Sports Apparel Sales continue to remain strong despite more difficult compares. We like FL and FINL into the quarter but these trends suggests a solid start to Q4 on the apparel side.

Additional Noteables:

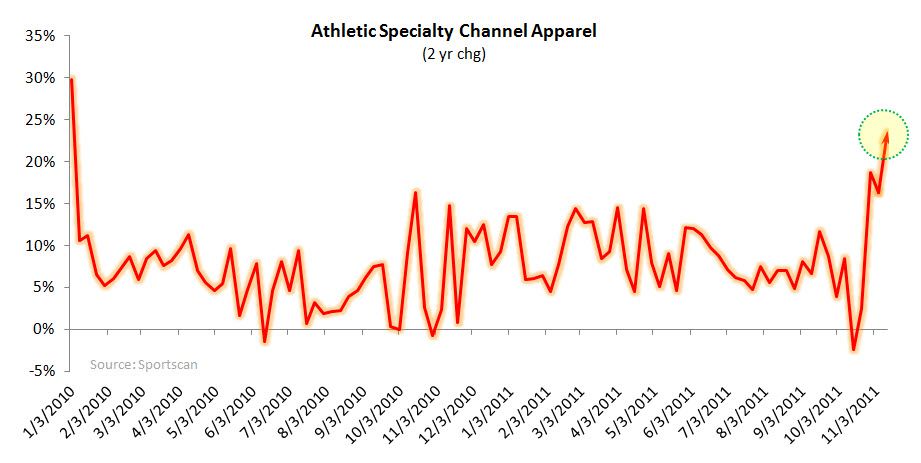

- Athletic Specialty Sales continue to outperform the other channels with strength in both pricing and units driving the 16% growth over 32% LY (this is the peak compare for the channel for the remainder of year)

- Outerwear continues to ramp earlier than in years past with growth north of 20% over the last 9 weeks; a potential pullback in unit sales looms but it is a better margin event on the whole. This is also positive for COLM & TNF – the latter of which is on a tear (see chart below)

- Basketball continues to grow LSD despite the increasing likelihood that the 2011-2012 NBA season is no more; Basketball looking more and more like a fashion play over performance

- Adidas continues to gain share but on a base of 8-10%

- Champion, which is about 15% of HBI’s total sales, has taken a rather dramatic turn down over the past two weeks. We initially viewed this an anomaly. Now we’re not so sure.