THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - October 12, 2011

After markets crash and funds have to liquidate, they have to cover their short positions – subtle but real factor and this short covering bid from Hong Kong to the S&P Futures remains relevant until it doesn’t; a 9-12% rally from bombed out lows is not atypical in a high volatility environment.

Longer term, every TREND line in the Hedgeye macro model is broken.

Earnings is always a hot topic in the bottoms up crowd and my overall point on earnings season is that it’s the riskiest we have “comped” in the last 6 quarters. Everyone and their brother knows “earnings have been good”, but earnings are cyclical, down Dollar has been a tailwind, and the Global Growth cycle has turned.

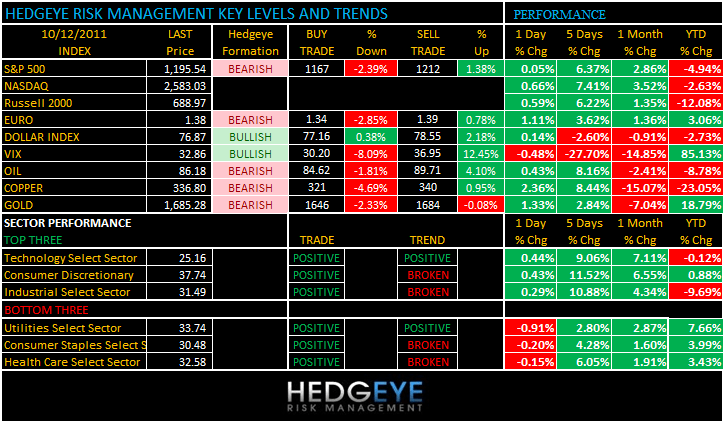

As we look at today’s set up for the S&P 500, the range is 45 points or -2.39% downside to 1167 and 1.38% upside to 1212.

SECTOR AND GLOBAL PERFORMANCE

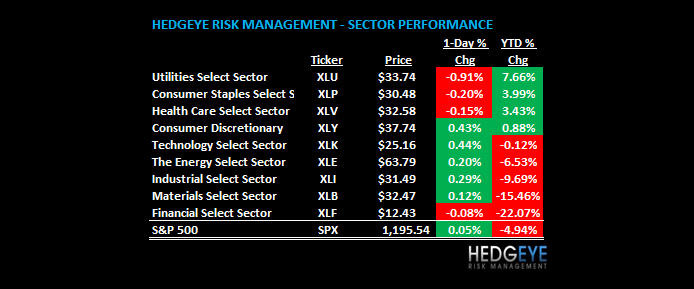

As of last night 6 of 9 sectors are positive on TRADE. The Question now is can these newly captured TRADE lines of support hold? Earnings and Europe will decide the answer. There has not been a more important earnings season in 2 years and I think the cyclicals remain the liability.

Since the Yield Spread is cyclical, so are net interest margins at the Financials. That’s one of 3 Sectors (Financials, Energy, and Basic Materials) that have not recovered either TRADE or TREND lines of support. Tech has – that’s new. That makes Tech and Utilities the only 2 Sectors that are bullish TRADE + TREND.

Alcoa isn’t exactly a high quality of earnings company. But if the TREND is what the market is already forecasting (7 of 9 Sectors are bearish TREND), Alcoa’s guidance for everything to magically recover sequentially in Q4 (versus Q3 pricing pressure) will likely be met with contempt rather than complacency.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 343 (-2187)

- VOLUME: NYSE 882.22 (-0.66%)

- VIX: 33.86 -0.48% YTD PERFORMANCE: +85.13%

- SPX PUT/CALL RATIO: 1.90 from 1.96 (-2.78%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 39.75

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.18 from 2.10

- YIELD CURVE: 1.86 from 1.80

MACRO DATA POINTS (Bloomberg Estimates):

- 7 a.m.: MBA Mortgage Applications, prior (-4.3%)

- 10 a.m.: JOLTs job openings

- 11:30 a.m.: U.S. to sell $30b 4-wk bills

- Noon: DoE short-term outlook

- 1 p.m.: U.S. to sell $21b in 10-yr notes reopening

- 1:15 p.m.: Fed’s Pianalto speaks at Univ. of Akron

- 1:20 p.m.: Fed’s Fisher speaks at Abilene, Texas

- 1:30 p.m.: Fed’s Plosser speaks on economy in Phila.

- 2 p.m.: FOMC Minutes

- 4:30 p.m. API inventories

WHAT TO WATCH:

- China said the U.S. currency bill passed by the Senate alleging the yuan undervalued violates world trade rules

- Slovakia, the only country that hasn’t ratified a revised European bailout fund, headed for a second vote after failing to approve the package yesterday

- Wal-mart hosts investment community meeting; watch for comments by CEO Duke in am, CFO Holley on possible capex spending

- Johnson Controls hosts strategy meeting; watch for 2012 EPS, rev.

- Euro banks may face more stringent pay and bonus rules than rivals in North America, the Financial Stability Board said

- Wal-Mart Halts Operations at More China Stores Over Labeling

- ArcelorMittal Unit in Ore-Carrier Talks to Shatter Arctic Ice

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Alcoa Profit Misses Estimates as Europe Cuts Aluminum Orders

- Gold Eclipses Cocaine as Rebels Tap Mining Wealth in Colombia

- Saudis Lay 2,400 Miles of Rail to Ease Oil Dependence: Freight

- Record Coal Price Risk Gaining on Australian Rain: Commodities

- Oil Drops First Day in Six on U.S., Europe Fuel Demand Outlook

- Gold Gains in London as European Debt Concerns Spur Demand

- Copper Gains as Shrinking Asian Stockpiles Signal Steady Demand

- IEA Cuts Oil Demand Forecast a Second Month on Slowing Economy

- Industry Gas Use Shows Slowest Growth Since 2009: Energy Markets

- Corn Extends Biggest Gain Since June 2010 on Stockpiles Demand

- Ship Lines Delay Asia-U.S. Rates Plan on Unpredictable Cargo

- Treasuries Decline, S&P 500 Advances as Commodity Producers Rise

- EU Farm Policy Debate Pits Top Recipient France Against U.K.

- Oil Rises Near Three-Week High as Europe Prepares Bank Support

- CFTC Said to Have Enough Votes to Approve Speculation Limits

- IEA Says Commodities No Longer a Separate Asset Class Since 2008

- Palm Oil Advances a Third Day After Soybeans Rally on Exports

CURRENCIES

FROM KM - EURO – I wasn’t short it at the bottom; but I did say short it w/ impunity at 1.36 (TRADE line resistance) and I’ll keep saying the same up to the TAIL and TREND lines of resistance (1.39 and 1.43); this is one of the world’s biggest short positions (Paulson getting squeezed there now too), so don’t stress about it; just understand it and manage risk around it.

EUROPEAN MARKETS

Slovakia's lawmakers have voted down an expansion of the euro zone's bailout fund ; the government of Prime Minister Iveta Radicova lost a confidence vote. However, a repeat vote on the EFSF could be held later this week and passed, if the government receives the support of opposition lawmakers from the left-of-center Smer-Social Democracy, or Smer, party. This would likely require a cabinet reshuffling. The repeat vote on the EFSF is unlikely to take place Wednesday as more time for political talks will be needed.

ASIAN MARKETS

Yesterday, Indonesia joined Turkey and Brazil as Emerging Markets that followed through with “surprise” rate cuts. (We use quotations because Hedgeye Macro clients have been warned of this since April.) Expect more Deflating the Inflation to continue getting priced into the interest rate and FX markets of EM economies. Indonesia, Philippines, and Malaysia are all preparing or implementing fiscal stimulus to bolster domestic demand.

MIDDLE EAST

Howard Penney

Managing Director