“Patterns replicate through time and manifest on each level because it is a grand unified manner in which all things move.”

-Martin Armstrong

While I am certain that there are plenty Market Practitioners who have adapted to their ecosystem in the last 5 years, uncertainty in Global Macro markets continues to reign supreme.

This is actually a good thing – whoever thinks that they can be certain about a central planner’s ability to suspend economic gravity is probably feeling more uncertain about that by the day.

Chaos Theorists Embrace Uncertainty. It’s what drives our process. No matter what you think about Nassim Taleb, Martin Armstrong, and Ray Dalio, I’m fairly certain that they don’t particularly care. These gentleman have capitalized on proactively preparing for tail risks by simply not allowing themselves to be certain of anything until both Time and Patterns make whatever that is obvious.

Yesterday, it became fairly obvious that 56 exotic animals running down a man’s driveway in Zainesville, Ohio was a risk. There were 18 tigers, 17 lions, and 8 bears. The owner of the fancy pets had shot himself after his wife left him.

In response, a politician in Ohio stated, “this was an accident waiting to happen.”

Ya think?

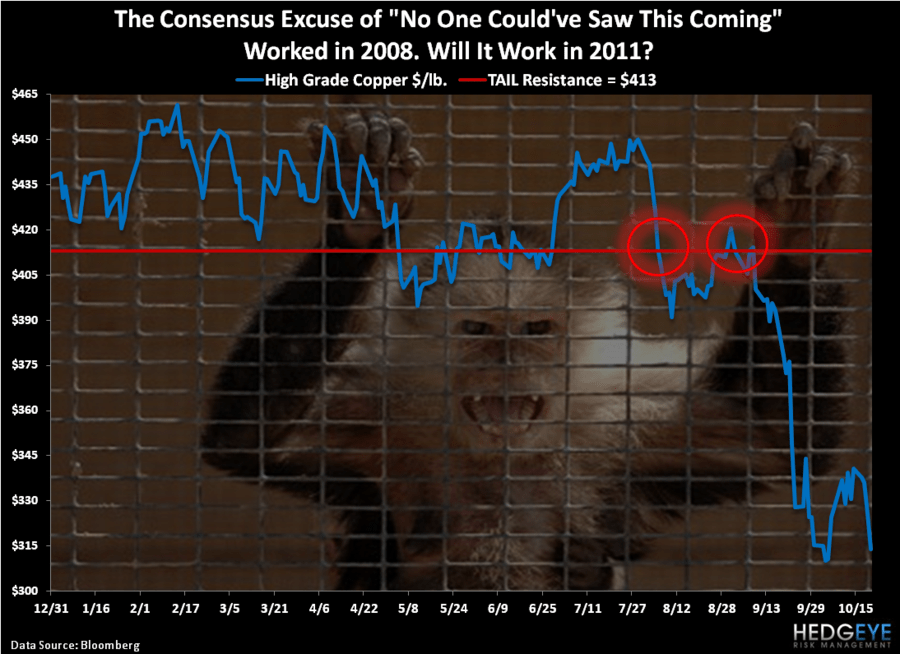

Exotic Tails of “risk” in Global Macro markets? What we see on the screens today, they are not. Like this whacko with his “pets”, the risks are plainly obvious to anyone who isn’t paid to be willfully blind. They have been since mid-July and early August (see Chart of The Day – when Copper’s TAIL broke).

Up until that intermediate-term 2011 point, these TAIL risks had been becoming more obvious for years. Since October 2007, the SP500 has lost 22% of its value and would need to rally +28.2% “off the lows” to get back to the Perma Bull Breakeven.

Time and Patterns

They take time to manifest and you need to do a tremendous amount of cycle research, across risk management durations, in order to appreciate that at any given time things can blow up.

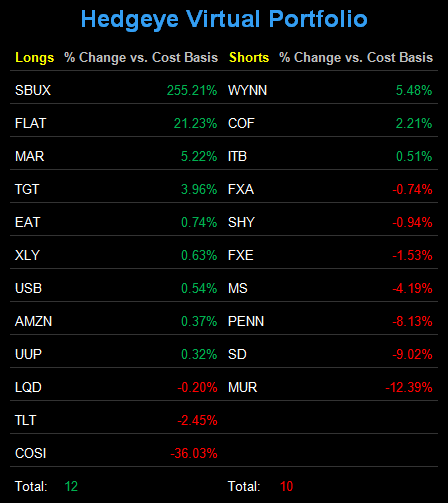

The US stock market is in the process of either bottoming or blowing up. I could go either way with this really (that’s why I’m hedged; 12 LONGS and 10 SHORTS in the Hedgeye Portfolio). There are no rules against changing your mind. There’s just time and space.

From a timing perspective, the situation in Europe could blow up any day. If it does, no one should be surprised. The monkeys you see swinging from their journalistic rumor trees throughout the trading day are compounding systemic risk for the sake of their short-term careers – and if it suddenly goes bad out there, as Jack Hanna said yesterday in Ohio, “you can’t tranquilize attack monkeys in the dark.”

Short-term vs Long-term

A Keynesian’s answer to accepting responsibility for policy recommendation is that “in the long-run, we are all dead.” Well, unfortunately, for those of us who have successfully managed 5 down US stock markets in the last 12 years (2000, 2001, 2002, 2008, 2011), and seen net US jobs added over the span of this past decade = ZERO, in the short-run, people die too.

What would have happened if these Bengal tigers found a way to survive the night and hit the Streets of Ohio? Ask the monkey who didn’t make it past the end of the driveway…

This is the point. We have all of this Global Macro risk all compartmentalized in cages now. Or at least we think we do. No one can get out. So no one gets hurt.

No one loses their political life. Everyone gets fed their “fair share.”

Until someone opens the cages…

And, then… since no one saw any of this coming – we’ll be on the precipice of another Great Depression again unless we all huddle back into captivity, take our commoner’s wage, and like it.

Yesterday I raised our US Equity position in the Hedgeye Asset Allocation Model to 6% from 3% (we’ve upped our beta by going long Consumer Discretionary, XLY, and selling Utilities, XLU).

I’m bullish on the US Dollar and, in the end, I believe that Americans are smart enough to realize that a Strong Dollar = Strong America.

In the long-term, Time and Patterns agree with me on this. Martin Armstrong says that it’s “the reason life perpetuates through what is called a system of self-referral.” George Soros calls it “reflexivity.” We call it Mr Macro Market.

No matter what you want to call it, it is all based on the most relevant mathematical discovery since relativity. So don’t let the Keynesians call what you see out there today, tomorrow, or the next day, an Exotic Tail.

My immediate-term support and resistance ranges for Gold (bearish TRADE and TREND), Oil (bullish TRADE; bearish TREND), German DAX (bullish TRADE; bearish TREND), and the SP500 (bullish TRADE; bearish TREND) are now $1, $80.09-89.11, 5, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer