TODAY’S S&P 500 SET-UP - November 10, 2011

As we look at today’s set up for the S&P 500, the range is 31 points or -0.66% downside to 1221 and 1.86% upside to 1252.

SECTOR AND GLOBAL PERFORMANCE

If you were long King Dollar, Long-term Treasuries, and Growth Slowing yesterday, you enjoyed your day – always a bull market somewhere!

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2517 (+1459)

- VOLUME: NYSE 1112.51 (+26.47%)

- VIX: +36.16 +8.48 YTD PERFORMANCE: +103.72%

- SPX PUT/CALL RATIO: 2.18 from 1.98 (10.1%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 44.41

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.04 from 1.96

- YIELD CURVE: 1.81 from 1.73

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Import Price Index; M/m est. 0.0% (prior 0.3%)

- 8:30am: Trade balance; est. -$46.0b (prior -$45.6b)

- 8:30am: Jobless claims; est. 400k, prior 397k

- 9am: Fed’s Lockhart speaks in Washington

- 9:45am: Bloomberg consumer comfort; est. -51.0, prior -53.2

- 10:30am: EIA natural gas storage

- 10:40am: Fed’s Evans welcome remarks at Chicago banking conference

- Noon: Fed’s Bernanke speaks to soldiers in El Paso, Texas

- 1pm: ECB’s Praet Speaks in Chicago

- 1pm: U.S. to sell $16b in 30-yr bonds

- 2pm: Monthly budget statement, est. -102.5b, est. $140.4

WHAT TO WATCH:

- Svenska Cellulosa agrees to buy Georgia-Pacific’s European tissue ops for $1.8b.

- U.S. trade deficit probably little changed at $46b, economists est.

- Greek President Papoulias calls meeting with political party leaders for today:

- U.S. foreclosure filings rose 7% in October to a seven-month high

- Cisco rating boosted by Deutsche after 1Q EPS, rev. beat est.

- Deutsche Telekom 3Q Ebitda beat est.

- Credit Agricole profit trails est. after EU905m Greek writedown

- The European Commission slashed its euro-region growth forecast for next year by more than half

- WhaleShark, which distributes online discounts, said to gain funding that values it at as much as $1b

- PC shipments may fall as much as 3.4% in 4Q following floding in Thailand, IDC says

- Mitsubishi agreed to pay $5.39b for Anglo American’s Chilean copper unit

- U.S. Bancorp sued by an Oklahoma police pension fund over mortgage bonds allegations.

- Italy sells 1-yr bill as 6.087%, most since Sept. 1997

COMMODITY/GROWTH EXPECTATION

- Copper Drops to Two-Week Low as EU Cuts Euro Growth Forecast

- Gold Falls for Second Day in New York After Gain in Dollar Value

- Oil Rises Near Three-Month High on Europe Sentiment, U.S. Supply

- Solar Glut Worsens as Supply Surge Cuts Prices 93%: Commodities

- Most Refinery Cuts Since ’80s Can’t Help Profits: Energy Markets

- Noble Falls Most Since 1998, Bond Risk Doubles as CEO Quits

- IEA Cuts Oil Demand Forecast a Third Month on Weaker U.S., Japan

- Gold ETF Calls Surging Most Since U.S. Stripped of AAA: Options

- Palm Oil Jumps to 3-Month High as Stockpiles Decline in Malaysia

- Transocean Risks Junk Grade as Cash Flow Ebbs: Corporate Finance

- Soybeans, Grains Decline on Concern Euro Crisis May Slow Demand

- Gold Exchange-Traded Products Attracted $2 Billion in October

- Indonesian Tin Shipments Gain for First Time in Four Months

- Copper Declines to Two Week-Low on Europe

- Brent Oil to Drop After Failing at $116 Peak: Technical Analysis

- Asia Naphtha Crack Drops; Hin Leong Buys Fuel Oil: Oil Products

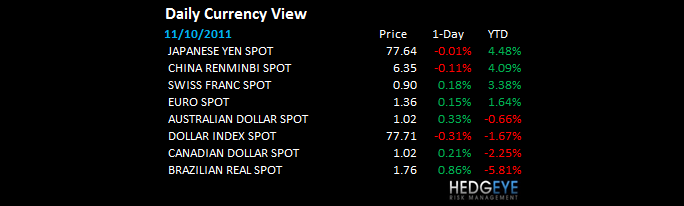

CURRENCIES

EURO – when our only line of remaining support (TRADE line support of $1.37) snapped yesterday, oh did they snap! Not only is this risk cleanly defined by The Correlation Risk, but a flailing currency perpetuates economic stagflation. European Stagflation is not consensus, yet – but it will be as long as Growth goes negative y/y and these inflation readings continue to accel sequentially.

EUROPEAN MARKETS

ASIAN MARKETS

ASIA – Growth Slowing continues to be the #1 factor that US centric investors (and European gawkers) have missed all year and will continue to miss if they don’t start modeling the day-to-day risk in both the Asian high-frequency economic data and what it’s embedding itself into Asian stocks/bonds/FX prices. Hang Seng down -5.3% last night and down -21.9% since April (crashing)

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director