This note was originally published at 8am on December 22, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“… every job created by the government would add a further job to supply that new worker with goods.”

-Nicholas Wapshott (Keynes Hayek, pg 58)

John Maynard Keynes had more personal and P&L issues over the course of his career than Time Magazine. His biggest losses (both in terms of academic credibility and in his personal account) came in the late 1920s when “corporate profits were good” and debauching the British Pound came to an end.

Sound familiar? It’s a good thing they don’t let Bernanke trade his p.a.

The aforementioned quote comes from a passage in Keynes Hayek where Nicholas Wapshott does a nice job reminding us of the context of Keynes’ big marketing idea for Lloyd George going into the 1929 British Election. The idea, much like the central planning ideas of Big Government Liberals today, was to “stimulate” economic growth via government spending.

The Liberals lost that 1929 election (the Conservative Party’s Ramsay MacDonald formed a minority government), and like most politicized people who can’t get paid putting their own capital at risk, John Maynard Keynes, “ever the pragmatist...” (Wapshott), pulled a Bernank and shifted his central planning ideas to the other party line.

“This marked the end of Keynes’ long dalliance with the Liberals.” He “… now directed his energies toward persuading the new government to accept his prescriptions.” (Keynes Hayek, pg 58)

*Note: Since 1929, while tested and tried by Charles de Gaulle (France in the 1950s), and Jimmy Carter (USA late 1970s), the Keynesian concept of the Multiplier Effect has not worked.

Back to the Global Macro Grind…

There was one big thing that changed yesterday that had me thinking about the 1928-1929 narrative of “but corporate profits are good and stocks are cheap” consensus – Oracle trading down -14% on the open.

Oracle isn’t exactly a small company ($130B in market cap – only about 20% of the size of yesterday’s LTRO leverage slapped onto insolvent European bank balance sheets). It’s also a company whose revenues are highly correlated to the corporate profit cycle.

Yes, a blind intellectual squirrel can tell you what corporate profits are, after they’ve occurred. But how many of the gargantuan intellects in our profession can tell you when the Global Growth and Profit Cycle is about to slow?

Not a trick question.

The answer, last I checked, on who nailed both the 2008 and 2011 Global Growth Slowdowns, is, not many.

How do we translate this thought about investing at the Top Of A Corporate Profit and Margin Cycle to our daily risk management positioning?

Well, the market has already started to do that for you. Look at the S&P Sector Returns for the YTD:

- Utilities (XLU) = +13.4% YTD (lead the market higher yesterday, closing +1.6%)

- Technology (XLK) = -0.7% (lead the market lower yesterday, closing down -1.7%)

- Financials (XLF), Basic Materials (XLB), and Industrials (XLI) = -19.8%, -13.4%, and -4.1% YTD, respectively.

In fact, the market has been telling you what we’ve been telling you on Global Growth Slowing since February – so this is not new. Neither is Utilities (dividends) moving into a raging bull market if we are on the cusp of what ISI’s Ed Hyman called for earlier this week (a Q4 surge in US GDP to 4%?).

Fortunately, the bond market has figured this out. Hyman actually taught me that, so I don’t get why he’s not following his own leading indicator process. Long-term US Treasuries (which we’ll be buying more of today and tomorrow, and really until the math tells us not to) remain in a bull market of their own.

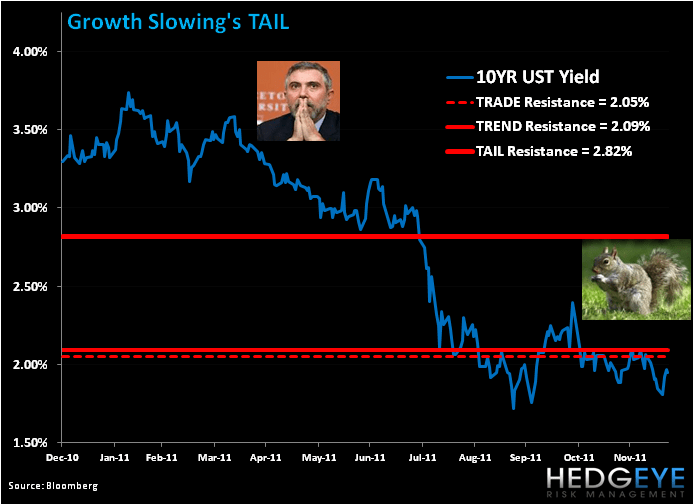

Across all 3 of our risk management durations, both 10 and 30-year UST Bonds are in what we call a Bullish Formation (yields are in a Bearish Formation) with TRADE, TREND, and TAIL lines of resistance for the 10yr at 2.05%, 2.09%, and 2.82%, respectively.

Now before my Ivy League classmates who are endowed with the high powers of determining “valuation” better than I start yelling at me this morning that “stocks are cheap relative to bonds,” I’ll just take a moment to whisper, softly, in their 2011 ears… the market doesn’t care about what you think is “cheap”… it’s getting cheaper…

The corollary, of course, to where US Government Bonds can go in a Growth Slowing environment that is perpetuated by the piling of debt-upon-debt is Japanese Government Bonds (or JGBs).

Looking at last night’s reported non-resident holdings of JGBs as a proxy for TLT demand (long-term US Treasury ETF), they hit a new all-time record of 76 TRILLION Yen. That’s a lot of yens. And 15 years after Paul Krugman told them to “PRINT LOTS OF MONEY and stimulate”, Japan is still waiting for the Multiplier Effect to reach “escape velocity”…

My immediate-term support and resistance ranges for Gold (shorted it yesterday), Oil (Brent), German DAX, French CAC, Shanghai Composite (down every day this week), and the SP500 are now $1568-1623, $106.03-109.16, 5803-5901, 3059-3118, 2152-2341, and 1228-1259, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer