TODAY’S S&P 500 SET-UP - October 11, 2011

Levels matter and ASIA looks more bearish in the majors (HK, Nikkei, KOSPI, etc) than Germany, France, and Italy do right now – that’s telling you something about Global Growth that is ringing in the -1.1% and -2.7% selloffs in oil/copper this morning that should be respected. Every stock market in Asia and every major commodity has failed at TRADE resistance.

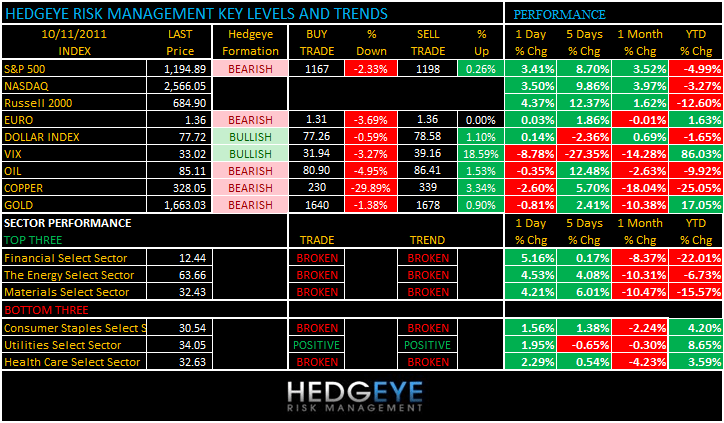

As we look at today’s set up for the S&P 500, the range is 31 points or -2.23% downside to 1167 and 0.26% upside to 1198.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 2530 (-1218)

- VOLUME: NYSE 888.12 (-22%)

- VIX: 33.02 -8.8% YTD PERFORMANCE: +86.03%

- SPX PUT/CALL RATIO: 2.24 from 2.54 (-11.80%)

CREDIT/ECONOMIC MARKET LOOK:

From KM - US TREASURIES: very interesting action on the short end of the curve continues to develop w/ 2-year yields having broken out above my TRADE line of 0.21% and now testing my TREND line up at 0.30%. I expect short-term yields to back off here, but the short end of the curve should continue to pressure the Gold price (which failed again at $1678 TREND resistance)

- TED SPREAD: 38.91

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.16 from 2.08

- YIELD CURVE: 1.85 from 1.79

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30 a.m.: NFIB Small Business, est. 88.8, prior 88.1

- 10:00 a.m: IBD/TIPP Economic Optimism, est. 39.4, prior 39.9

- 11:30 a.m: U.S. to sell $29b 3-mo., $27b 6-mo. bills

- 1:00 p.m.: U.S. to sell $32b 3-yr notes

- 2:30 p.m.: Treasury Secretary Timothy Geithner participates in Financial Stability Oversight Council meeting

WHAT TO WATCH:

- FDIC to release Volcker Rule on proprietary trading

- Chrysler talks with UAW continue

- NBA cancels first two weeks of season

- Hewlett-Packard said to decide future of WebOS, Palm this week, AppleInsider

- FDA staff issues recommendation on Cook’s medicated heart stent ahead of 10/13 meeting; watch Medtronic, Baxter

- Citigroup said to halt soliciting some Japanese retail business as it awaits government investigation outcome

- Bloomberg/Washington Post Republican Presidential Debate at Dartmouth College, Hanover, N.H., 8 p.m.

- No IPOs expeted to price today

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Soy Slump Ending as Record Demand Overwhelms Farms: Commodities

- Oil Drops From Two-Week High in New York Before Europe Debt Vote

- Copper Declines Most in a Week on Concern About Chinese Demand

- Timah to Resume Refined-Tin Exports After Price Rebounds

- Corn Falls as U.S. May Raise Supply Estimate; Wheat Advances

- Gold Declines in London as Commodities Fall Before Slovakia Vote

- Sugar Declines in New York as Slower Growth May Curb Demand

- Rio Says Greece Risk Overdone as China Overcomes ‘Wall of Worry’

- U.S. Refinery Runs at Four-Month Low in Survey: Energy Markets

- Soy Sinks More Than Oil Deepens Bond Sell-Off: Argentina Credit

- Economists Call for Crop-Trading Limits to Curb Volatility

- Most Tankers Idled Since ‘80s Won’t Buoy Charter Rates: Freight

- Alcoa’s Earnings Recovery Slows on Aluminum Price ‘Headwind’

- COMMODITIES DAYBOOK: Gold Declines, Oil Falls From 2-Week High

- Ship Futures Jump to Year’s High as China Surge Lifts Charters

- Aluminum Demand to Grow as Much as 10% in 5 Years, Novelis Says

CURRENCIES

EURO – yesterday KM put up the $1.36 line in the sand and said short the Euro with “impunity” there.

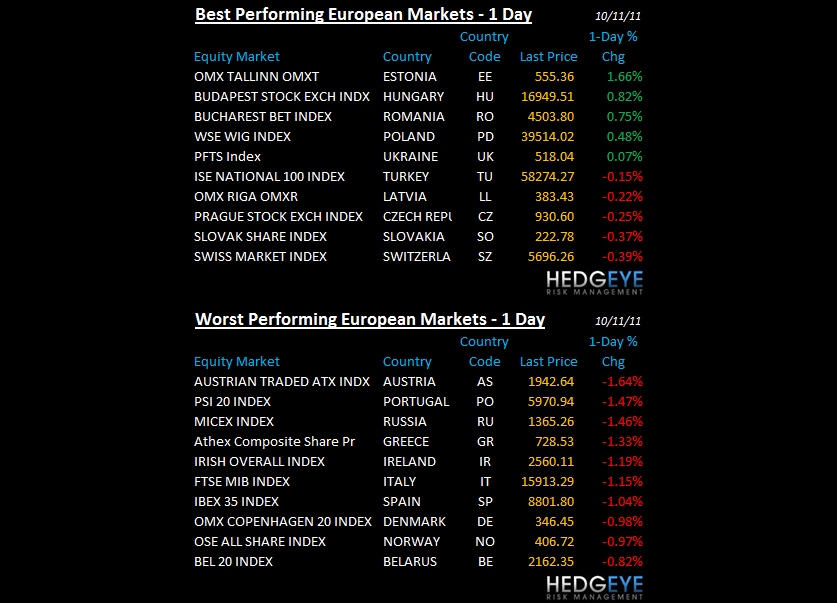

EUROPEAN MARKETS

ASIAN MARKETS

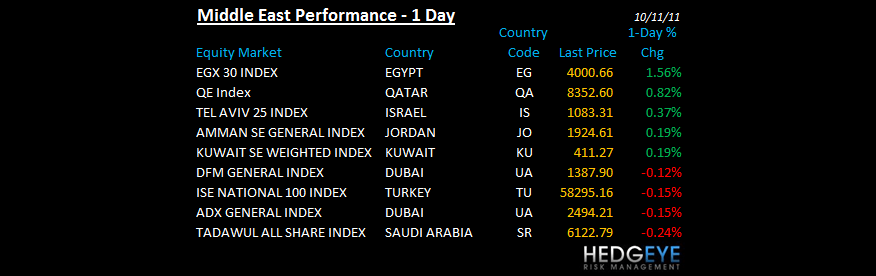

MIDDLE EAST

Howard Penney

Managing Director