“I love playing ego and insecurity combined.”

-Jim Carrey

There is a good article in this week’s The Economist titled “Return to Maastricht” where Charlamagne interviews locals in the Dutch town that gave birth to the Euro in 1991. Frans Timmermans has a concise quote on page 68 that summarizes the Eurozone today:

“Europe seems to be an agent of insecurity. The benefits are invisible; the downside is very visible indeed.”

The French know this. The Belgians know this. The Germans and the Dutch know it too – but the question remains as to whether or not they need to swallow Bear Stearns like exposures whole to the extent that the French and Belgians do.

On that score, this morning’s #1 Most Read Story on Bloomberg tells you all you need to know about what matters to interconnected Global Macro markets today:

“Merkel, Sarkozy Pledge Bank Recapitalization”

And while there are very different definitions of the size and scope of this “recapitalization” (coined first at Hedgeye as the Eurocrat Bazooka), this morning’s Global Macro market action tells you all you need to know about dominos.

Dexia, as we wrote last week, is the domino.

Dexia is a Belgian/French bank that is being bailed out this morning by, drum-roll, Belgium and France. Sure, the fine lads in Luxembourg appear to be throwing in some Europig Paper too – but, ultimately, this is a Belgian and French thing. A really big thing for those 2 countries in particular (relative to Germany and the Netherlands), because Belgium and France have marked their Pig Paper at par!

Qu’est ce qui se passe avec le marking of le Pig Paper at par?

Put simply, this is what Bear, Lehman, Morgan, etc. did in 2007-2008. They called it “level 3 asset pricing.” And Bailout Bankers around the world can call it whatever they want in Europe this morning, but there is one thing it is not – marked-to-market!

The most important move in all of Global Macro for the past 3 weeks has been that the US Dollar Index has been up for 3 consecutive weeks. In the end, I think this is the most bullish development there has been for the US economy. Strong Dollar = Strong America.

With the US Dollar Index up +7.8% since La Bernank tested Burning The Buck to a 30-year low in April of 2011, this has been good for the 71% of America that matters – Consumption (C) as a % of US GDP – and bad for dysfunctional debtors who are begging for bailouts.

This isn’t a consensus view. But I’m not really a consensus kind of a guy. And neither should you be. If the last 3 years has taught you anything about common sense, one is that Keynesianism is not for the commoner. If you are a debt laden aristocrat, sorry – can’t help.

Of course the US Dollar strengthening has nothing to do with Ben Bernanke or Tim Geithner changing their Keynesian policies (yes, It’s The Policy, Stupid). It has everything to do with the Europeans trying to do exactly what our Too Big To Perform financial system had Americans do in 2008 – bailout bad banks with tax payer backed fiat currency.

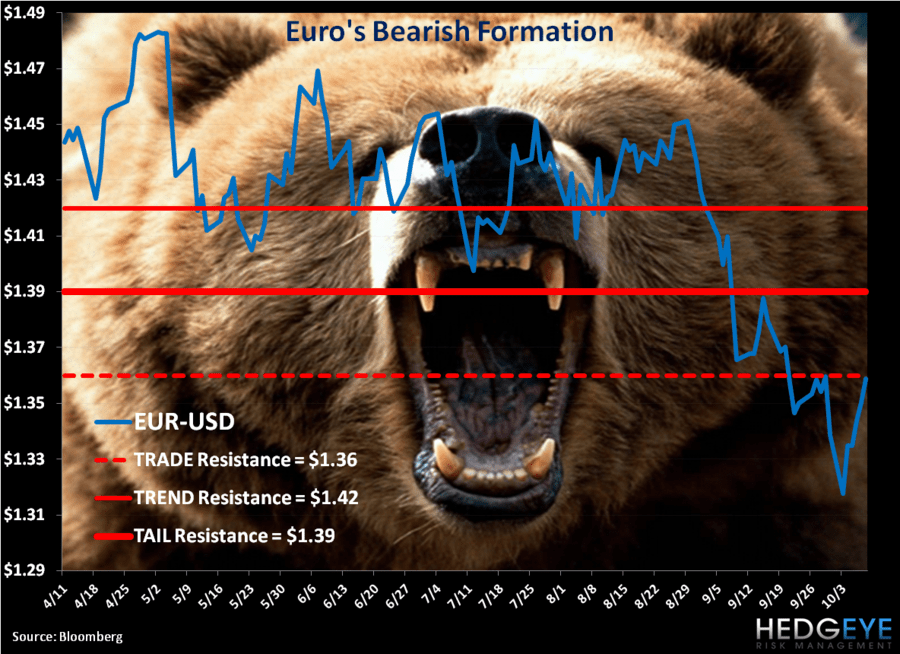

Perversely, with the “news” of the Dexia Domino in motion this morning, the Euro is rallying to another lower short-term and lower long-term high. This has more to do with the mechanics of the EUR/USD pair being the most widely held short position on planet hedge fund right now, so don’t let it stress you out.

Across all 3 of our risk management durations (TRADE, TREND, and TAIL), the Euro (versus the USD) remains bearish/broken:

- TRADE resistance = $1.36

- TREND resistance = $1.42

- TAIL resistance = $1.39

When all 3 of our risk management durations are bearish/broken, we call this a Bearish Formation. Those are not good.

And neither is Austria or Greece seeing their stock markets get hammered for -4.5% moves to the downside this morning. I guess that’s what you get when your Eurocrat Bazooka isn’t big enough, yet. Size matters. Insolvent European banks are seeing their marked-to-market stock prices fail. Insecurity’s Ego is going to have to have another European emergency bailout meeting about that…

My immediate-term support and resistance ranges for Gold, Oil, the German DAX, and the SP500 are now $1, $80.66-84.66, 5, and 1145-1169, respectively. My Cash position in the Hedgeye Asset Allocation Model dropped to 64% from 73% week-over-week.

Happy Canadian Thanksgiving and best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer