THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - October 26, 2011

This is what Bernanke and Dudley call The Price Stability!!

As we look at today’s set up for the S&P 500, the range is 32 points or -0.57% downside to 1222 and 2.03% upside to 1254.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

SENTIMENT - This morning’s II Survey is a big blow to the bulls as Bullish Sentiment pops from 35.8% to 40% and Bears drop to 37.9%, making the Spread Bullish by +2pts vs the -12pts to the Bear side in early October.

- ADVANCE/DECLINE LINE: -1979 (-3970)

- VOLUME: NYSE 1008.45 (+8.75%)

- VIX: 32.22 +10.12% YTD PERFORMANCE: +81.52%

- SPX PUT/CALL RATIO: 1.94 from 2.24 (-13.38%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 41.71

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.14 from 2.25

- YIELD CURVE: 1.88 from 1.95

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, week Oct. 21

- 8:30am: Durable Goods Orders, Sept., est. -1.0%, prior - 0.1%;

- 10am: New Home Sales, Sept., est. up 1.7% to 300k, prior 295k

- 10:30am: DoE inventories

- 1pm: U.S. to sell $35b 5-year notes

- 2pm: Bank of England’s Adam Posen speaks in New York

- 5:15pm: Bank of Canada Gov. Carney speaks in NY

WHAT TO WATCH:

- European leaders meet in Brussels today to discuss Greece’s second bailout, the recapitalization of banks, strengthening the EU440b ($612b) rescue fund

- Nokia hosts conf. in London, unveils Lumia smart phones with Microsoft’s Windows OS

- President Obama speaks on American Jobs Act at University of Colorado - Denver, 12:45pm

- Democratic members of Congress hold news conference to call on supercommittee members to preserve Medicare, Medicaid and Social Security benefits, 1pm

- Bullish sentiment increases to 40.0% from 35.8% in the latest US Investor's Intelligence poll; bearish sentiment decreases to 37.9% from 41.0% and those expecting a market correction decreases to 22.1% from 23.2%

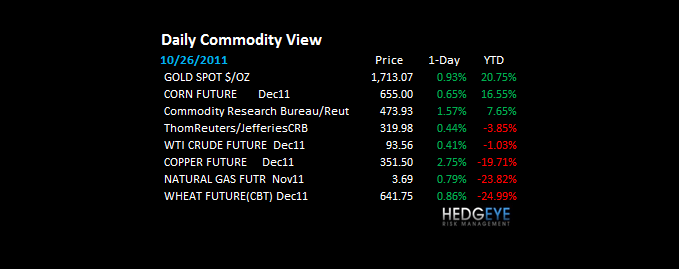

COMMODITY/GROWTH EXPECTATION

OIL – zoom; with the flick of a headline, Dudley’s role at the NY Fed is fulfilled, keeping the USD under pressure this week and Oil ripping US Consumption at exactly the wrong time (pre Halloween and Thanksgiving). The good news is that WTI is failing at its long-term TAIL of resistance ($93.89) this morning as the USD holds TREND and TAIL line support. Short Oil, buy the USD.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Thai PM Warns ‘50-50’ Chance Inner Bangkok May See Floods

- Oil Contango’s End Sparked by Falling Stockpiles: Energy Markets

- Gold Climbs to One-Month High as Europe Debt Woes Spur Demand

- Floods Ruining 14% of Thai Rice Erases Global Glut: Commodities

- Oil Trades Near 12-Week High as China Considers Economy Stimulus

- ArcelorMittal Quits $5.1 Billion Peabody Bid for MacArthur

- Agriculture Puts Surge After ETF Rises Most Since 2009: Options

- Russia to Sell $4 Billion Rail Fleet to Billionaires: Freight

- Copper Advances on Speculation China May Ease Monetary Policy

- Freeport Declares Force Majeure on Indonesian Mine Strike

- Jiangxi Copper Sees ‘Good’ China Demand on Building Projects

- Corn, Soybean Imports by China Seen Surging in ‘Golden Age’

- Copper Rises on Speculation of More Demand in China: LME Preview

- Iron Ore Price Slides 7.2%, Biggest One-Day Drop Since 2009

- Corn Gains as Imports Into China May Surge; Soybeans Advance

- Goldman Sachs, JPMorgan Raise Stakes in London Metal Exchange

- Cosan Gets No Respect as Barclays Sees Upgrade: Brazil Credit

- Argentines Ditch Steak as Beef Beats Inflation: Chart of the Day

CURRENCIES

EUROPEAN MARKETS

ITALY - Monster Pig Paper issuance by the Italians this morn, selling €8.5B 6-mth fiat with yield 3.53% vs 3.07% - ECB running out of bullets? The ECB has been supporting the Italian sovereign bond bid and its not working anymore – with yields rising like this, does the market have it wrong? We don’t think so. Italy has their guy running the ECB by next week – I’m sure the German people are just going to love that…

<CHART6>

ASIAN MARKETS

China’s 3Q job creation (+3.4 million QoQ; +6.8% YoY YTD; and 4.1% unemployment rate – flat sequentially) was rock solid and is supportive of our belief that the gov’t is actively supporting a rebalancing of the economy towards consumption growth. We don’t think it is sustainable if the EU and US slow incrementally from here, but it does quiet hard landing speculation for now.

Hong Kong exports (-3% YoY) are a very negative leading indicator for global demand. Went slightly negative in back in June ’08 and then decidedly so in Nov ’08.

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director