THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Small-business confidence

Yesterday, recession fears continue to weigh on U.S. small-business confidence, as the NFIB Index moved slightly higher in September, rising from 88.1 to 88.9.

The gain snaps a streak of six consecutive monthly declines. Despite the improvement, the index remains depressed, having been below 90 for three consecutive months. There was no noticeable improvement in the details; it is clear small businesses are in no rush to expand.

Commodities

Corn and wheat prices have driven higher over the past week. News emerging today from the government states that the U.S. corn crop, the world’s largest, will be 0.5% smaller than forecast last month after unusually hot weather in July and freezing temperatures in September reduced yields.

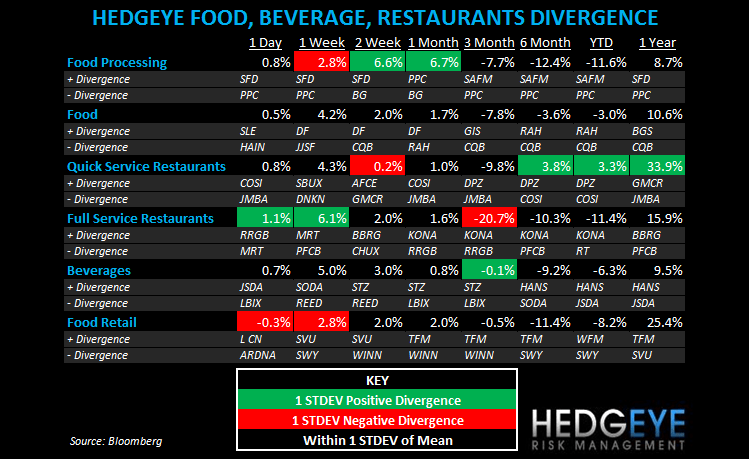

SUBSECTOR PERFORMANCE

Food processor stocks have slowed as corn prices reversed the downward slide that had been helping the outlook of TSN, SAFM, and the rest of the industry.

QUICK SERVICE

CMG: An article in Fortune, published yesterday, is highly critical of Chipotle’s new concept, ShopHouse Southeast Asian Kitchen.

CASUAL DINING

EAT: GS resumed coverage of Brinker at Neutral with a price target of $21.

EAT: Chili’s Grill and Bar opened its first restaurant in Sao Paulo, Brazil.

DRI: Coverage of Darden was resumed at Goldman Sachs at Buy

CAKE: Coverage of The Cheesecake Factory was resumed at Goldman Sachs at Sell

PFCB: PFCB was resumed Neutral at GS, price target is $29.

Howard Penney

Managing Director

Rory Green

Analyst