TODAY’S S&P 500 SET-UP – January 4, 2012

Raging European bears are begging for bad news and they just aren’t getting it 4 days into the year, yet… KM

As we look at today’s set up for the S&P 500, the range is 18 points or -0.79% downside to 1267 and 0.62% upside to 1285.

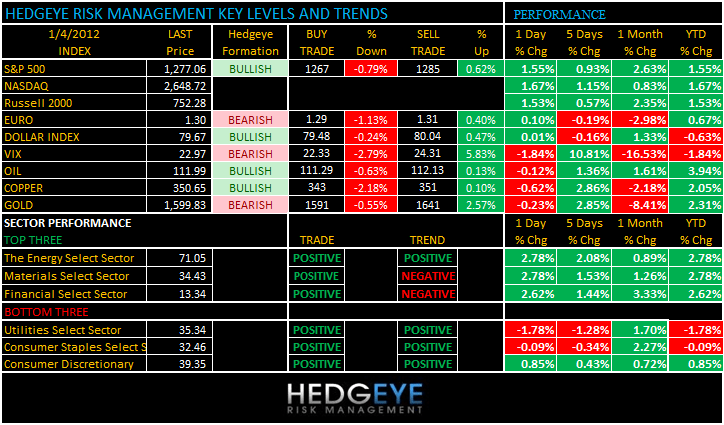

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1659 (+1813)

- VOLUME: NYSE 855.12 (+45.42%)

- VIX: 22.97 -1.84% YTD PERFORMANCE: -1.84%

- SPX PUT/CALL RATIO: 1.88 from 1.49 (+26%)

CREDIT/ECONOMIC MARKET LOOK:

10YR – really bullish for German Bunds to see 4.06B of 10yr paper printed 4bps below 10yr UST’s (1.93% on Bunds vs 1.97% on USTs). Keith is watching 10yr UST’s like a hawk for a confirmation that Growth’s Bottom (2011 Slowdown) is in. He'd need to see a sustained breakout > 2.03% to sell TLT and keep ramping up Global and US Equity exposure (moved to 12% Global Equities yest).

- TED SPREAD: 57.23

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 1.97 from 1.89

- YIELD CURVE: 1.64 from 1.70

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- 7am, MBA Mortgage Applications, Dec. 30

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 10am: Factory Orders, Nov., est. 2.0% (prior -0.4%)

- 11:30am: U.S. to sell $30b 4-week bills

- 4:30pm: API inventories

- Eurozone Dec preliminary CPI +2.8% y/y vs consensus +2.8% and prior +3.0%

- Eurozone Dec Final services PMI 48.8 vs consensus 48.3 and prior 48.3

WHAT TO WATCH:

- President Obama to discuss economy at high school in Shaker Heights, Ohio, 1:15pm

- Yahoo may name CEO this morning; PayPal president Scott Thompson a leading candidate: AllThingsD

- Mitt Romney beat Rick Santorum by 8 votes in Iowa caucuses, each capturing less than 25%; Ron Paul third, Rick Perry considering whether to continue campaign

- Bullish sentiment decreases to 49.5% from 50.5% in the latest US Investor's Intelligence poll

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Citigroup Sues Hedge Fund Manager in Singapore Over Gold Losses

- China’s Wen Jiabao Sees ‘Relatively Difficult’ First Quarter

- Raw-Materials Rebound Seen as Economy Skirts Slump: Commodities

- Oil Trades Near 8-Month High on Iran Tension, Shrinking Supply

- Exxon in Talks to Restructure Stake in Japan Refining Unit

- Gold May Advance for a Fourth Day on Outlook for Asian Demand

- Dalian to ‘Seriously Consider’ Vale-Ship Protests, Owners Say

- Oil Trades Near 8-Month High on Iran Tension, Shrinking Supply

- Vedanta Plans India Caustic Soda Unit, Cost-Cuts as Prices Dip

- Copper Drops as Europe Crisis Boosts Demand Concern; Tin Slumps

- Chesapeake Comes Up Short of Investment-Grade: Corporate Finance

- Hong Kong Keeps Ban on Some Poultry Imports Due to Avian Flu Tie

- Copper Falls as Societe Generale Says Prices May Drop Almost 10%

- Gold Demand in India Is ‘Moderate,’ Rajesh Exports Says

- Dow Climbs to Highest Since July, Oil Surges on Manufacturing

- Saudi Arabia May Cut Oil Premiums for February From Record Highs

- Silver Will Lead Gains in 2012 Among Raw Materials: Table

CURRENCIES

EUROPEAN MARKETS

GERMANY – shaping up on the long side after really impressive employment data this wk (6.8% unemployment rate for DEC amidst the mayhem) and a better than bad Services PMI this morn (52.4 DEC vs 52,7 NOV). German 10yr bond auction was solid too - KM

ASIAN MARKETS

ASIA – after 2 solid up days to start 2012, the 3rd was not a charm – China down -1.4%, HK -0.8%, and India -0.5% reminds us that Equity market bottoms are processes, not points. December data implies growth slowing at a slower rate in Asia (but it’s still slowing).

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- U.S. Spurns Iran’s Demand to Keep Aircraft Carrier Out of Gulf

- U.A.E. Deposit Fall May Squeeze Banks as Debt Looms: Arab Credit

- Oil Trades Near 8-Month High on Iran Tension, Shrinking Supply

- Afghan Taliban Takes Step Toward Peace Talks to End War With U.S

- Huawei’s Work in Iran May Violate U.S. Sanctions, Lawmakers Say

- U.S. Defense Strategy Plan Focuses on Thwarting China, Iran

- Oil Trades Near 8-Month High on Iran Tension, Shrinking Supply

- Aldar’s May 2014 Bond Yield Drops to Record on Asset Sale

- Arabtec Wins 561 Million Dirhams Contract at Dubai Airport

- Saudi Arabia May Cut Oil Premiums for February From Record Highs

- Iran’s Nuclear Fuel Rod Isn’t Military Threat, U.S. Analysts Say

- Dana Gas Bond Yield Jumps Most in Two Weeks Ahead of Meeting

- OPEC Crude Production Rises to Three-Year High, Survey Shows

- Kuwait Oil Tanker Will Award Contracts to Daewoo, Al-Anba Says

- Gold Rallies Most in 10 Weeks on Iran, Dollar; Wien Sees $1,800

- Biggest Hedge Fund in Ships Sees Frozen Gas Beating Oil: Freight

- Jarir Fourth-Quarter Profit Jumps 21% on Phone, Laptop Sales

The Hedgeye Macro Team

Howard Penney

Managing Director