THE HEDGEYE BREAKFAST MENU

Notable macro data points, news items, and price action pertaining to the restaurant space.

MACRO NOTES

The latest ICSC index fell 0.2%. We now have been in a downward trend that has been occurring since late July. Consumers have not stopped spending, but growth remains only modest.

Alcohol not a panacea for all restaurants - NYT.

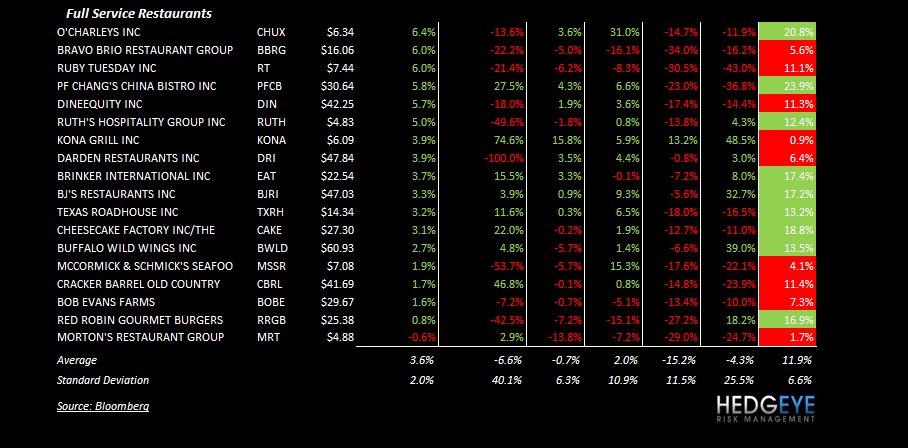

SUB-SECTOR PERFORMANCE

Sanderson Farms added to Conviction Buy List at Goldman Sachs

QUICK SERVICE

MCD - is reprising its popular traffic-driving Monopoly Game promotion beginning Tuesday at its nearly 14,000 U.S. restaurants - stop on by your local arches and purchase any of the following menu items:

- Medium Fountain Drinks (2 pieces)

- McCafe Smoothies (2 pieces)

- Hash Browns (2 pieces)

- Big Mac® (4 pieces)

- 10-piece Chicken McNuggets (2 pieces)

- Egg McMuffin (2 pieces)

- Oatmeal (2 pieces)

- Filet-O-Fish (2 pieces)

- 20-piece Chicken McNuggets (4 pieces)

- Large Fries (4 pieces)

According to GRUBGRADE this is the best time of year to buy Hash Browns, as they remain the cheapest way to collect game pieces. The contest will run through October 24th.

DPZ and JACK at the Telsey conference today

FULL SERVICE

DRI - Reports EPS tomorrow

PF Chang's announces departure of COO Richard Tasman at the end of FY11

Howard Penney

Managing Director

Rory Green

Analyst