TODAY’S S&P 500 SET-UP - November 30, 2011

Month-end is finally out of the way. Not a good month for most things other than the USD and Long-term Treasuries. We have seen 2 down days for the USD, 2 up days for Global Equities = Correlation Risk.

As we look at today’s set up for the S&P 500, the range is 56 points or -4.03% downside to 1147 and 0.65% upside to 1203.

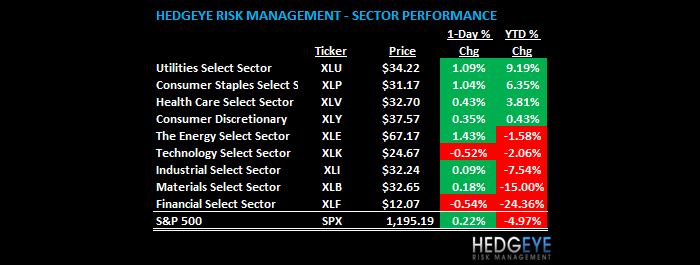

SECTOR AND GLOBAL PERFORMANCE

Putting today’s 2ndconsecutive failure to overcome the S&P line of intermediate-term TREND resistance in context is critical: A) it was only the 2ndup day for US stocks in the last 9, and B) the SP500 is down -4.6% for November.

For the immediate-term TRADE (3 weeks or less) it’s also important to bear in mind the draw-down risk associated with the first 6 days of the new month. Since May, the first 6 days have averaged close to -400bps. Not perpetual. But not good either.

That’s one of the many globally interconnected reasons why only 1 of 9 Sectors are bullish on my immediate-term TRADE duration (Consumer Staples - XLP). Financials (XLF) continue to look awful – down -24.4% YTD and crashing. Followed closely by Basic Materials (XLB) which are down -15.0% for the YTD and that Sector could very well be the worst on the next US Dollar up day. Hedgeye is long Healthcare (XLV) and short (SPY).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -110 (-2154)

- VOLUME: NYSE 918.43 (-4.19%)

- VIX: +30.65 -4.64% YTD PERFORMANCE: +72.62%

- SPX PUT/CALL RATIO: 2.07 from 2.71 (-23.63%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 51.17

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.00 from 1.97

- YIELD CURVE: 1.74 from 1.74

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage, (prior -1.2%)

- 7:30am: Challenger job cuts (prior 12.6%)

- 8:15am: ADP Employment, est. 130k (prior 110k)

- 8:30am: Non-farm productivity, est. 2.5%, prior 3.1%

- 9:45am: Chicago Purchasing Manager, est. 58.5, prior 58.4

- 10am: Pending home sales, est. 2.0% (prior -4.6%)

- 10am: NAPM Milwaukee, est. 56.0, prior 55.5

- 10:30am: DoE inventories

- 11:30am: Fed’s Plosser moderates panel in SF

- 2pm: Fed’s Beige Book

WHAT TO WATCH:

- S&P downgrade of banks “expected” and “manageable,” Goldman says. Watch bank stocks; Bank of America hit a low of $5.03 during regular trading yday

- FAA to increase safety inspections of American Airlines

- President Obama travels to Scranton, Pennsylvania, to spotlight plan for jobs, then to New York for re-election fundraisers

- Secretary of State Clinton in Myanmar

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – down this morning because the US Dollar is up; this is a new correlation risk that’s developing and was only this high last in Q4 of 2008; immediate-term inverse correlation to USD now = -0.79 (vs TREND of +0.08). Liquidations and redemptions in the hedge fund business are significant and so is the gross and net long position in Gold. Selling what they can vs. should.

- Gold Producers Poised Like ‘Coiled Spring’ to Rally: Commodities

- Former Goldman Traders Said to Start Hedge Fund With Mezvinsky

- Iran Oil Sanctions Set to Shrink Circle of Foreign Buyers

- Korean Shipbuilders’ Focus Is No Longer Ships: Chart of the Day

- Gasoline Makers Showing First Losses in 3 Years: Energy Markets

- Oil Pares Second Monthly Gain After U.S. Crude Stockpiles Rise

- Iron Ore Seen Finding Floor at $120 as China Rebuilds Stockpile

- Morgan Stanley Says Commodities Gains to Be Limited in 2012

- Gold Falls in London, Erasing Monthly Advance, as Dollar Gains

- Central Banks May Repeat Gold Purchases of 450 Tons, UBS Says

- Copper Extends Monthly Decline After S&P Cuts Banks’ Ratings

- China Lion Fund’s Asset in Gold ETFs Halved to $250 Million

- Commodities Are Set for ‘Difficult’ Year in 2012, UBS Says

- Palm Oil Has Longest Losing Streak in Five Years as Exports Drop

- Commodities May Jump 7.1% in Next Two Months: Technical Analysis

- Corn Declines on Rising Supplies From South America, Ukraine

- Copper Falls in London as S&P Downgrades U.S. Banks: LME Preview

- New Hope Holding Talks With ‘Several’ Potential Bidders

- Commodities Upside Limited in 2012 on Growth Outlook, Dollar

- Rubber Drops From One-Week High as S&P Downgrades Global Banks

CURRENCIES

EURO – just a pathetic week for European central planners and their currency’s credibility – rally to 1.34 is gone and now we’re testing intermediate-term lows of 1.32 again; bullish for the USD; bearish for Correlation Risk across Global Macro

EUROPEAN MARKET

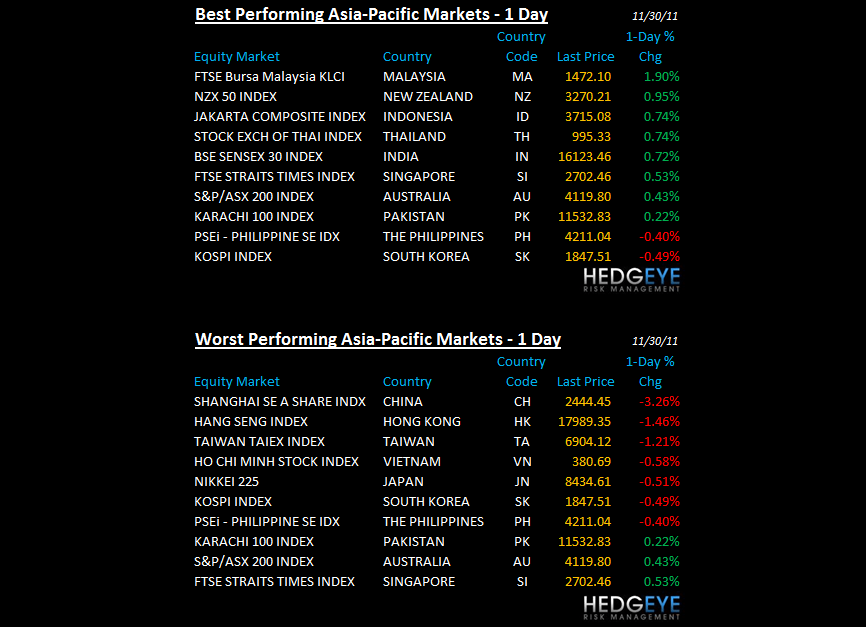

ASIAN MARKETS

CHINA – not in headline news for the last few weeks but that doesn’t mean China’s growth slowdown (and implications to global growth) cease to exist; Chinese stocks got hammered overnight, closing down -3.3% close to their OCT lows (down -16.9% YTD). Thailand cut rates aggressively (125bps to 2.5%); expect more Asian rate cute (bullish for USD).

MIDDLE EAST

- Citigroup Deal Haunts Pandit as Saudis Seek to Reclaim Fortune

- U.K. Warns of ‘Consequences’ After Tehran Embassy Attack

- VTB Capital Said to Hire 4 Bankers From Credit Suisse Dubai

- Iran Oil Sanctions Set to Shrink Circle of Foreign Buyers

- Dubai Sukuk in One of Worst Months Since 2009: Islamic Finance

- Qatar Returns to Global Debt Market With $5 Billion Fund-Raising

- Dubai Islamic Bank, Tamweel Hire Banks for Possible Bond Sale

- Emirates NBD May Sell Sukuk for Acquisition, Debt: Arab Credit

- Arabtec Expects Saudi Contract Value to Rise to $400 Million

- Abu Dhabi Shares Rise to Week-High as FGB Spurs MSCI Optimism

- Iran's missile base obliterated: satellite imagery

- Ex-Saudi Spy Chief Warns Against Iran Attack, Jordan Times Says

- Iran Blast Reports in Nuclear Province Fuels Sabotage Suspicion

- Standard Chartered Names Hassan Jarrar CEO of Bahrain Unit

- British Embassy Evacuates Staff From Iran, BBC Reports

- U.A.E. Starts Investing in U.S. Treasuries, Backs Dollar Peg

- U.K. Says Some Embassy Staff in Iran Are Leaving Tehran

- British Embassy Staff Leave Iran Following Ransacking of Diplomatic Offices

The Hedgeye Macro Team

Howard Penney

Managing Director