TODAY’S S&P 500 SET-UP – December 20, 2011

Plenty going on out there in the world – we just need to keep refining a repeatable risk mgt process to absorb it: 1207 holding in the SP500 is critical. We’ll see what the bulls have left to keep it treading water – inflows are dead. As we look at today’s set up for the S&P 500, the range is 20 points or -1.02% downside to 1193 and 0.63% upside to 1213.

SECTOR AND GLOBAL PERFORMANCE

Markets wait for no one. Unfortunately, they don’t take vacation – and have a not so funny way of imposing the most amount of pain on the most amount of people in short windows of time. With the SP500 down -3.3% for December to-date, today’s break of our intermediate-term TREND level (1207) is an explicit warning signal.

Holding below 1207 needs to be confirmed by at least 3 trading days (on a closing basis), but it’s important to note that the last time we snapped the TREND level, moving the SP500 into a Bearish Formation (bearish across all 3 of our risk management durations - TRADE, TREND, and TAIL), was in mid-July.

The good news is that 5 of 9 Sectors did not confirm today’s TREND Break in the SP500 (Utilities, Consumer Staples, Consumer Discretionary, Healthcare, and Industrials). The bad news is that Tech joined Financials, Basic Materials, and Energy today, moving into a Bearish Formation. So watch Tech closely from here.

Strong Dollar = Strong Consumption. That beat beta today, but still reminds me it can lose money on down days if beta is bad enough.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1742 (-2463)

- VOLUME: NYSE 774.69 (-56.69%)

- VIX: 24.92 +2.59% YTD PERFORMANCE: +40.39%

- SPX PUT/CALL RATIO: 1.60 from 1.36 (+17.76%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 56.69

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 1.82 from 1.86

- YIELD CURVE: 1.58 from 1.62

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 8:30am: Housing starts, Nov., est. 635k, up 1.1% (prior 628k)

- 8:30am: Building permits, Nov., est. 635k, down 1.4% (prior 644k (revised)

- 11:30am: U.S. to sell $30b 4-week Bills

- 1:00pm: U.S. to sell $35b 5-yr notes

- Germany - Jan GfK consumer sentiment 5.6 vs consensus 5.5, prior 5.6

- Nov PPI +5.2% y/y consensus +5.2%, prior 5.3% Dec IFO business climate 107.2 vs consensus 106.1, prior 106.6 current conditions 116.7 vs consensus 116.0, prior 116.7 expectations 98.4 vs consensus 97.0, prior 97.3

- European Automobile Manufacturers' Association (ACEA) Nov Commercial Vehicles Registrations in the EU +8.4% y/y

WHAT TO WATCH:

- HTC said it would work around a U.S. ITC ruling after Apple won a patent-infringement judgement; Bernstein says Apple victory won’t lead to disruption

- ITC judge to issue decision in Microsoft patent-infringement case against Motorola Mobility, 5pm

- Explosion at Shanghai supplier to Apple injured 61 workers after aluminum dust produced by polishing cases for iPads ignited, China Labor Watch said

- House Republicans poised to force impasse over payroll tax cut; House meets at 9am

- Gingrich in Iowa, Romney in N.H.

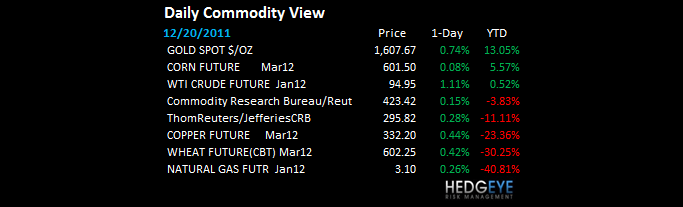

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – Bearish is as bearish does; provided that the USD holds my most immediate-term TRADE line of $79.68 support, I see Brent Oil making lower-highs on bounces within a newly established Bearish Formation (TAIL resistance = $110.12/barrel). This read through is wrecking Russia; down another -1% this morning, sending the RTSI to -36.2% since the Bernanke USD debauchery low (April 2011)

- Yanzhou Said to Plan $2 Billion Purchase of Gloucester Coal

- Australia Weathering Europe Recalls 2009 Resilience: Economy

- Silver Puts Rise to Highest Ever After Dollar Rally: Options

- Oil Climbs for a Second Day on U.S. Crude Supply, Iran Outlook

- Recession Risk Beats Fukushima in German Power: Energy Markets

- Tanker Bear Market Worst Since ’90s as Owners See Loss: Freight

- Gold Gains as Drop Spurs Purchases, Offsetting Dollar Strength

- Stocks Fall on Debt Crisis Concern as Treasuries, Dollar Advance

- Sino-Forest Defaults on Two Bond Issues, Seeks Waivers

- Investors in ‘Fetal Position’ as Goldman Sees Rally: Commodities

- Copper Climbs as U.S. Growth Forecast Boosts Optimism on Demand

- Eldorado Drops Amid $2.4 Billion Bid for European Goldfields

- Oil Advances as North Korea, Iran Bolster Geopolitical Tension

- Uranium Prices Decline 0.9% as Spot Market Winds Down, Ux Says

- Palm Oil Drops for First Day in Three on Weaker Export Demand

- Copper Gains as Europe Plan, U.S. Growth Forecast Fuel Optimism

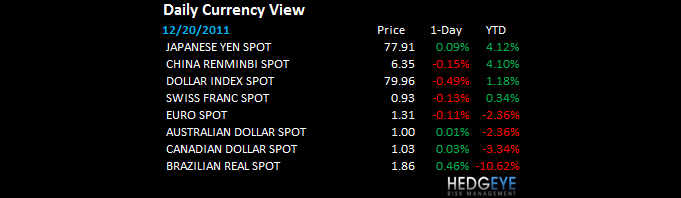

CURRENCIES

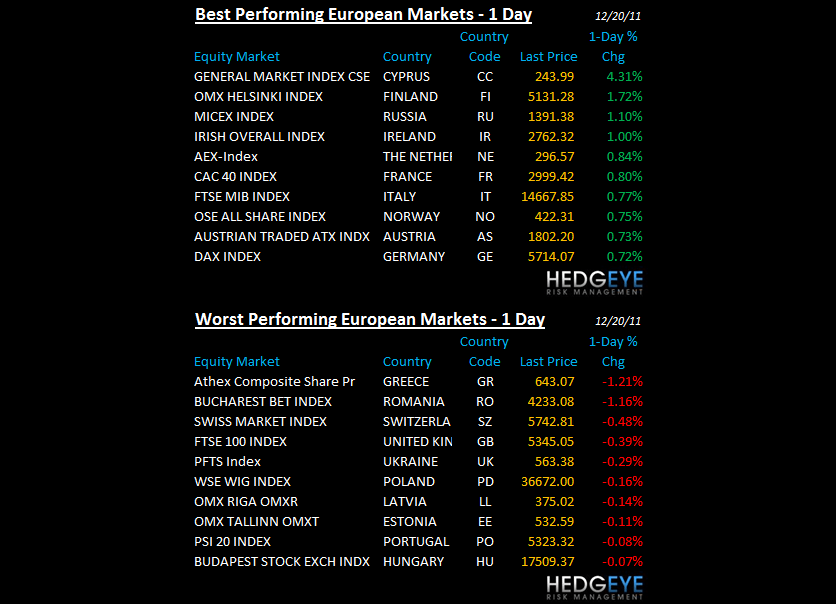

EUROPEAN MARKETS

FTSE – Steiner highlighted this in our morning meeting yesterday and it appears that the market continues to care about it this morning – capital charges on British banks – gives the FTSE and Swiss Market Index negative divergences vs the region this morn despite the Swedes cutting rates by 25bps to 1.75% (Sweden gets the + divergence for the morning, up +0.8%)

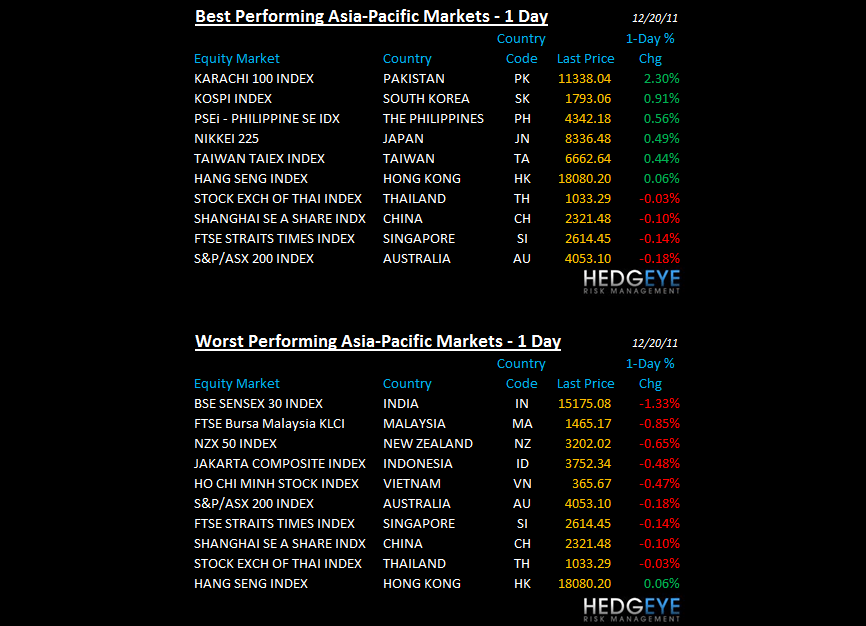

ASIAN MARKETS

KOREA – I learn a lot more about a bear market on the bounces than you do on the down moves – the KOSPI’s -3.4% drop on the “news” was met w/ a +0.91% bounce overnight (you’d need a +3.7% move to get back to breakeven); much like the rest of Asia which was weak again (India down another -1.3%, crashing to -26% YTD), South Korean Industrial and Tech demand continues to slow

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Oil Climbs for a Second Day on U.S. Crude Supply, Iran Outlook

- Saudi Border Guards Chase Smugglers as Yemen Unrest Spurs Exodus

- Indonesia Sukuk Poised to Beat Malaysia in 2012: Islamic Finance

- Drydocks World Sees $2.2 Billion Debt Restructuring in March

- Saudi British Bank Ratings Reviewed for Downgrade at Moody’s

- Emaar Raises $980 Million Financing to Extend Maturities

- Oil Advances as North Korea, Iran Bolster Geopolitical Tension

- Saudi King Abdullah Calls for Closer Arab Union at GCC Summit

- Twitter Gets $300 Million From Alwaleed Amid Website Revamp

- Emaar Rises Most in a Week After $980 Million Financing Facility

- Iranian Oil Halt Would Boost Oil by $40 a Barrel, BofA Says

- Iran Pumps Less Crude Oil as Investors Grow Scarce, ISNA Says

- Etihad Takes 29.2% Stake in Air Berlin, Squeezing Lufthansa

- Qatar Plans to Invest Up to $2b in Financial Services, FT Says

- Moody's places Saudi British Bank's Aa3/C+ ratings on review for

The Hedgeye Macro Team

Howard Penney

Managing Director