Uninspiring fundamental results the quarter after a significant shift in strategy (i.e. aggressive store closures) is enacted is to be largely expected, but the reality is that PSS’ stock remains a waiting game for investors. We still think the break-up value is ~20%+ higher, but with the company under strategic review we need to have better confidence in a sale either in part or whole, or that a new CEO will raise the bar to take our estimates meaningfully higher. Until then, break-up value math is a simple smokescreen.

But the biggest question that we increasingly think needs to be answered is whether or not the Core Payless business deserves to exist at all. To determine a real margin of safety here, we have to evaluate the NPV assuming that it does not.

But we all know that we can’t simply make pretend that the business goes away with a special charge or two. It would be a painful exercise of absorbing losses in the Payless in order to get to the optimal store count. The question is whether that store count is 3,500, 2,500, 1,000, 500, or zero. We don’t think it’s zero. There are some Payless stores running at a margin well above 20%. But it’s probably not a number starting with a 3 – and perhaps not even a 2.

We don’t have the answer to this yet, and there’s no doubt that anyone that would step in as a buyer for the company would need to have done the work, or if there have been offers for PLG, then PSS will need that level of comfort for the Payless business that remains.

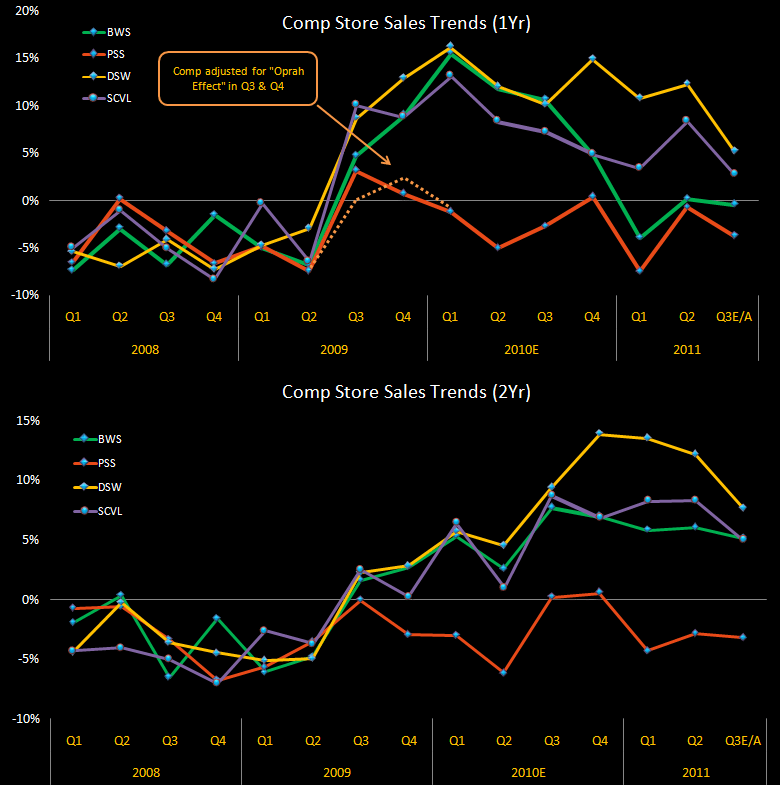

In looking at Q3 results, sales were mixed with domestic Payless coming in lighter than expected with comps down -4.5% along with a deceleration in International Payless offset in part by PLG wholesale coming in strong. A major point is that PLG accounted for 78% of aggregate operating profits in the quarter.

The biggest delta in the quarter is on the gross margin line coming in down -524bps reflecting the company’s new pricing strategy – offering more moderate price points. The issue here is that the strategy was implemented on legacy product purchased prior to the new strategy and intended to have a higher initial price (i.e. a great exercise in finger-pointing). We are reducing our gross margin estimates to down -325bps in Q4 as this disconnect will weigh on margins near-term and through Q1 in addition to reflecting like product cost increases of +10%.

While near-term fundamentals are mediocre at best, there is early (and we stress early) evidence to suggest the company’s new strategies are starting to show signs of progress. After a weak start in August, domestic Payless sales improved through the quarter from down high single-digits to flatish in response to the sharper pricing. While hardly a trend, it’s a trajectory worth noting. In addition, the company ramped the number of store closures by year-end to 350 from 315 of 475 over next 3-years as well as cut the associated costs (lease terminations, severance, etc.) to $25mm-$30mm reducing the high end of the range by $5mm. Taking the pain now is a positive and should accelerate the timing of a turn in profitability.

Assuming PSS continues to operate as it exists today (including store closures), we’re shaking out at $0.70 for F11 EPS and $1.14 for F12 EPS. This stock typically trades at 10-12x EPS and 5-7x EBITDA, which suggests a modest premium to where it is now. We get to a valuation of $12-$17 based on our bear case breakup analysis and can justify a valuation of the PLG business in the mid-teens to low 20s alone suggesting decent support at current levels, but we need better confidence in a sale either in part or whole, or that a new CEO will raise the bar to take our estimates meaningfully higher before we get more constructive on the name.

Below is the detailed analysis of the three potential outcomes noted above from our August 25thpost “PSS: The Decision Tree”

Our Take on Strategic Review Outcomes (from 8/25):

1) An all out sale of the company:

- This is the least likely of the three scenarios given the disparate characteristics of two business that would ultimately attract different buyers.

- The high fixed cost and real estate intensive nature of the domestic Payless business is best suited for a financial buyer. One with a Ron Johnson-like 7-year duration that can take control, absorb losses, and slowly but surely take the store count meaningfully.

- Another possibility is a large property owner like a strip-mall REIT that is better equipped to utilize the company’s store base and either take out/take down the leases, or flip them to a more profitable concept. But these companies are hardly cash-rich right now.

- Based on our breakup analysis, we get to a valuation of $3-$6 per share for the ‘core’ payless business (both domestic and international) taking debt into account and $9-$11 per share for the PLG business on our bear case assumptions. $3-6 + $9-11 = $12-$17. Using less than heroic assumptions, we can get a valuation for the PLG business in the mid-teens to low-20s alone.

2) A sale of some part of the company:

- This is a distinct possibility, but the company is less likely to sell off PLG in its entirety as the company’s key growth engine.

- Saucony and Sperry are the most likely candidates and both could see interest from both financial and strategic buyers.

- Re Saucony:

- VFC could buy it in a heartbeat. It’s small enough that they can do this side by side Timberland.

- Adidas makes sense. They’ll do anything to get into the technical running market. They’d rather buy Asics, but if the price is right it can happen.

- Why not Li&Fung? Li Ning? Yue Yuen? Li&Fung has stated flat out that it wants to buy brands to leverage its scale. Yue Yuen has diversified into retail. Moving into the content side of the equation would definitely leverage its manufacturing base.

- New Balance, Asics, and Under Armour are all out.

- Nike wouldn’t touch it with a twenty foot pole. The irony is that Nike does not do well at all in the technical running category – despite the fact that it views its birthright to be rooted in running (watch the movie ‘Without Limits’ or ‘Pre’). An interesting angle on Nike’s running share… it has about 35% share in the running space. But count the number of swooshes on the feet of the first 20 finishers of the Chicago marathon. You’ll see far fewer than 35%. Nonetheless, the factoid here is that as long as Nike THINKS it can dominate this category (which it does) it won’t buy anyone else. It’s a strategy that has paid off for shareholders, by the way.

- Re Sperry:

- A financial buyer is more likely. This brand is strong enough to be a stand-alone company – and even a public one.

- On the strategic side, there’s everyone from VFC, to JNY, to the same Asian acquirers that we think are going to make their way into this market.

- We’ve already hit on the valuations above, however in breaking out PLG further, Stride Rite and Keds are worth $1-$2 per share with Saucony and Sperry valued at $9-11 with slightly more than half of the value attributed to Saucony at $5-$6.

- There are no structural impediments that would prohibit a carve out of PLG from happening. However, carving out a single brand within PLG would be a bit more difficult in terms of integrated back office functions. Consider the following…

- It took the company a very very long time to integrate some of the back-end infrastructure (consolidated 2DCs and a manufacturing facility) and pulled roughly $25mm of SG&A out, but the PLG brands still operate independently to a large extent.

- The entire PLG team still operates out of their own HQs in Lexington, MA.

- It wasn’t until Q2 that only some of the PLG stores were hooked into the same PeopleSoft financial systems that the core domestic Payless business uses and in a similar fashion, the retail systems that count traffic/store metrics are also still largely independent from one another.

3) No sale at all. Instead, the company names a new CEO and gets to work on closing stores:

- Business as usual is probably the most likely outcome as the company completes its strategic review process.

- Assuming an asset sale does not occur, who PSS hires as the new CEO will be the most important near-term catalyst. (positive or negative)

- The board wasted no time in getting a plan in place to aggressively reduce underperforming stores, which is the most significant positive development to come out of Q2 results.

- In total, the company expects to close approximately 475 stores (~400 Payless & ~75 Stride Rite) over the next 3-years with 300 closings by year-end with most coming after the holidays.

- We are modeling approximately 60 store closures in Q3 and another 255 at the end of Q4.

- With roughly $110mm in revenues associated with these stores, we expect closures to impact revenues by $5mm in Q3 and ~$15mm in Q4. The greatest hit to revenues will come in F12 (~$75mm) given the timing of closures in F11.

- Additionally, there are $25-$35mm in costs (lease terminations, severance, etc.) associated with these closings, the bulk of which are expected to be realized in the 2H F11. Of course, the Street will strip these costs out as being non-recurring – even though they represent real cash going out the door, and PSS making up for poor decisions made in years past. Nonetheless, on an ‘adjusted’ basis, we’re likely to see far better comparision starting in 1Q12.

- Lastly, the net benefit of these actions are expected to improve EBIT by $18-$22mm once all closures are completed. We’re modeling in an incremental $0.15 in F12 EPS as a result of these actions.