This note was originally published at 8am on December 29, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“If you can’t explain it simply, you don’t understand it well enough”

– Albert Einstein

For some reason, finance and science maintain a rather unique fascination with generating overly complicated and confounding verbiage to describe fairly straightforward and pedestrian concepts. In my 30 years, I have had the lamentable pleasure of being a professional in both vocations.

Before joining HEDGEYE, I was a molecular biophysicist. I’m still not sure I can tell you exactly what that is, but it sure sounds impressive. I’ve also been a dishwasher, business owner, carpenter, physiologist, bartender, Ph.D researcher, industrial sheet metalist, and successful self-taught trader. Wandering philanderer? I like to think of it as Generation Y’s version of a renaissance man.

Across disciplines, many times a process that, superficially, appears complex is really only the summation of a series of simple questions asked and answered. The trick, of course, is in asking the right questions and then having the ability to successfully source the correct data as inputs for the model.

In finance and science, it just so happens that the canonical blueprint for increasing scarcity values calls for the addition of unnecessary technical jargon and intentional obfuscation of the details around the process in a way that makes the output appear overtly complex and thus, through the trappings of behavioral psychology, more desirable.

So, as the edifice of Wall street 1.0 has continued to implode under the weight of institutionalized, levered conventions of its own creation, on the healthcare research side, we’ve been working to develop an investment research process that successfully functions outside of the legacy construct of management one-on-one’s, recycled expert opinion, and valuation-in-isolation and intuition driven decision making.

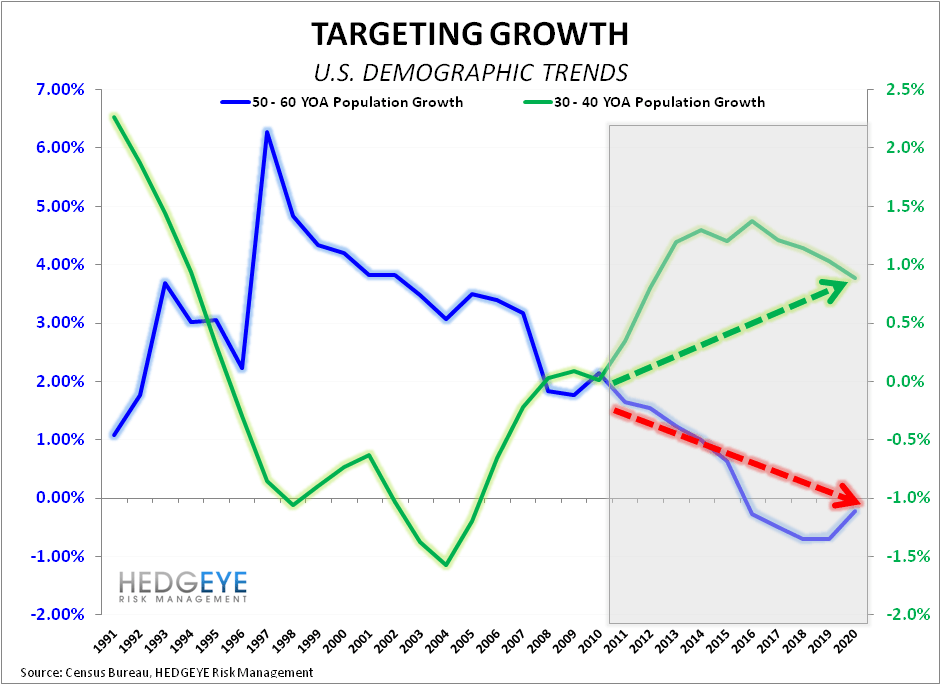

At the heart of the HEALTHCARE MACRO modeling effort has been the analysis and integration of government data sets which have proven effective in helping us create a quantitative, independent, and thus far, successful process for tracking real-time consumption across the health economy broadly and major sub-industries specifically. Longer-term, healthcare consumption growth continues to be defined by domestic demographic trends.

From a macro level, understanding how this approach functions from a practical investment research perspective can be explained fairly simply. Broadly speaking, the consumption curve for healthcare services across the age continuum is fairly static with elastic demand occurring largely at the margin. Given fixed census trends, if one is able to determine per capita consumption by age for a particular procedure or service type, a reasonable estimate for the underlying growth trend can be derived.

Having a quantifiably justified estimate for underlying organic growth, finding higher frequency data sets that accurately reflect real-time demand and solving for the shorter-term impacts of larger, more acute factors such as employment/insurance status makes it possible to both identify and forecast cyclical growth inflections as well. Conviction is found where the demographic, per capita consumption by age, and the higher frequency macro data function to drive company model inputs that back test with strong correlations across durations.

Taking a TAIL perspective on the healthcare sector, as an example, let’s take a short walk down demography lane and examine the consequences of the existent, secular domestic demographic shift and some of the resulting longer-term investing implications.

Given that the consumption curve for healthcare services across age buckets remains relatively fixed, the glacial movement of U.S. demographic trends holds specific consequences both for healthcare and the larger economy broadly. Therefore, it is important to understand that the period of greatest acceleration in per capita healthcare consumption comes as people age into their 50’s. Equally important is the fact that this 50-64 year old subset is covered, in large part, by high margin, commercial insurance.

The largest acceleration in medical consumption in combination with high margin insurance, places the 50-64 year old demographic as the heart, and profit center, of the health economy. This demographic is now in a secular decline (although the continued acceleration in employment for this age bucket remains a near-term positive for healthcare consumption). In fact, extending current census trends and per capita healthcare consumption by age out over the coming decades reveals a secular bear market for healthcare that won’t see its trough until 2024!

This trend has definite and specific consequences for the hospital industry as well. With roughly 30 cents of every healthcare dollar flowing through the hospitals, the industry sits at the heart of the healthcare economy and is inextricably beholden to meaningful shifts in utilization and service consumption growth.

At present, the current demographic setup is one which will see the 45-64 year old age group graduate into Medicare at a faster rate than those underneath can fill the void. In other words, the spread between those aged 45-65 and those aged 65-85 will reach its narrowest point in 2011 before embarking on a protracted expansion where hospital margins will face a secular decline as negative margin Medicare volumes grow faster than commercial admissions.

In this scenario, we continue to believe high-tech, med-tech remains the relative loser as hospitals focus cost initiatives across controllable supply expenses. ZMH remains our favorite long-term short in the space.

The outlook isn’t completely dismal, however. The 30-40 year old demographic will continue to accelerate for the better part of the next decade. Here, women’s health and companies levered to birth volumes remain favorably positioned to benefit from this secular trend. Moreover, women’s health, along with dental and domestic U.S. physician office exposure, continues to sit positively across a number of our strategic TRADE & TREND themes as well.

(Please email sales@hedgeye.com for more on our ZMH specific fundamental and demographic work, additional detail on where we’re targeting long exposure, or further detail on how we marry the HEALTHCARE MACRO process with our fundamental, company research.)

As the transparency curtain gets pulled further back on the collective global balance sheet, staring into the mirror of a leveraged overconsumption past will continue to reveal some painful realities. Growth will remain impaired as developed economies deal with structural debt/deficit issues. Beta will continue to auger to the latest centrally planned headline, and government intervention will continue to sponsor market volatility.

And while Euro & Bureau – Crats continue to hold summits and engineer soundbytes in a flagging attempt to placate markets looking for tactical solutions to structural problems, we’ll continue to evolve our own process.

It’s not perfect, but it has worked a lot more than it hasn’t – and it’s repeatable.

Buy Low. Sell High. Repeat. Pretty Simple.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, Italy’s MIB Index, and the SP500 are now $1537-1568, $106.01-107.93, $1.28-1.30, 14,466-15,094, and 1240-1260, respectively.

Christian B. Drake

Analyst

Hedgeye Healthcare