Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.

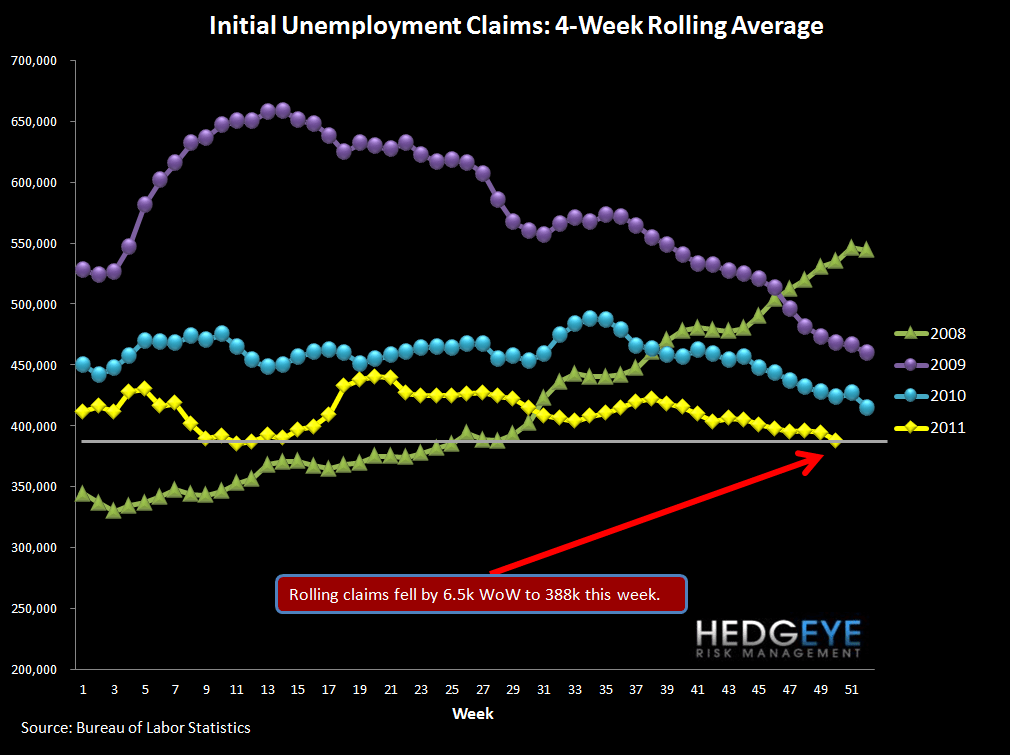

Initial Claims Drop 15k

The headline initial claims number fell 15k WoW to 366k, the lowest level seen since early 2008 (down 19k after a 4k upward revision to last week’s data). Rolling claims fell 6.5k to 388k. On a non-seasonally-adjusted basis, reported claims fell 96k WoW to 433k.

On its face, this is a very strong print. No seasonal factors were noted by the Labor Department. However, year-end volatility is not unusual, which leaves us modestly cautious. See the third chart below for the non-seasonally-adjusted series by year.

We’ve previously identified 375k – 400k as the claims range where unemployment can begin to improve. Initial claims printed below the bottom end of our range this this week, and has been printing near or below the 400k level for almost a month. This begins to create a tailwind behind unemployment improvement.

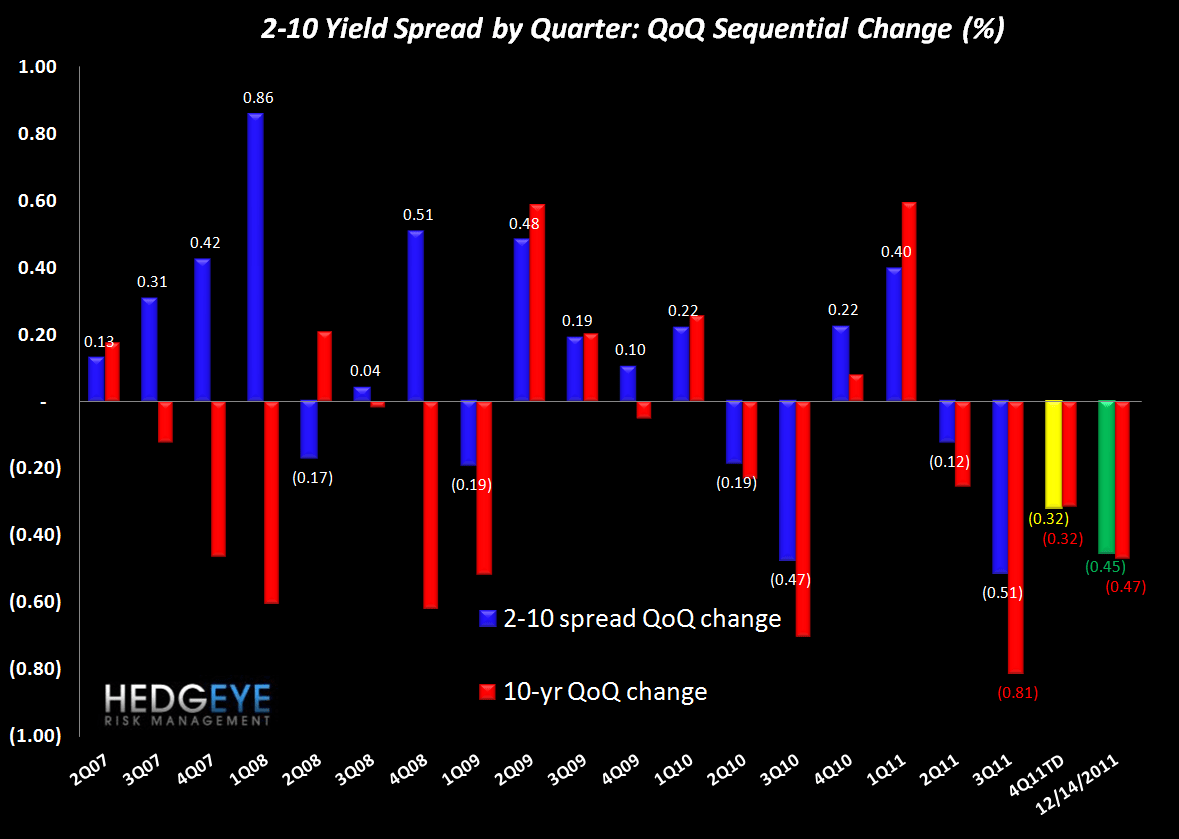

2-10 Spread

The 2-10 spread tightened 12 bps versus last week to 167 bps as of yesterday. The ten-year bond yield fell 13 bps to 190 bps.

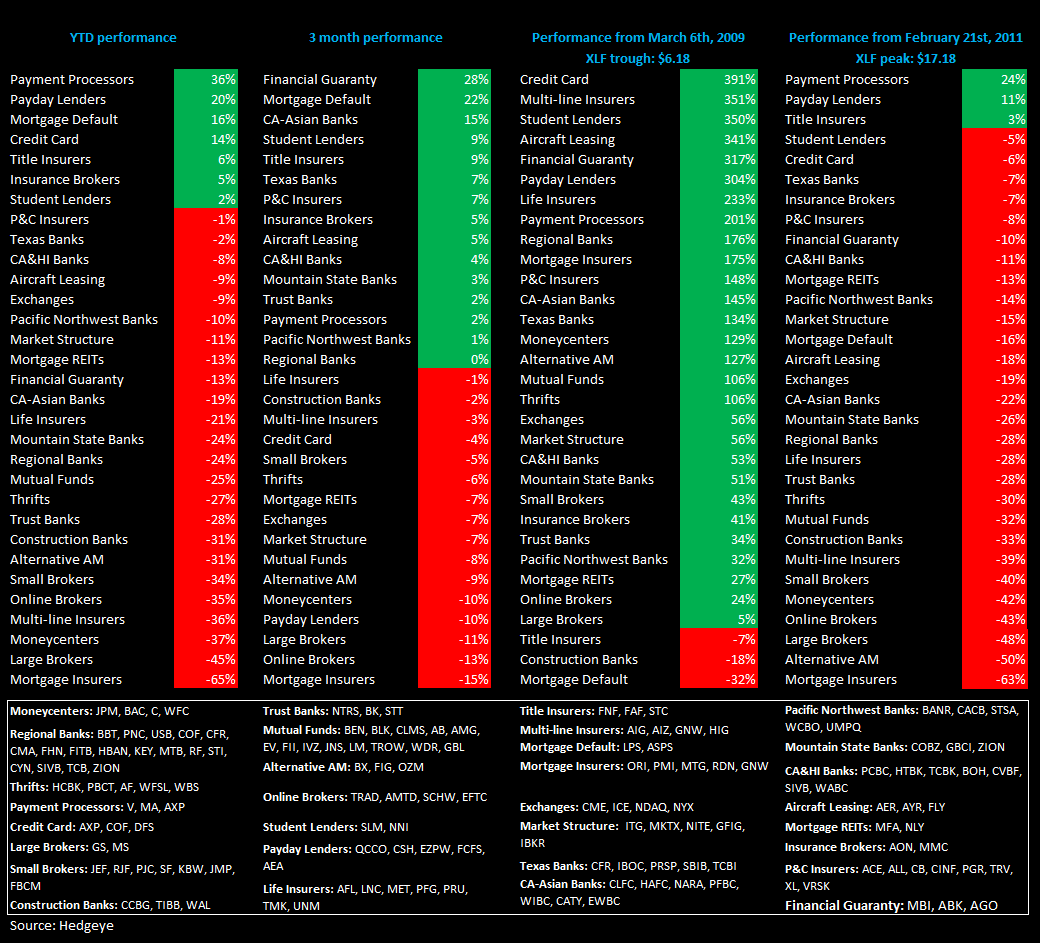

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.