(Note: This post includes the industry SIGMA, which was not included previously - otherwise unchanged)

With the Q2 Retail earnings season now in the books, let’s revisit the industry’s financial health. Following our mid-earnings update, the 2H shaped up considerably different than the first. Results started off good overall and remained that way through the quarter. The notable change however, was the positive turn in sales/inventory trajectory.

After starting the quarter down -25% reflecting continued deterioration, the industry finished with a sales/inventory spread down only -11% marking the first quarter in the last five to show sequential improvement. The delta was driven primarily by footwear and sporting goods retailers (FL, FINL, DKS, HIBB, DSW, GCO) as well as a few notable apparel companies (GES, LTD, and ANF) that posted a positive sales/inventory spread reflecting cleaner inventory levels in the athletic channel relative to the industry more so than stronger top-line growth.

This doesn’t change the fact that the consolidated SIGMA for the apparel/footwear supply chain remains squarely in the lower left quadrant with inventory growth outpacing sales growth and margins contracting. To some extent, it’s needed for the industry to catch up on 3+ years of unsustainably low inventory levels. But the fact remains that Gross Margins are near peak for the space. Also, we’re facing a dynamic where the better companies ordered 10% fewer units and have realized close to 10% higher prices. Coupled with a sharp decline in cotton prices, we think there’s a high likelihood of a false sense of security across the industry that will compel companies to order up for next season – not good.

Shorts: JCP, UA, HBI, SHLD

Longs: LIZ, NKE, RL, TGT

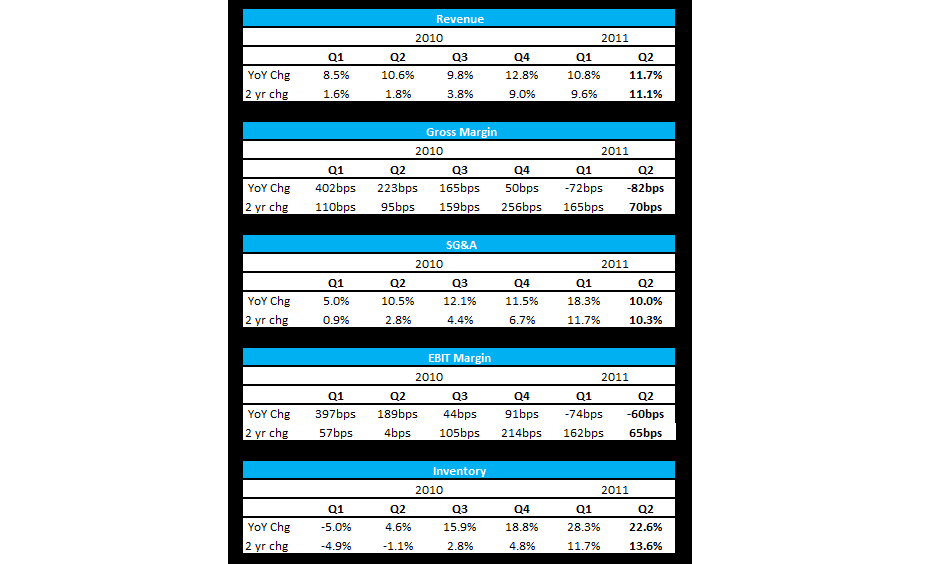

The sales trajectory setup for the space is unchanged, Q1 through Q3 of last year grew steadily between 8-10%, but then in the three quarters since, we have seen a definite step-up. While the yy change has only been by roughly 200bps, the underlying 2-Yr trend has increased from sub 2% to 4% in Q3 last year before jumping up to 9-11% over each of the last three quarters. This would be less concerning if inventories were tight and margin compares easy, but that’s not the case.

Not surprisingly, with sales slowing and margins tightening, we’ve seen the industry shift from the top-left quadrant where 52% of the industry was this time last year (sales/inv spread positive margins expanding), to the lower left quadrant otherwise referred to as the “Danger Zone” where 37% of the industry players we track are now (negative sales/inv spread margins contracting). This move has still not been fully reflected in the stocks leaving an notable overhang on the industry. In addition, with Q3 earning season setting up to be the worst in worst in 2-years, we see further downside near-term for retail stocks. We’ll get the latest read on this reality when retailers report September sales tomorrow.