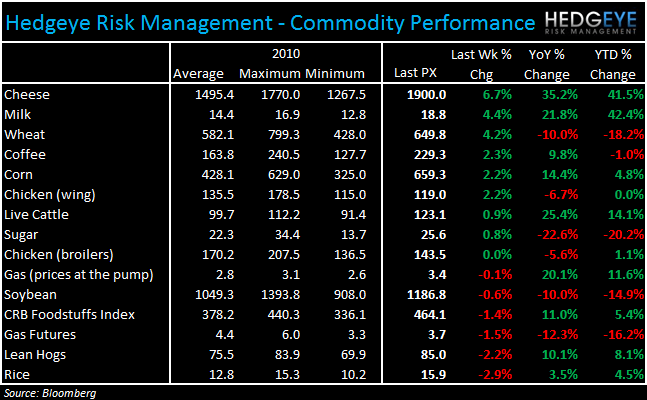

The important commodities, at least for the food and restaurant industries, moved higher over the last week. Despite the dollar strengthening over the past week, commodities went higher including those that typically trade with an inverse correlation to the greenback.

Please scroll down for charts detailing the trends of individual commodities.

STOCK THOUGHTS

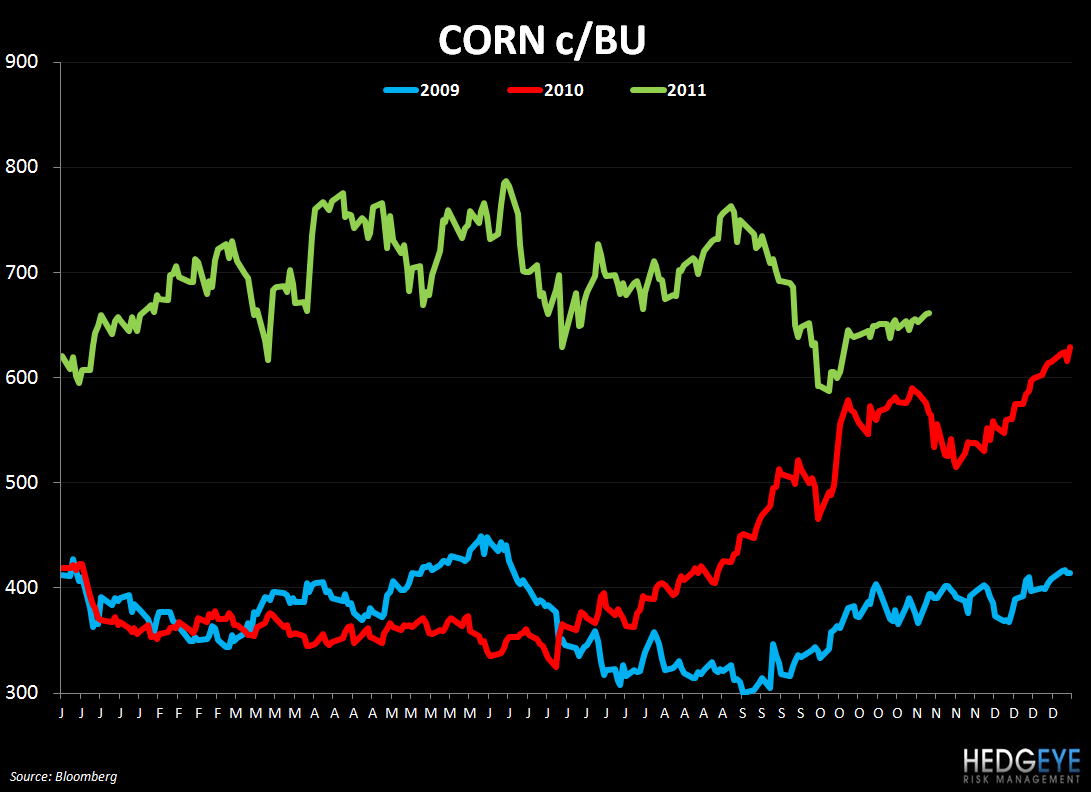

Corn - WEN, TXRH, CMG, SAFM

Corn is an important for all companies in the restaurant industry, not only those I mentioned in the heading. Corn prices gained again over the last week, even as the dollar gained, as the USDA crop progress report indicates that 87% of the harvest for the top 18 corn-producing states is complete. The USDA also cut its corn harvest estimate by roughly 1% from its previous forecast. The expected yields, per the USDA are now at 146.7 bushels per acre, down 1.4 bushels from the October forecast. If this yield were to come about, it would be the lowest yield since 2003.

Beef – WEN, TXRH, CMG

Texas is the state most associated with the drought that has plagued cattle farmers this year but ranchers in Arkansas are now stepping up the rate at which they are culling their herds. The quality of the calves being sold is also down, according to market participants interviewed by cattlenetwork.com. With grain too expensive to maintain herd sizes through the winter, and small rain showers having no material impact on soil conditions, farmers are downsizing their herds drastically.

While this is boosting supply in the near-term, for FY12 it may mean even higher prices. Consumer may expect higher retail prices in the grocery aisle but, as WFM noted in its earnings call last week, passing on inflation in meat prices has proven difficult.

Chicken –BWLD

Chicken wing prices have continued their march higher. As we wrote recently, food industry experts’ commentary as well as our own analysis gives us confidence that BWLD could have year-over-year inflation in wing prices beginning in the first quarter of 2012. Replicating the 3Q11 strategy of driving comps via a promotion will likely be difficult in 2012 if the company faces significant inflation. Some industry experts see $1.50 wings next year and sustained year-over-year inflation versus 2011 next year.

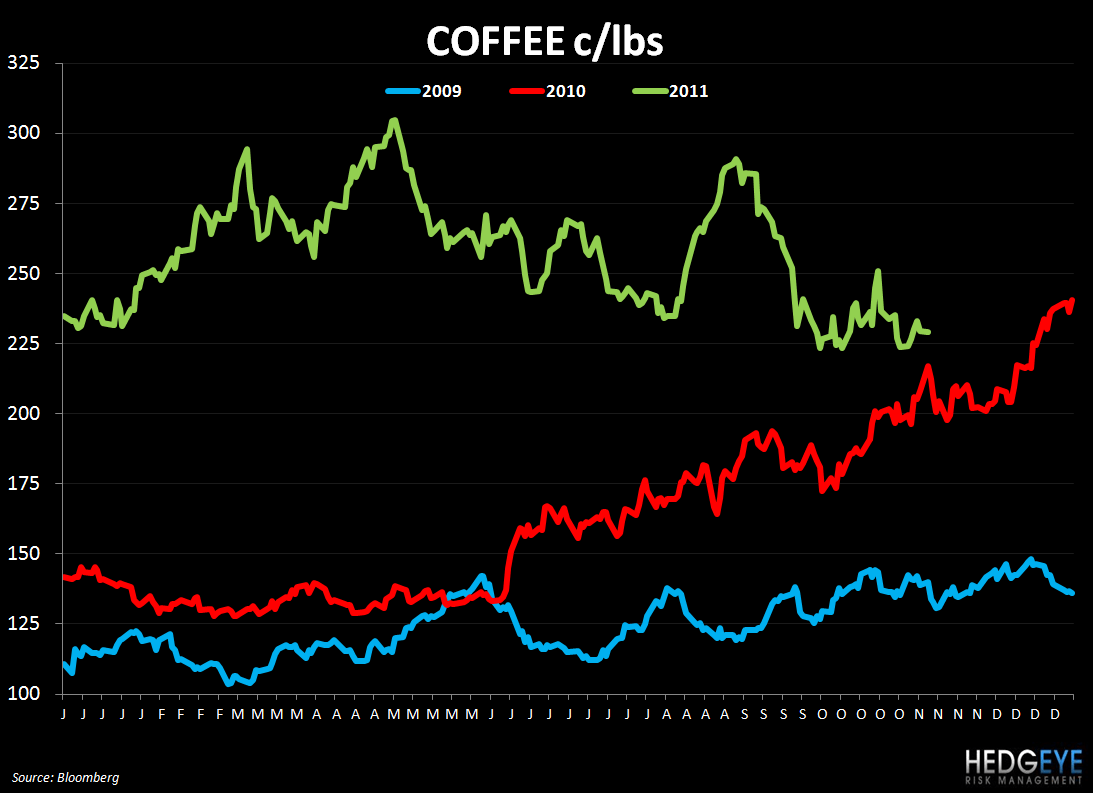

Coffee – SBUX, DNKN, PEET, CBOU, THI, MCD

Coffee prices moved higher over the last week after the previous seven days’ decline. Despite the crisis in Europe and the strengthening dollar, coffee prices gained 2.3% over the last week as coffee exports from Brazil fell to 3.1 million bags in October from 3.5 million a year prior. A University of Sao Paulo research group, Cepea, is stating that the 2012-13 harvest may still be a record, despite concern that dry weather and frosts earlier in the year could have hampered crop development.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst