The jobs data released this morning are positive, on the margin, for the restaurant space.

On the surface, the employment data were positive for the restaurant space and it is important to take these data points for what they are. Nonfarm payrolls came in way ahead of expectations at 103k versus expectations of 60k and an upwardly revised 57k in August. However, there are some important caveats within the employment report that we think are worth noting for restaurant stocks.

- The number of people in part-time work for economic reasons ticked up to 9.3 million in September

- Long-term unemployment ticked up to 6.2 million in September.

- The unemployment rate is being aided by the fact that the labor force participation rate has not increased meaningfully since the “recovery” began.

- Manufacturing jobs contracted in August, disappointingly, while construction jobs ticked up from August to September. Government jobs continued to decline, with local governments shedding jobs heavily, implying that the growth came from the private sector. We view this as a positive.

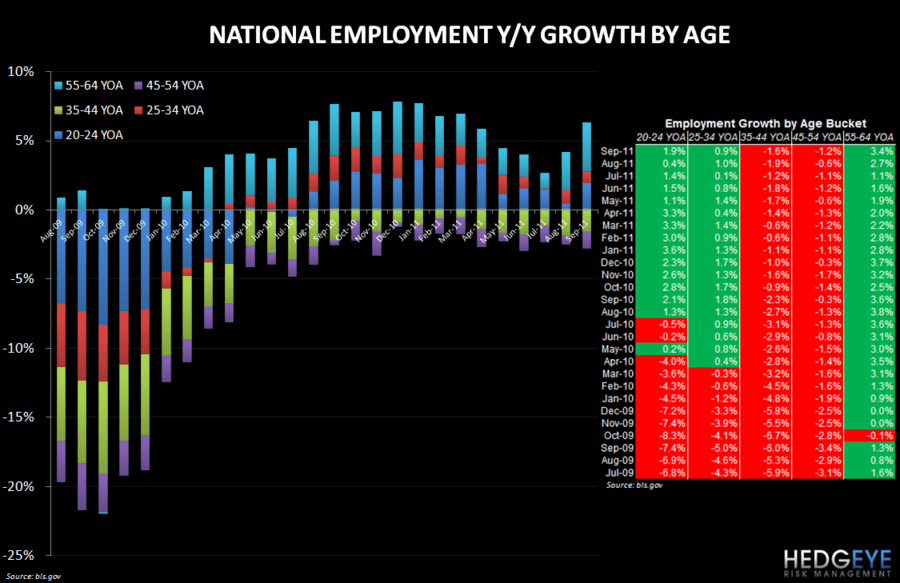

More specifically for restaurants, employment growth by age cohort and also by the industry itself provides insight into the state of the industry. The employment-by-age data is, on the margin, positive for both quick service and casual dining. For 20-24 year-olds, employment growth in September accelerated to 1.9% versus last year from +0.4% in August. This is a positive data point for quick service given that this cohort is a frequent customer for the category. For casual dining, 55-64 year-olds saw employment growth accelerated to +3.4% in September from +2.7% the month prior.

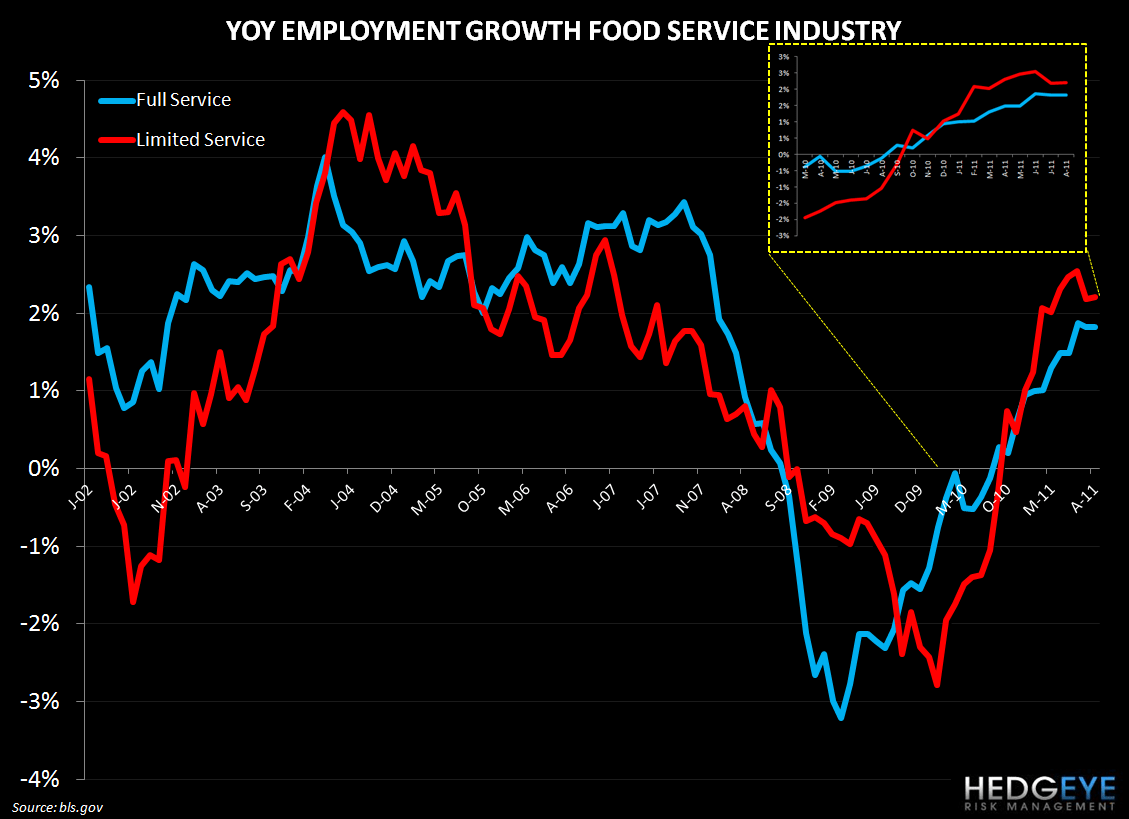

Hiring within the restaurant industry was less bullish in August (this data series is released on a lag). Year-over-year growth in limited service hiring picked up in August while hiring in full service was flat. We will continue to monitor this trend in the coming months. Within the payroll data, payrolls in “food services and drinking places” increased by 12k in September following a similar sequential increase in August. Considering the payrolls data, the lagging industry specific data, shown in the chart below, when it is released for August may show an improvement for September. We remain more positive on casual dining than quick service.

Howard Penney

Managing Director

Rory Green

Analyst

hiring by limited service restaurants and full service restaurants were