Keith just shorted Buffalo Wild Wings in the Hedgeye Virtual Portfolio. From a fundamental perspective, this is one of our favorite names on the short side.

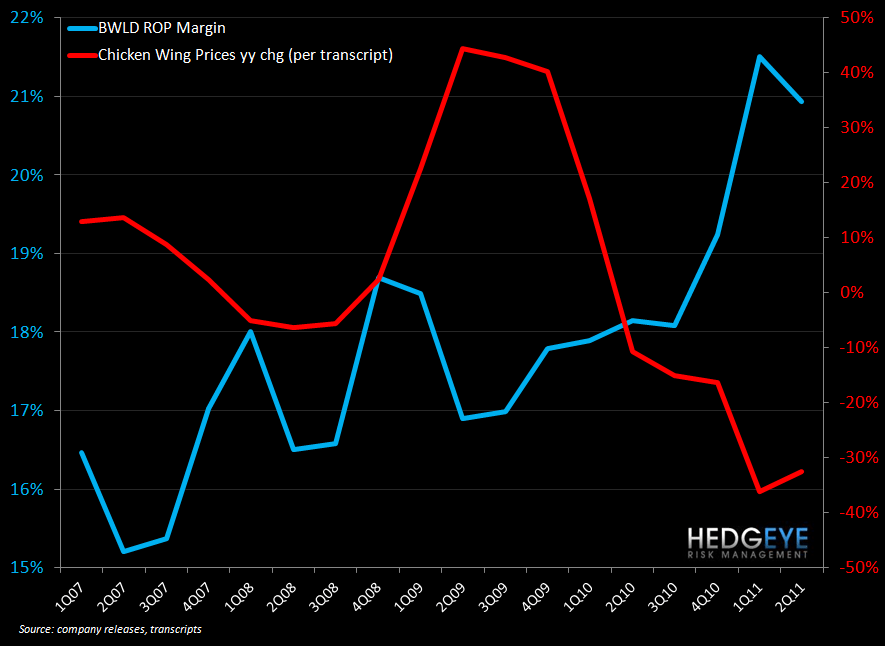

Buffalo Wild Wings’ share price has popped nicely today on a sell-side upgrade. We have not seen the report but were told that EPS numbers for the next two quarters and the year were being reduced but the price target was being raised from $63 to $78. Again, we have not seen the report so cannot refute it directly but our thesis remains intact; chicken wing prices are heading higher (already north of $1.40/lbs) and that means the promotional strategy the company has implemented to drive sales will not be viable in 1Q12 when wing prices are likely to be up roughly 50-60% year-over-year. The Street is modeling a moderate price increase that we believe is far too low. Margins are almost certain to come down under the wing price scenario we are anticipating.

From a quantitative perspective, BWLD is nearing its TREND line of resistance at $62.69. See the chart below.

Howard Penney

Managing Director

Rory Green

Analyst