Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser

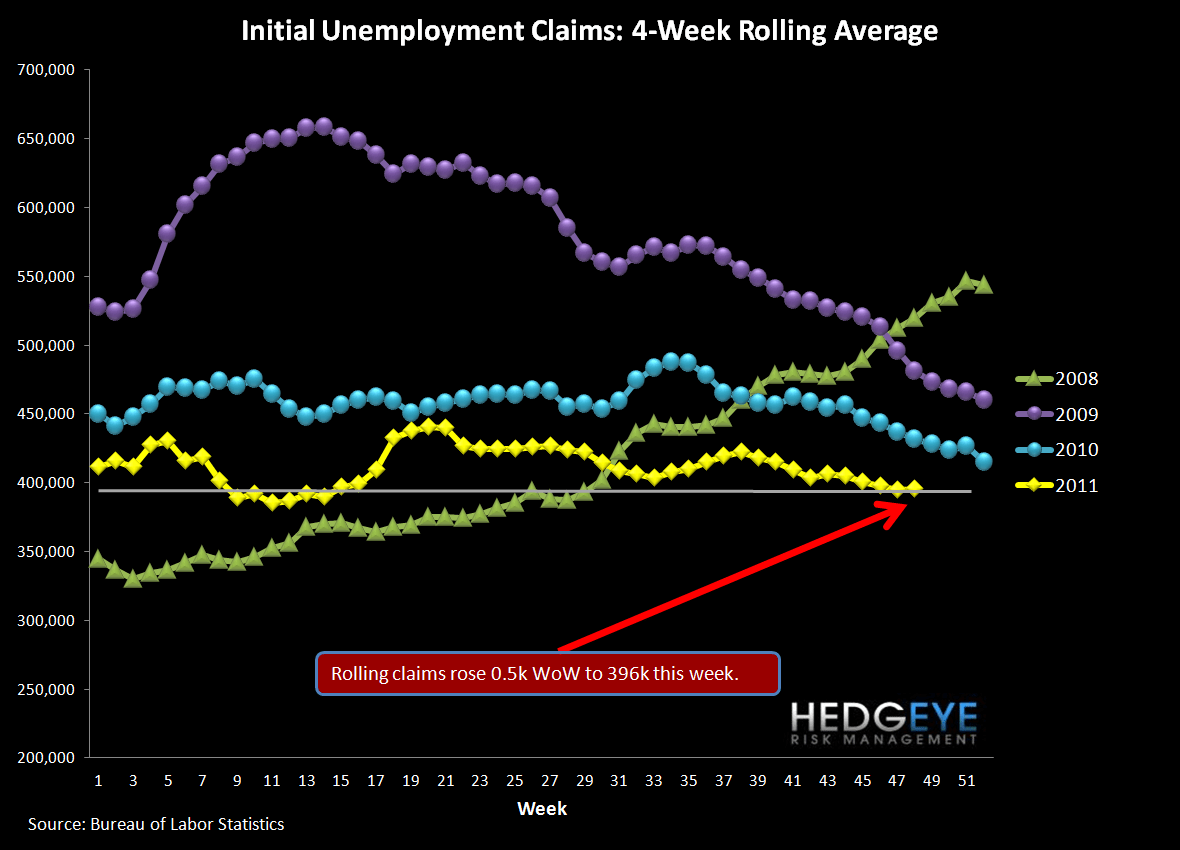

Initial Claims Rise for the Second Week

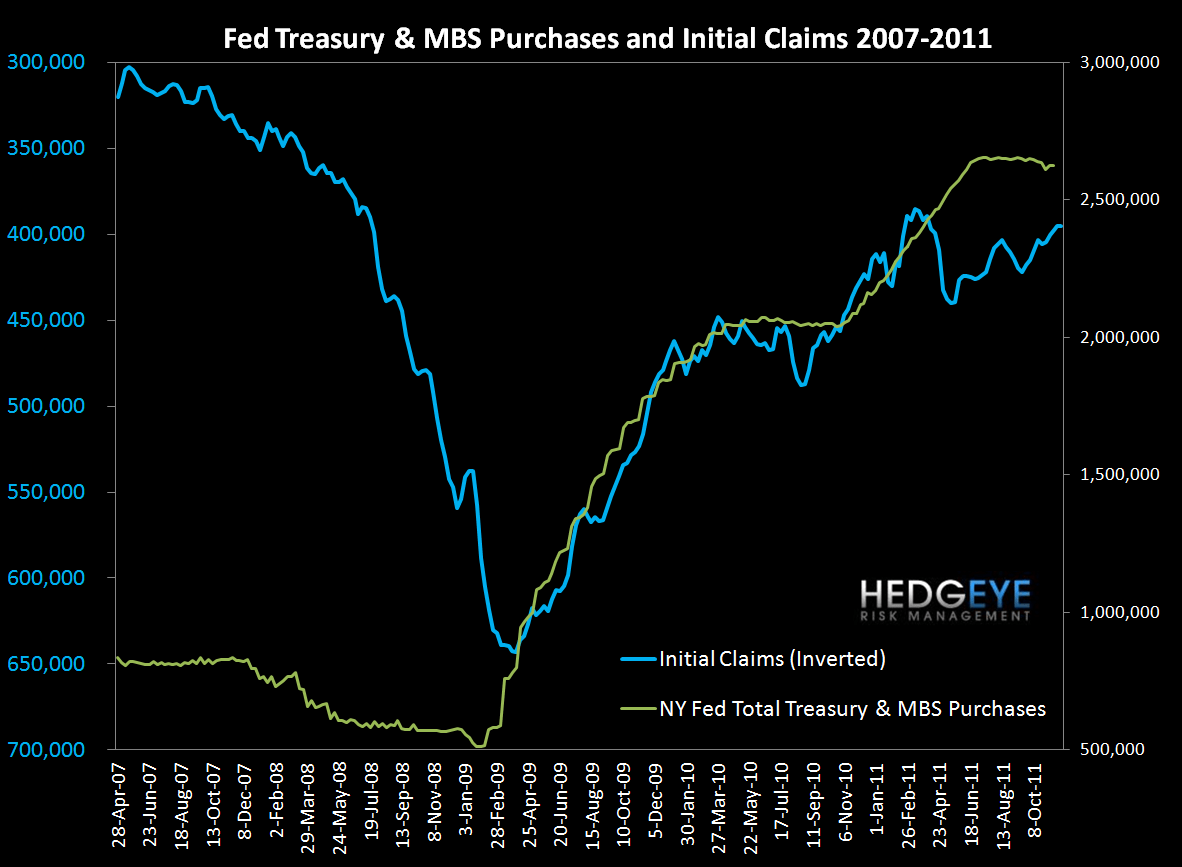

The headline initial claims number rose 9k WoW to 402k (up 6k after a 3k upward revision to last week’s data). Rolling claims rose 0.5k to 396k. On a non-seasonally-adjusted basis, reported claims fell 70k WoW to 371k for the week of Thanksgiving.

We’ve previously identified 375k – 400k as the claims range where unemployment can begin to improve. After coming in within that range for 2 weeks in a row, claims printed slightly above the 400k level. A sustained period below 400k would be meaningful for unemployment.

2-10 Spread

The 2-10 spread widened 15 bps versus last week to 182 bps as of yesterday. The ten-year bond yield increased 15 bps to 208 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser