THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - October 7, 2011

Short Covering Opportunities are what they are – we had a big one this week. Now it’s time to manage the downside risk again. Whispers were bountiful yesterday about a better than “expected” unemployment report. That will surprise me if it comes to fruition. From these levels in macro markets, that’s now a liability for the bulls if it doesn’t. The Hedgeye S&P model is looking for jobless claims to re-accelerate in the coming weeks to 465,000-475,000 range.

As we look at today’s set up for the S&P 500, the range is 27 points or -1.71% downside to 1145 and 0.60% upside to 1172.

SECTOR AND GLOBAL PERFORMANCE

Three days and +5.9% higher than the YTD closing low (1099), once again, the shorts have been squeezed.

But will there be follow through?

Tomorrow we have a Game Time catalyst with the employment report and there’s a gaping hole down to 1101 support, so stay tuned…

Nothing has really changed in the Sector Risk model other than seeing a continued (and healthy) rotation toward sectors that I think would benefit most from a Strong US Dollar (Consumer Discretionary and Technology – both are now bullish on our immediate-term TRADE duration).

Deflating The Inflation is good for consumption

The only sector that remains bullish from an intermediate-term TREND perspective is Utilities (XLU) and we are long that.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +2132 (+705)

- VOLUME: NYSE 1117.43 (-6.45%)

- VIX: 36.27 -4.07% YTD PERFORMANCE: +104.34%

- SPX PUT/CALL RATIO: 1.70 from 1.91 (-11.08%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 38.78

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.01 from 1.92

- YIELD CURVE: 1.72 from 1.67

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 a.m.: Non-farm payrolls, est. 55k, prior 0k

- 9:30 a.m.: Fed’s Fisher speaks on U.S. economy in Dallas

- 10 a.m.: Wholesale inventories, est. 0.6%, prior 0.8%

- 10:45 a.m.: Fed’s Lockhart speaks on economy in Atlanta

- 1 p.m.: Baker Hughes rig count

- 3 p.m.: Consumer credit, est. $8b, prior $11.965b

WHAT TO WATCH:

- Employment in U.S. probably gained 55k last month, economists estimate, not enough to bring down unemployment rate of 9.1%.

- U.K. bank ratings cut by Moody’s after agency concluded government less likely to provide support.

- Global investors like Mitt Romney better than any other U.S. presidential candidate, though cool to Republican field in general

- President Obama hosts Prime Minister of Tunisia Beji Caid Essebsi

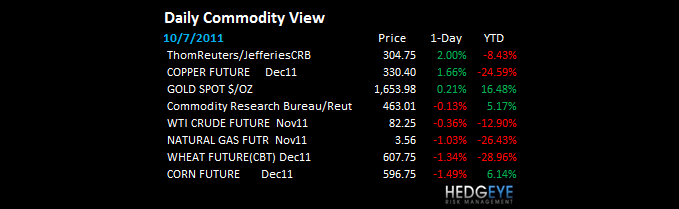

COMMODITY/GROWTH EXPECTATION

COPPER – nice rally for the Doctor but, like Asian Equities, it’s simply a short squeeze from immediate-term oversold lows. Most of the manic media was running Copper charts at the bottom last week, but we have been signaling Copper’s having broken its TREND since late-July early-August. That has not changed – TRADE and TREND lines of resistance for Copper now 3.44 and 4.18.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- China Baby-Formula Maker Buying Arsenic Debt Shows Trust Risks

- Copper Traders Turn Most Bullish in Six Weeks on China’s Demand

- Gazprom Extends Drought on Two-Year High Spread: Russia Credit

- Rio, Ivanhoe Halt Mongolian Bid to Raise Oyu Tolgoi Stake

- ‘Resilient’ Gold Set for Record Rally, Morgan Stanley Says

- Oil Set for First Weekly Gain in Three Before U.S. Jobs Report

- Gasoline Declining to Eight-Month Low on Economy: Energy Markets

- Gold Heads for First Weekly Increase in Five as Equities Rally

- Malaysia’s Export Growth Quickens on Higher Sales of Commodities

- Oil May Fall Next Week on European ‘Downside Risks,’ Survey Says

- Oil Trims First Weekly Advance in Three Before U.S. Jobs Report

- Worst Oil Industry Slump Since Lehman May Herald Takeovers

- Gold May Gain a Third Day on Economy Concern, Physical Purchases

- Palm Oil Set for Third Weekly Loss on Rising Malaysian Inventory

- Thai Rice Prices Unlikely to Remain High, Riceland’s Vichai Says

CURRENCIES

FX: EUR/USD bumping up against a wall of resistance 1.34-1.37

EURO – I re-shorted it yesterday into the close at my 1st line of immediate-term TRADE resistance (1.34); there is a wall of resistance overhead with the most impt line being the EUR broken TAIL of 1.39. My highest conviction Global Macro position remains long US Dollar.

EUROPEAN MARKETS

EUROPE: wet kleenex day across the board with no tangible bazooka timing - Belgian and Swiss stocks leading Europe lower (banks)

ASIAN MARKETS

ASIA – tail ends of the squeeze in every market that is still in crash mode (Hong Kong, Korea, Japan, etc) effectively failed at all of my immediate-term TRADE lines of resistance – for HK that’s 18,728; KOSPI 1797; and Nikkei 8777.

MIDDLE EAST

Howard Penney

Managing Director