THE HEDGEYE BREAKFAST MENU

Notable macro data points, news items, and price action pertaining to the restaurant space.

MACRO NOTES

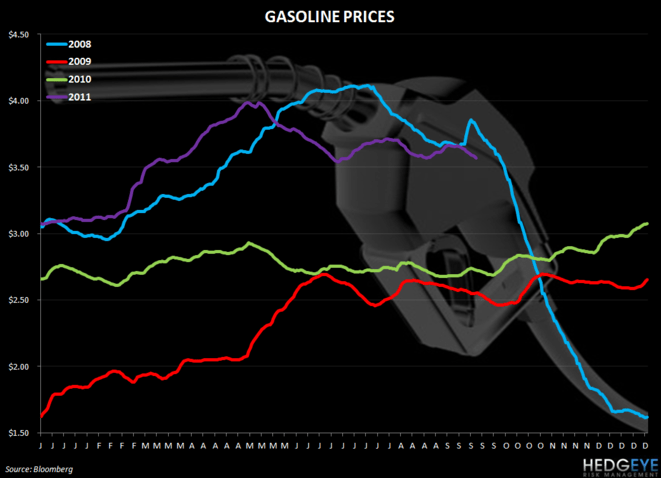

Growing concern over a Greek debt default combined with signs of weakness in China and further erosion in the U.S. economy triggered steep declines in worldwide stocks and commodities (ranging from oil to gold to grains). I know its 2011 and not 2008, but the chart on gas prices is haunting me; gasoline prices continue to shadow the trend of 2008.

SUB-SECTOR PERFORMANCE

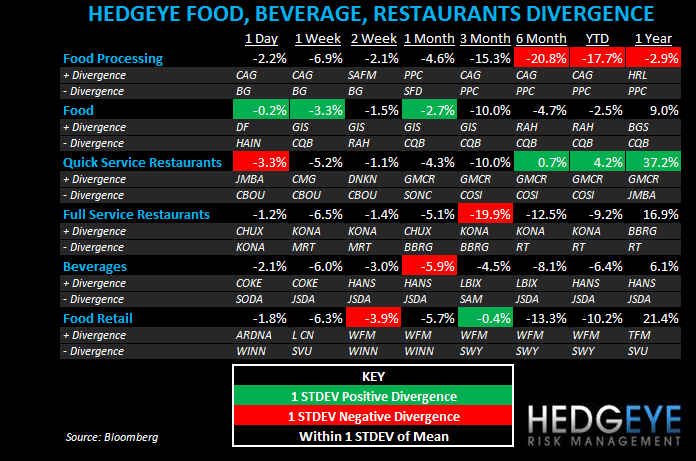

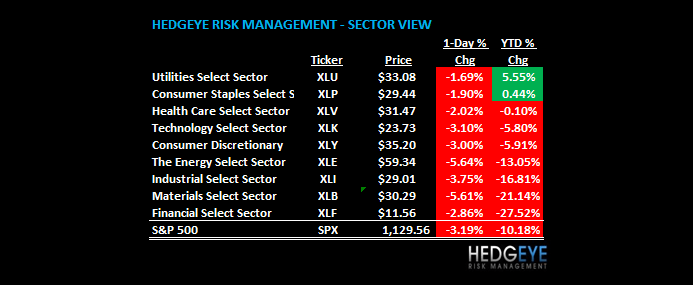

Yesterday, food stocks were the safe-haven of choice and QSR underperformed. As of the close yesterday, Utilities (XLU) and Consumer Staples (XLP) were the only two S&P sectors that were still showing positive performance year-to-date. The XLU is positive on both TADE and TREND.

QUICK SERVICE

DPZ - announced that after just three months since its launch, the new Domino's App for iPhone and iPod touch has achieved $1 million in sales over a single week. The Domino's App also speedily achieved $1 million in total sales – just 28 days after launch. With the app initially available on June 8 and announced to the public one week later, Domino's met both milestones much quicker than it expected.

YUM - agreed to sell Long John Silver's Inc. and A&W Restaurants Inc - "As we continue to sharpen our long-term growth focus on international expansion and improving our U.S. brand positions in KFC, Pizza Hut and Taco Bell, Long John Silver's and A&W no longer fit our long-term growth strategy," said David Novak, Yum chairman and chief executive, in a statement. LJS Partners LLC will buy Long John Silver's and A Great American Brand LLC will buy A&W Restaurants for undisclosed sums.

ARCO - The following is from Hedgeye’s Moshe Silver daily BRAZIL NOTES - In Brazil worker wages highest since 2002 – government statistical office IBGE reports 6% unemployment in August in the six major metropolitan areas surveyed, the same level as in July, and the lowest August reading since the series was initiated in 2002. Actual wages in August were R$ 1,629.40, the highest level in the history of the survey. August’s reading was up 0.5% from July and up 3.2% YoY. The survey also found an increase in documented workers and a decline in the informal sector. The director of the IBGE labor and wage section said the increase in documented workers contributes directly to a higher level of wages overall.

MCD Japan - is looking to close hundreds of “small” restaurants next year in an on going effort to boost profitability. SSS have started to increase in September following the end of limits on electric power usage set by utilities after the March 11 earthquake and tsunami crippled some power plants.

MCD - boosts dividend by 15% - Yield now 3.2%

MCD/YUM rated new outperform at Raymond James

<chart4>

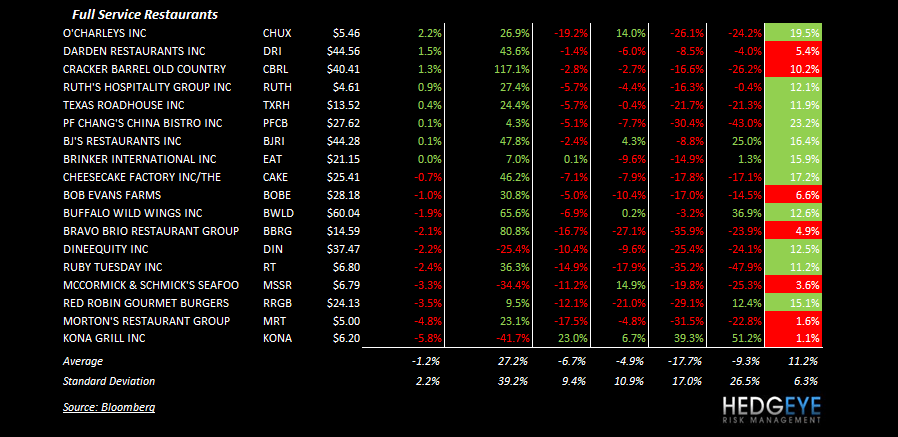

FULL SERVICE

DRI - annual meeting was very bullish from a Hedgeye TAIL perspective. In the short run, the Olive Garden/Red Lobster is still the perceived as the choice of an aging demographic. Could be the reason why the company is so keen on making an acquisition.

KONA - has closed its underperforming restaurant in Sugar Land, Texas.

CBRL - adopts shareholder rights plan with qualifying offer exception; rights plan will have three-year term subject to shareholder approval at 2011 annual meeting and does not apply to all-cash, fully-financed tender offers open for 60 business days

Howard Penney

Managing Director

Rory Green

Analyst