THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Employment

The unemployment rate fell to 8.6% in November versus 9.0% consensus. The Labor Force Participation Rate fell to 64% from 64.2% in October. The unemployment rate for teenagers aged 16-19 years dropped to 23.7% from 24.1%. Nonfarm payrolls came in at 120k versus 125k consensus and average hourly earnings declined -0.1% MoM versus +0.2% consensus.

Beef Costs

According to an article on cattlenetwork.com, now is one of the best times to be in the cattle business. According to Randy Black of Cattle-Fax, “this is the first year in history the U.S. has been a net beef exporter.” For restaurant companies with exposure to spot market beef, this is not good news for margins.

Notes from CEO Keith McCullough

Fed sponsored Dollar Debauchery this week has its reflation perks – don’t mistake it for growth:

- CHINA – unfortunately, the Chinese economy doesn’t like the commodity inflation – this only compounds the already accelerating deceleration in sequential (Q4 vs Q3) Asian and European growth. China closed down another -1.1% overnight, right back to where it was pre the rate cut.

- BRAZIL – fortunately, the Bovespa is linked to inflation (Petrobras, etc) and is one of the ways to get long of Bernanke getting pushed around by the Germans and the French on bank blow up fear. We’re not long the EWZ yet, but likely will be on a pullback – the Bovespa is down -16% YTD but trading above its TREND line of 55,378 as Brazil cuts rates and taxes.

- COPPER – the Doctor looks exactly like European Stoxx because they have the same correlation to the USD. Copper climbs back above its immediate-term TRADE line of resistance this week of 3.47/lb and remains under TREND line resistance of 3.72/lb. Pick your European stock market and the TRADE/TREND setup is the same. Trade the new ranges.

US Futures spikey as short sellers are now in Pain Trade mode while the long-onlys chase beta. Always a powerful combo in the immediate-term – also the biggest downside risk after the immediate-term squeeze makes a lower-high. My refreshed SP500 range = 1.

KM

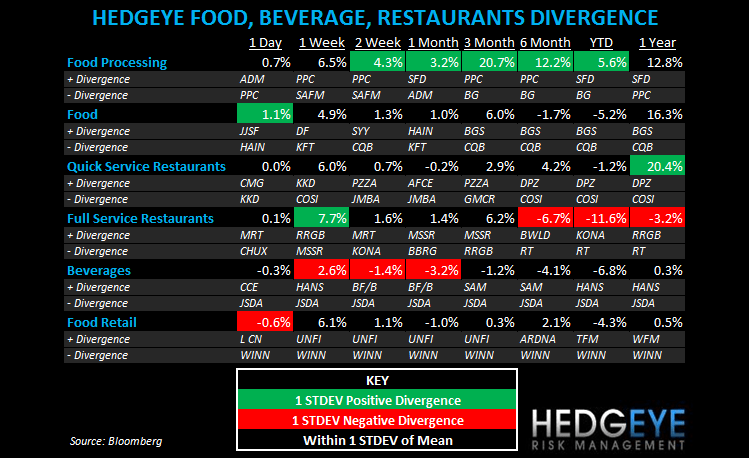

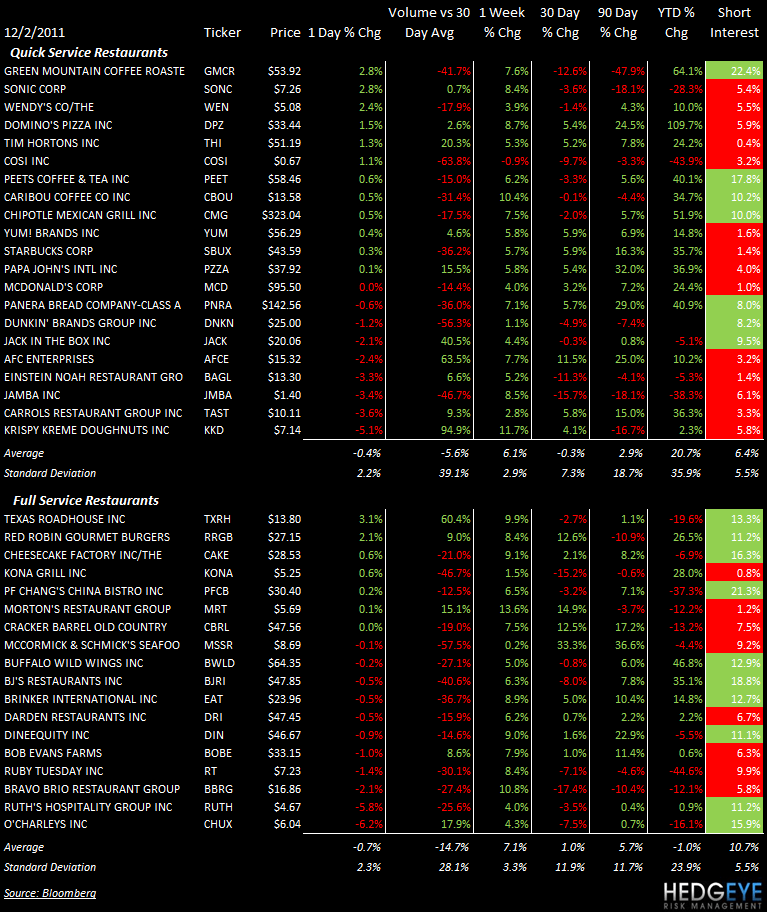

SUBSECTOR PERFORMANCE

QUICK SERVICE

DPZ: Domino’s Pizza was initiated “Hold” at KeyBanc.

WEN: Wendy’s announced plans to consolidate its World HQ in Dublin, Ohio. Wendy’s said that it has 200-210 employees in the Atlanta office right now and that most Atlanta-based employees will be offered relocation. 30-40 jobs, according to the company, are redundant and may be eliminated.

GMCR: Green Mountain Coffee Roasters was raised to “Outperform” at William Blair.

SBUX: Starbucks is set to create 5,000 jobs in the UK as it opens 200 more drive-through stores across the country.

KKD: Krispy Kreme same-store sales gained 4% in the third quarter. EPS came in at $0.35 versus $0.41.

CASUAL DINING

DIN: Dine Equity was initiated “Neutral” at Janney Montgomery. The twelve-month price target is $45.

CBRL: Cracker Barrel reported November sales metrics yesterday. Comparable restaurant traffic was down -1.0% while average check gained 2.2% to leave the overall comp at +1.2% for the month. Comparable retail sales were up +2.7%.

EAT: Chili’s features in an article on NRN.com today describing the “kitchen of the future”. We have been bullish on this name for some time and remain so following store visits this week.

Howard Penney

Managing Director

Rory Green

Analyst