI (M/m), Dec., est. 0.1% (prior 0.0%)

- 8:30am: Housing Starts, Dec., est. 680k (prior 685k)

- 8:30am: Building Permits, Dec., est. 680k (prior 685k (revised)

- 8:30am: Jobless Claims, week Jan. 14, est. 384k (prior 399k)

- 9:45am: Bloomberg Consumer Comfort, week of Jan. 15

- 10am: Freddie Mac 30-yr mortgage

- 10:00am: Philadelphia Fed., Jan., est. 10.3 (prior 6.8 (revised)

- 10:30am: EIA Natural gas storage

- 11am: DoE inventories

- 1:00pm: U.S. to sell $15b 10-Yr TIPS

WHAT TO WATCH:

- Eastman Kodak filed for bankruptcy protection from creditors, listing assets of $5.1b, debt of $6.8b

- Bristol-Myers, AstraZeneca failed to win FDA clearance to sell first in new class of experimental diabetes pills as regulators sought more data on medicine’s safety

- BankUnited said to decide to remain independent as takeover offers fall short of its expectations

- Greece’s govt. in second day of talks with private creditors on accord that would slash nation’s debt

- HUD Secretary Shaun Donovan, DoJ official set to meet with state AGs next week to rally support for proposed settlement with banks over foreclosure practices

- TransCanada’s Keystone pipeline seen moving ahead on alternative route

- Kinder Morgan said to be considering piece-by-piece sale of El Paso’s oil-exploration business as offers for entire operation due this week: WSJ

- President Obama said to consider nominating Larry Summers to lead World Bank

- Hedge funds may sue Greece in European Court of Human Rights to make good on its bond payments: NYT

- No U.S. IPOs expected to price today

EARNINGS:

- Huntington Bancshares (HBAN) 5:55 a.m., $0.14

- BB&T (BBT) 6 a.m., $0.53

- Knight Capital Group (KCG) 6 a.m., $0.25

- UnitedHealth Group (UNH) 6 a.m., $1.04

- BlackRock (BLK) 6:30 a.m., $2.98

- Southwest Airlines Co (LUV) 6:50 a.m., $0.08

- Bank of America (BAC) 7 a.m., $0.13

- Johnson Controls (JCI) 7 a.m., $0.62

- Morgan Stanley (MS) 7:15 a.m., $(0.57)

- Rockwell Collins (COL) 7:30 a.m., $0.84

- Fairchild Semiconductor (FCS) 7:30 a.m., $0.16

- Freeport-McMoRan Copper & Gold (FCX) 8 a.m., $0.61

- Union Pacific (UNP) 8 a.m., $1.82

- PPG Industries (PPG) 8:11 a.m., $1.27

- Progressive /The (PGR) 8:27 a.m., $0.35

- Cubist Pharmaceuticals (CBST) 4 p.m., $0.33

- Flextronics (FLEX) 4:01 p.m., $0.20

- Google (GOOG) 4:02 p.m., $10.49

- Capital One Financial (COF) 4:05 p.m., $1.55

- Intel (INTC) 4:05 p.m., $0.61

- Intuitive Surgical (ISRG) 4:05 p.m., $3.34

- People’s United Financial (PBCT) 4:05 p.m., $0.19

- American Express Co (AXP) 4:06 p.m., $0.99

- International Business Machines (IBM) 4:06 p.m., $4.62

- Microsoft (MSFT) 4:06 p.m., $0.76

- Associated Banc-corp (ASBC) 4:10 p.m., $0.23

- Skyworks Solutions (SWKS) 4:30 p.m., $0.50

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – when the Doctor gives us the signal, we listen. That breakout my model signaled last week > $3.45/lb was as pure as a cold Canadian beer on the 1st of July. Copper up another +1.4% this morning in what should be considered nothing short of a massive squeeze = +11% YTD.

- Sugar Traders Bet Biggest Glut in Five Years Ending: Commodities

- Oil Gains in New York on Shrinking Stockpiles, Iranian Risks

- Copper Climbs on Speculation China May Relax Curbs on Credit

- Thai Rice Production Seen Climbing to Record After Floods

- Gold Advances to a 1-Month High as Euro Rallies, Demand Gains

- Corn Advances on ‘Irreversible’ Damage to Crops in Argentina

- Cocoa Gains as West Africa Supply May Start to Slow; Sugar Rises

- U.S. May Expand Corn Output to Offset Argentina Loss, FAO Says

- Palm Oil Imports by Pakistan May Plunge on Truckers’ Strike

- Super Bowl Chicken Wings Flying to Record High: Chart of the Day

- Shell Venture Spurs Cosan’s Investment-Grade Bid: Brazil Credit

- Oil Grab in Falkland Islands Seen Tripling U.K. Reserves: Energy

- Cholera Risk Means Mounting Costs for Hapag-Lloyd, Torm: Freight

- COMMODITIES DAYBOOK: Crude Rises on Shrinking Supply, Iran Risk

- Food Demand to Stay ‘Strong’ Amid Global Slowdown, Viterra Says

- Palm Oil Prices to Be ‘Firm’ in 2012 on Crude Oil, Soybeans

- Aluminum May Extend Rally to $2,295 Per Ton: Technical Analysis

CURRENCIES

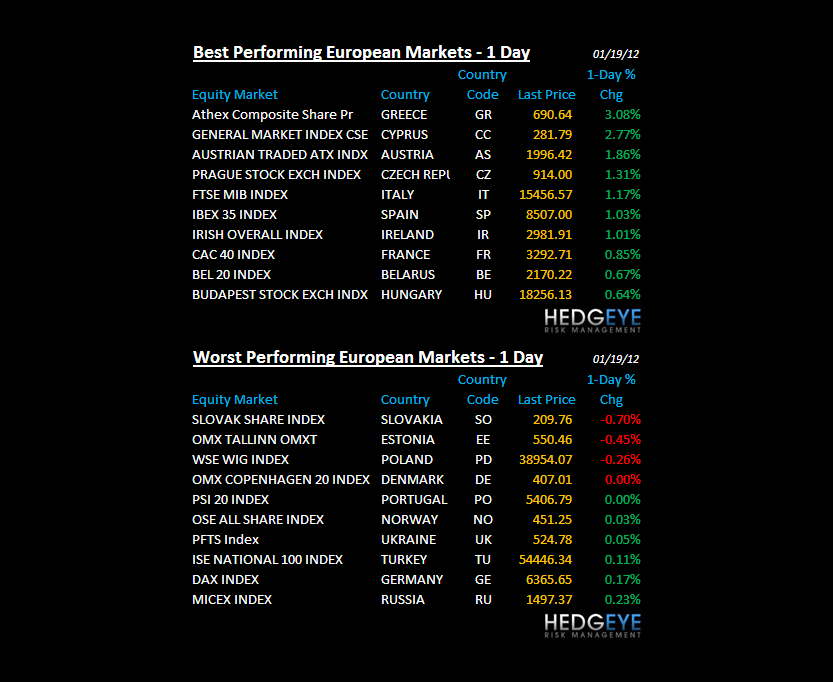

EUROPEAN MARKETS

ASIAN MARKETS

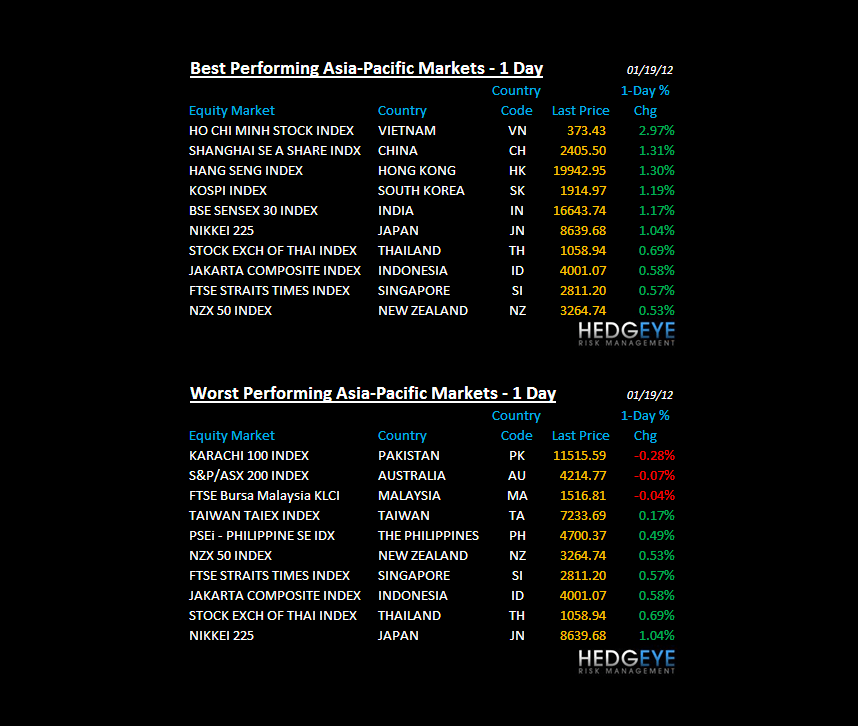

CHINA – get the slope of the money supply and lending cycle in China right (finally easing instead of tightening), you’ll get a lot of things Chinese Growth right. Shanghai Comp and Hang Seng both up another +1.3% respectively overnight on “news” that China’s top 5 banks are going to ease lending reqs. End of the world thesis = bad YTD.

MIDDLE EAST

The Hedgeye Macro Team