THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

According to the National Bureau of Statistics, the annual inflation rate in China decelerated to 5.5% in October from 6.1% in September.

Hedgeye Financials posted this on today's MBA Mortgage Purchase Applications print - "The MBA Purchase Index rose 4.8% last week, bringing the series to an index level of 173. In spite of this improvement, purchase application levels remain roughly 5% below their rates from the summer. At the current rate, applications will finish the year roughly 10% lower than 2010. We reiterate that this has a direct read through to prices."

SUBSECTOR PERFORMANCE

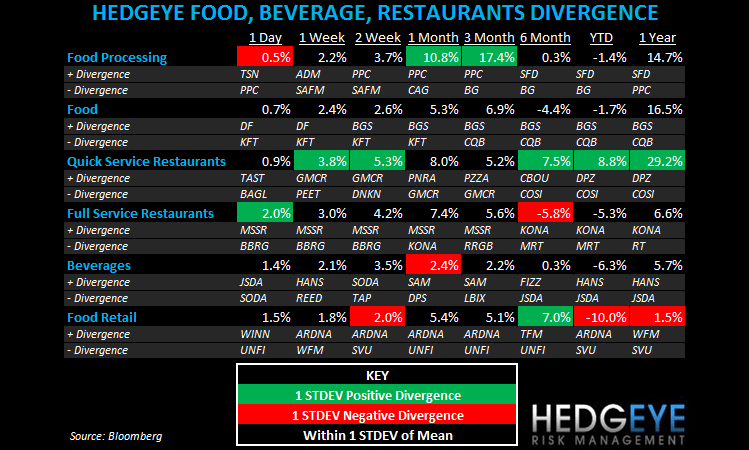

QUICK SERVICE

CBOU: Caribou Coffee reported 3Q EPS after the close yesterday of $0.07 versus expectations of $0.06. Comps increased 4.1% and FY11 and FY12 guidance of $0.39-$0.41 and $0.48-$0.51, respectively. Consensus is at the high end of both ranges.

CASUAL DINING

CAKE: Cheesecake Factory says it’s doing nearly anything it can to lower costs without cutting portions during a time of high commodity-price inflation. “We have to balance the need to protect margins with the even greater desire to grow guest counts”, said CFO Douglas Benn. WSJ

Howard Penney

Managing Director

Rory Green

Analyst