Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.

Initial Claims Drop on Seasonal Factors

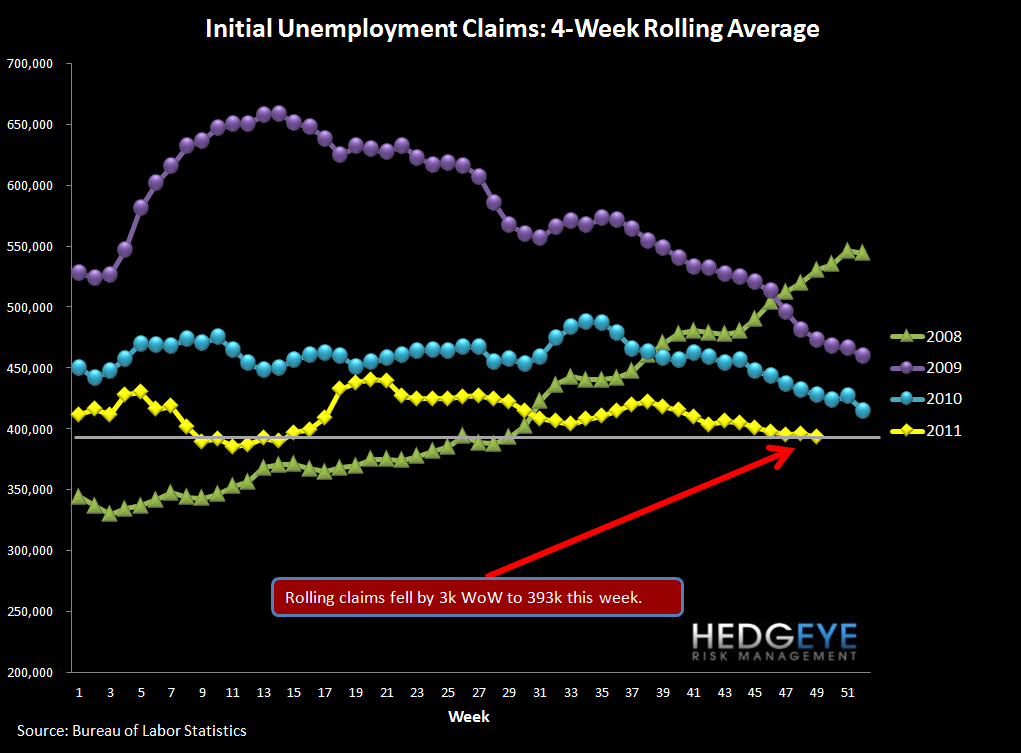

Initial claims dropped 23k last week to 381k, one of the best improvements in months. Unfortunately, like the last eye-popping decline in claims (the week ended September 23rd), this one also looks too good to be true. The Labor Department noted that seasonality is generally problematic this week of the year. A typical seasonal increase is 182k, and claims actually increased only 151k. Because the seasonal adjustment factor drives such a large piece of the data this week, it's difficult to take today's print at face value. We would require several more weeks of confirming data to get more positive.

We’ve previously identified 375k – 400k as the claims range where unemployment can begin to improve. A sustained period below 400k would be meaningful for unemployment.

2-10 Spread

The 2-10 spread tightened 3bps versus last week to 179 bps as of yesterday. The ten-year bond yield decreased 4 bps to 204 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.