This note was originally published at 8am on January 10, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Perpetual optimism is a force multiplier.”

-Colin Powell

Politicians have been trying to spin multiplication theories for generations. From time to time, within their own groupthink tanks, these theories have become particularly influential – especially with the large percentage of the political-class that doesn’t do math.

In 1936, when he wrote the General Theory, John Maynard Keynes focused on what he infamously coined “The Multiplier Effect.” The theory was that every dollar spent by government would have a multiplier effect (greater than 1) rippling throughout the economy. Unfortunately, when Keynesian governments tried that in the late 1920s it didn’t work – and it hasn’t worked since.

Despite being proved wrong throughout the 1929-1933 period, Keynes, ever the master Storyteller, found a way to re-frame his vision of the elixir of a government-stimulated life. Keynes preached “that it is a complete mistake to believe that there is a dilemma between schemes for increasing employment and schemes for balancing the budget.” (Keynes Hayek, page 135)

What does 1 scheme multiplied by 2 more failed schemes equal? But these guys have to do something!

Fortunately, President Bill Clinton figured this out and wanted nothing to do with being labeled a Keynesian. President Clinton, like President Reagan, oversaw one of the 2 largest decades of employment growth in US history (by decade, the 1980s and 1990s saw between 18-22 million jobs added (net), respectively – Obama/Bush decade = net zero).

And Clinton did it with a balanced budget mandate…

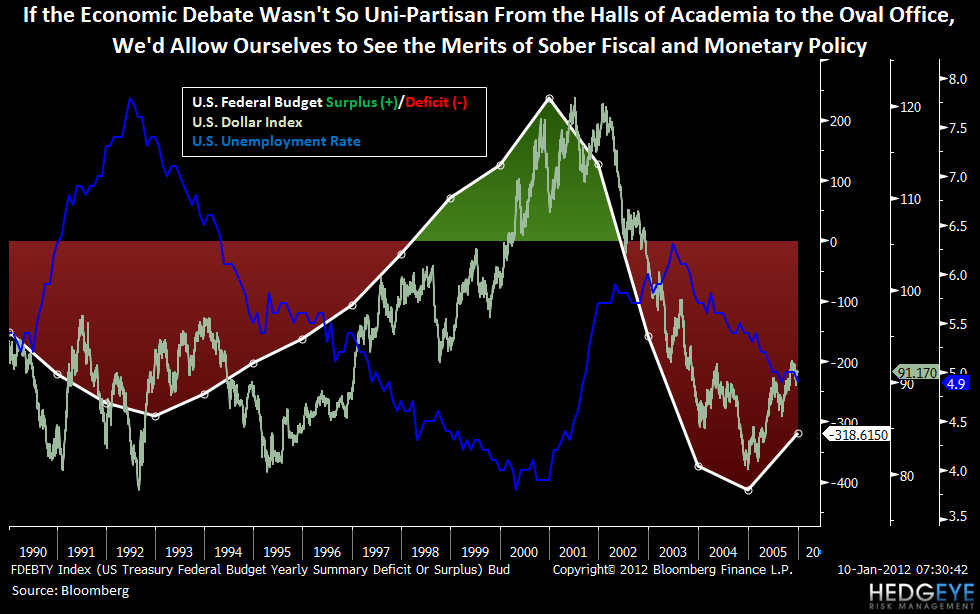

Fact Check: Clinton’s Balanced Budget Act of 1997 led to the following Federal Budget results:

- 1998 = +$69B surplus

- 1999 = +$124B surplus

- 2000 = +$230B surplus

“… the first surplus in three consecutive years since 1947-1949, when Harry Truman was President. The debt had been reduced by $360B in three years with $223B paid in 2000, the largest one-year debt reduction in American history.” (Keynes Hayek, page 274-275)

I’m not a Republican or a Democrat. I’m just a man who wants to get this right. And, setting aside all of the other angles on this Presidential Election, I think that if Obama or Romney get the economic policy messaging right, they’ll win the election.

So far, President Obama has a lot of Reagan in his economic policy legacy (ballooning national debt balance and Keynesian spending). Romney’s got plenty of baggage too, but maybe he has a bigger opportunity to be the change Americans want to see in our economics.

Last night on The Kudlow Report, Larry asked me what I’d suggest Romney be (economically). My answer: ½ Clinton ½ Reagan.

Back to the Global Macro Grind…

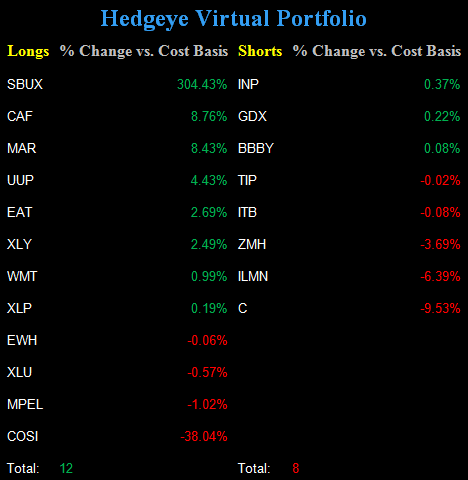

I’m coming into this morning’s US market open hot. I don’t mean Alabama Crimson Tide hot – I mean locked and loaded with the most Global Equity exposure I’ve had in well over a year:

- Long US Consumer Discretionary(XLY)

- Long US Consumer Staples (XLP)

- Long US Utilities (XLU)

- Long Chinese Equities (CAF)

- Long Hong Kong Equities (EWH)

But how hot is hot? Well, get out the calculators and tell me what your money is up or down if you sold all of your Asian and US Equity exposure between February and April of last year, and you tell me.

We all invest from the vantage point of what’s in our own accounts. This cochamamy storytelling of the Old Wall that there is an optimal “asset allocation” is as broken as Keynes personal accounts were when they crashed in 1929.

Money compounds. Anyone who does math with their own money gets that. Money also gets evaporated during big draw-downs (i.e. if you’re still long SP500 1565 from October 2007, you’re still down -18.2% from there and need to be up over +22% to get back to breakeven). That’s math too – it’s called geometric.

For my money, moving to a 24% total Global Equity asset allocation in an environment like this actually makes me really nervous. Maybe that’s why it’s working for 2012 YTD (Chinese Equities are already up +3.9% for the year). Maybe it’s not. All I know is that what I don’t know is what makes me nervous about being long anything tied to government decision making.

Maybe Powell was right about the force-multiplier of optimism. Maybe I’ve been right on the trust-divider of fear-mongering. All I know is that, combined with a Strong Dollar, the best of ½ Clinton ½ Reagan is a winner for me.

My immediate-term support and resistance levels for Gold, Oil (Brent), EUR/USD, US Dollar Index, Shanghai Composite, and the SP500 are now $1592-1645, $111.89-115.61, $1.26-1.29, $80.41-81.61, 2178-2295, and 1269-1291, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer