No change to September revenue forecast of HK$20-22BN.

Despite investor fears of a slowdown, Macau had another outstanding week and remains on pace to hit the midpoint of our previous HK$20-22 billion estimate for the full month of September. Average daily table revenue of HK$689 million this past week was almost exactly in-line with the prior week and slightly above the month to date average of HK$686 million. Our full month projection assumes a slowdown in the last 4 days of the month which is typical heading into Golden Week.

Golden Week, from Oct 1st thru Oct 9th, should be the busiest period of the year. We are hearing that hotel rooms are fully booked and that the Junkets and Promoters are geared up for a record holiday.

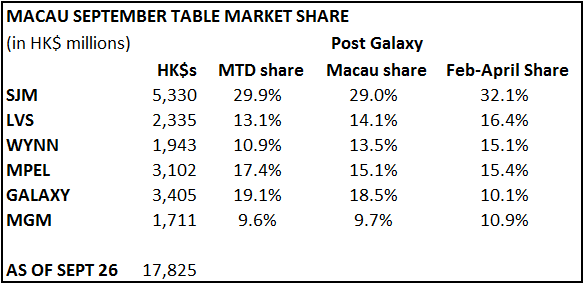

In terms of market share, as expected, Wynn continues to recover from low hold experienced earlier in the month and MPEL’s share moderated from record highs. However, MPEL is trending well ahead of trend and remains on track for a blockbuster quarter. Galaxy looks like it hit a homerun on the luck side this past week as its MTD share went from 16.3% last week all the way up to 19.1%.