“There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency.”

-John Maynard Keynes

If you study the history of John Maynard Keynes and his economic ideas, experiments, and failures, you’ll come to a very simple conclusion – he was a world class storyteller, not a Risk Manager.

Before he became politically conflicted and compromised (in his early 40s), Keynes had it absolutely right on what debauching a currency functionally does to a society. After World War I, the policies to inflate across Eastern Europe made that crystal clear.

Ironically enough, explaining this in the 1stbook to make him world famous – The Economic Consequences of Peace (1919) – is what made Keynes popular with the Austrian, German, and Russian people:

“Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency”, wrote Keynes. “By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens.” (Wapshott’s Keynes Hayek, page 22).

Tomorrow at the FOMC meeting, someone should ask Ben Bernanke what he thinks about that.

Back to the Global Macro Grind…

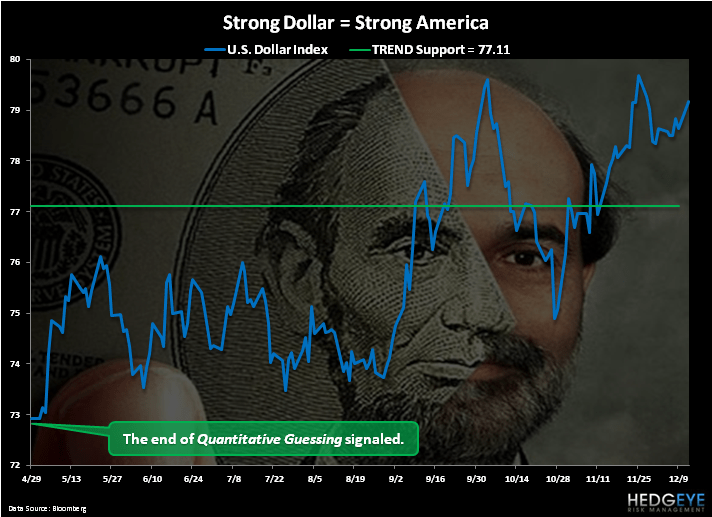

I call out this linkage between currency and inflation this morning because last week’s stabilization of the US Dollar continues to improve not only my outlook on the US economy but the Consumer Confidence within it. US Consumption, don’t forget, represents 71% of US GDP.

Closing flat week-over-week at $78.63, the US Dollar Index has gained +7.6% since Ben Bernanke signaled the end of Quantitative Guessing II. We’ve called it guessing, because that’s what it was – a guess that a second stock and commodity market inflation could magically boost the US economy into what Bernanke calls “escape velocity.”

On the two mandates that he is scored on – full employment and price stability – guessing didn’t work out for him.

What has actually worked quite well for Bernanke is getting out of the way. Since the elixir of QE3 hope has been temporarily removed from the almighty table of letting losers win, 3 big things have materialized:

- Strong Dollar

- Deflating The Inflation

- Rising Consumer Confidence

Last week’s preliminary December reading on US Consumer Confidence from the University of Michigan improved again, sequentially, to 67.7 (versus 64.1 in November). It’s not a great reading. But it’s certainly better than bad.

Last week’s Deflating The Inflation (Hedgeye Macro Theme from Q311) was also additive to US Consumer Purchasing Power:

- CRB Commodities Index (basket of 19 commodities) = -2.2% week-over-week

- Oil Prices (Brent and WTIC blended avg) = -1.2% week-over-week

- Gold and Copper = -2.0% and -0.8% week-over-week, respectively

Just as an fyi, most Americans don’t have enough money to buy an ounce of Gold, nor should they if their outlook is in line with Hedgeye’s for a potential US Dollar appreciation of another +5-10% higher from here.

That’s not to say we don’t want you to own some gold. That’s just a friendly reminder that the idea is to buy low, not high. Gold’s intermediate-term TREND line of resistance remains overhead at $1743/oz and there is no long-term TAIL support to $1568/oz.

Back to what Strong Dollar means for America…

- Stronger Employment

- Stronger Consumption

- Stronger Society

If you can have a Keynesian refute Keynes’ view of the same to me, just tweet me @KeithMcCullough.

My immediate-term support and resistance ranges for Gold, Oil (Brent), and the SP500 are now $1, $107.11-109.55, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer