This note was originally published at 8am on September 29, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We will all sleep as I do, in the open.”

-Leonidas

At the end of chapter 22 of “Gates of Fire”, King Leonidas gives an epic speech to his officers about leadership.

“I am telling the Spartans what I tell you now. You are the commanders; your men will look to you and act as you do. Let no officer keep to himself or his brother officers, but circulate day long among his men. Let them see you and see you unafraid.”

Compare and contrast that sense of responsibility and selflessness versus the putrid lack of accountability we have to wake up to as modern day capitalism comes under left-leaning Keynesian assault:

“Monetary policy is not a panacea. There are certainly some areas where other policy makers could contribute.”

-Ben Bernanke (in a speech yesterday)

There is no legitimate leadership in this country’s economic policy making inasmuch as there is none in France or Italy this morning. Losers are pointing fingers and making excuses rather than bellying up to the bar like Red Sox GM Theo Epstein did last night:

“You can’t sugarcoat this. This is awful. We did it to ourselves and put ourselves in a position like this to end our season.”

The winners in this country who bleed red, white, and blue get accountability. Our academic and political policy makers, who have never had to meet a payroll in their life, do not.

Back to the Global Macro Grind…

In Monday’s Early Look I outlined this week’s calendar of Global Macro catalysts. The last 2 catalysts left for the Big Government Intervention “is the best path to long-term economic prosperity” club, were a vote for the Euro-TARP bailout in the Bundestag and month-end markups.

If the German vote was your catalyst to be long anything European or US Equities, that catalyst is now gone. What do you do now? Hope for another left-leaning central plan to suspend economic gravity? Or just say hey – this whole Keynesian thing “is not a panacea?”

Rather than lean on the losing side of this year’s Global Macro trade, it’s time to get back to winning again here this morning. From New Haven, Connecticut to St. Louis, Missouri, we’re issuing a friendly challenge to all of the winners of the 2011 game of Globally Interconnected Risk to unite.

First, let’s stick with this week’s game plan:

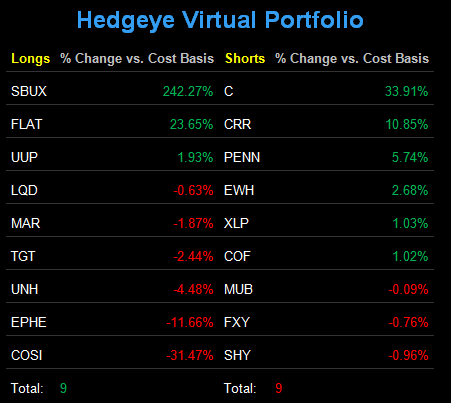

- Monday, I cut our asset allocation to US Equities to 0% again (sold Utilities, XLU)

- Monday, I cut our asset allocation to Commodities to 0% again (sold Gold, GLD)

- Tuesday, I moved the Hedgeye Portfolio back to net short (more shorts than longs)

This isn’t being “over-confident”, “uber bearish”, or whatever the losers and the haters out there want to call us. This is simply a reminder that we have a repeatable risk management process at this firm that has saved our clients and their clients a lot of money in both 2008 and 2011.

"Winning takes talent, to repeat takes character."

-John Wooden

Winning doesn’t require bailing out losers. It doesn’t require extending the short-selling ban like the French are doing again this morning either. Winning requires accountability, confidence, and trust. If people don’t trust you or your economic policy making process, you should be fired.

The SP500 is down -26.5% from the October 2007 high. It’s down -15.6% from the April 2011 lower-long-term high. This is called losing. And the best way to start winning again is to end whatever it is that these people keep doing to our markets, over and over and over, again.

No more whispers, rumors, and squirreling around in the shadows of this fiat system. No more bailout money printing as the elixir of short-term political life. Stop.

“I want to see shields flashing like mirrors, for this sight strikes terror into the enemy” (Leonidas in Gates of Fire, page 226). Give me transparency, or give me a place of American mediocrity where I can sleep in.

My support and resistance ranges for Gold, Oil, the German DAX, and the SP500 are now $1567-1667, $77.91-83.69, 5449-5741, and 1113-1171, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer