THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

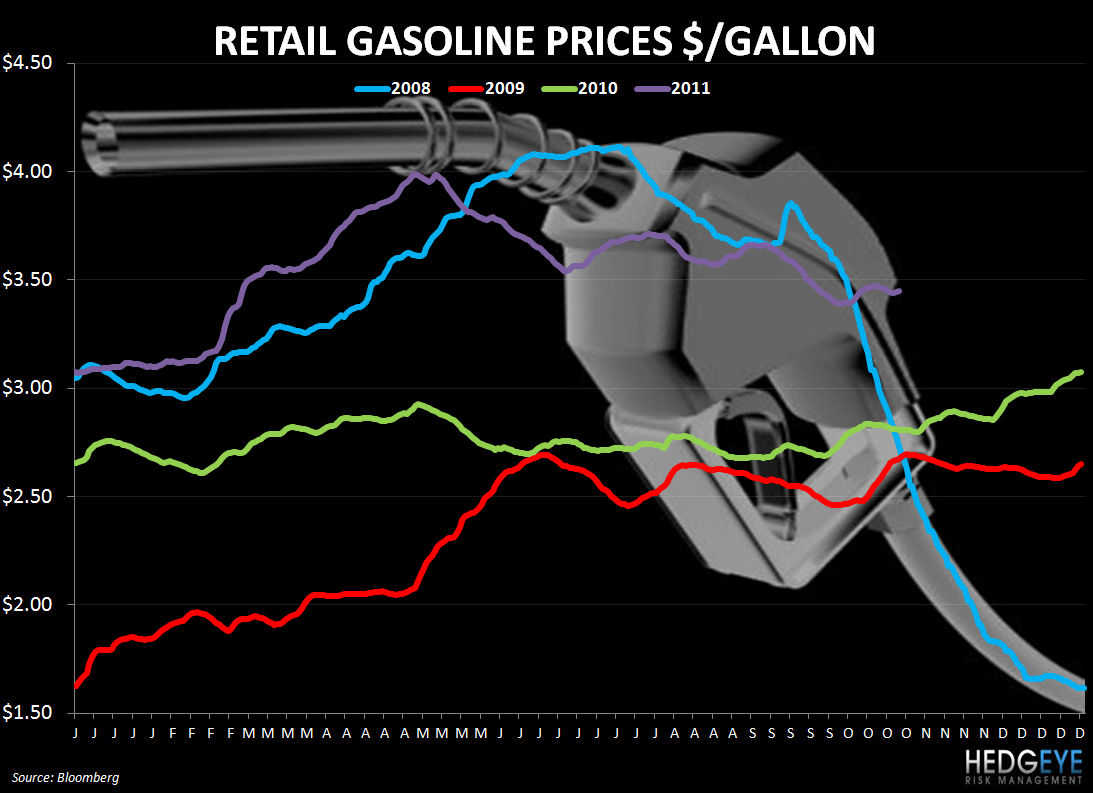

Gasoline prices are down 50 bps over the last week but seem to be trending flat-to-slightly-higher as the dollar has weakened. Gas prices coming down from the 2Q high’s has been a tailwind for restaurant traffic.

SUBSECTOR PERFORMANCE

GENERAL

The Nation’s Restaurant News Restaurant Social Media Index (RSMI) was released, ranking restaurant chains using three primary aspects of tracking in social media: digital brand interaction; consumer sentiment and social audience growth; and overall Klout score. Unsurprisingly, Starbucks topped the list. More surprising was Chili’s coming in at 75th. You can find the full list here.

QUICK SERVICE

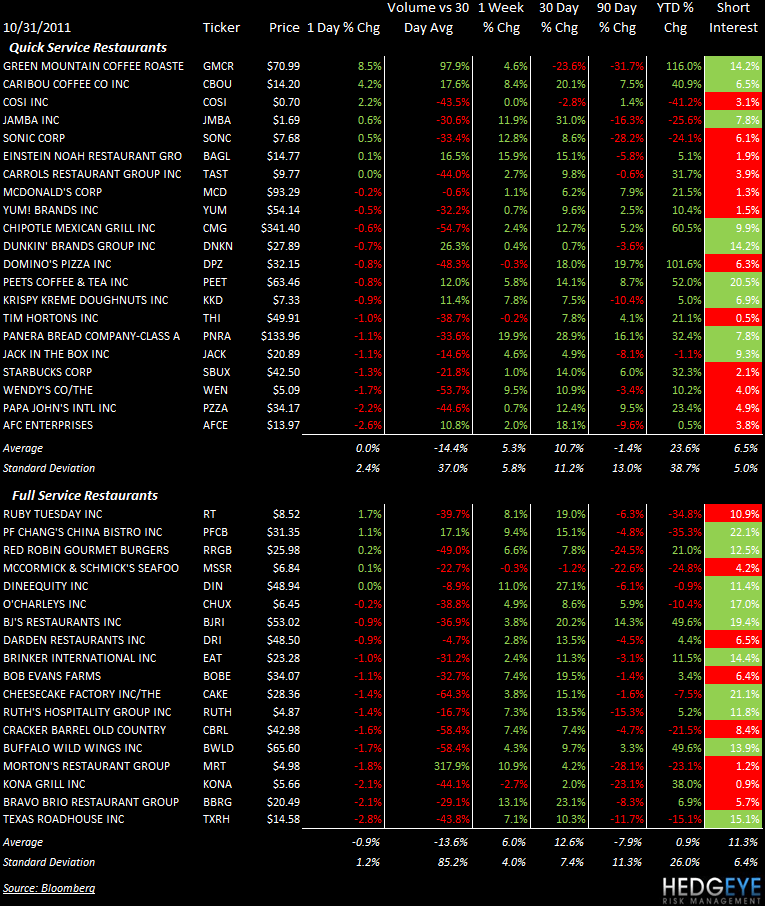

YUM: Yum! Brands’ KFC raised its menu prices in China by 0.5-to-2 Yuan, according to media reports. The move is the third price adjustment that KFC China has made in 2011.

JACK, JMBA: Jack in the Box and Jamba Juice are testing Google Wallet in a limited trial of the technology that lets customers pay for purchases and redeem coupons with their smartphones, executives at each chain have said, according to Nation’s Restaurant News.

SONC: Sonic is putting out a new Bacon Cheddar Melt burger and a Mushroom Swiss Melt burger. The advertisement reads "starting at $1.99" but it is unclear what exactly that means. The burgers are served on "Texas toast".

CASUAL DINING

MRT: Morton’s Restaurant Group was reiterated “Perform” at Oppenheimer.

Howard Penney

Managing Director

Rory Green

Analyst