“I’m just saying, just let it flow, man.”

-Ray Dalio

I think I have milked both the quotes from Ray Dalio’s New Yorker interview and this week’s short squeeze in Global Equities bone dry. While there has been plenty of emotion embedded in this week’s 100 point S&P futures rally, it’s just time to “let it flow”, Bro.

“Bro” is a very sophisticated nickname that Wall Street trader types use when addressing each-other. Examples would be: “Bro, that was a monsta print, bro…” or “Bro, the two-hundo is still broken – this rally doesn’t make sense, bro.”

Both in the Bro Brotherhood and beyond, this week’s +9% rally in the S&P futures (from Monday’s pre-open low to yesterday’s intraday high) has left a mark. Not surprisingly, you’re seeing the commensurate hedge fund blowups that are associated with price volatility. The Goldman Beta Fund shutdown is a Top 3 story on Bloomberg this morning. Yesterday it was the Euro Bro at UBS.

Bull markets generally don’t blow up the Bros. Volatility does. And as a profession we have a lot of work to do in order to evolve the risk management process so that our clients are actually getting the protection we market to them.

Bridgewater’s Ray Dalio doesn’t blow up. To the contrary, his $100 Billion Dollar hedge fund capitalizes on other people blowing up. In the same New Yorker interview (“Ray Dalio’s Richest and Strangest Hedge Fund”, by John Cassidy, July 25, 2011) Dalio explains how emotion has no place on his team – or he, at a minimum, needs a way to govern it:

“What we’re trying to have is a place where there are no ego barriers, no emotional reactions to mistakes… if we could eliminate all of those reactions, we’d learn so much faster.”

Re-think. Re-work. Re-learn.

That’s what getting good at this Globally Interconnected Game of Risk is all about - not pointing fingers, fighting change, and/or Mr. Macro Market’s leading indicators.

Back to the Global Macro Grind…

Not surprisingly, after prices have moved higher across the Global Equities universe, my price, volume, and volatility factors look a heck of a lot better than they did last Friday.

Let’s look at those core 3 factors in the SP500 for example:

- PRICE – what was immediate-term TRADE resistance at 1178 is now support

- VOLATILITY (VIX) – what was immediate-term TRADE support at 35.47 is now resistance

- VOLUME – remains less than dead in the water on the up moves with Wednesday’s volume signal being +9% above average

Now to be crystal clear on reading these factors, they are on 1 duration (the immediate-term TRADE), not all 3 (TRADE, TREND, and TAIL). From a long-term TAIL perspective, resistance for the SP500 remains up at 1265. In other words, all of the “long-term” investors out there should still be concerned about the long-term.

The hallmark of my risk management process is to be:

A) Multi-Factor

B) Multi-Duration

What that means (and I think Dalio would agree with this) is that you can heighten the probability of 1. not missing something big or 2. being overly exposed to one big thing, if you are analyzing multiple-factors (Countries, Currencies, Commodities, etc.) across multiple-durations.

So, if we broaden the immediate-term TRADE signals to Europe this morning, here’s what I see (and it’s not good):

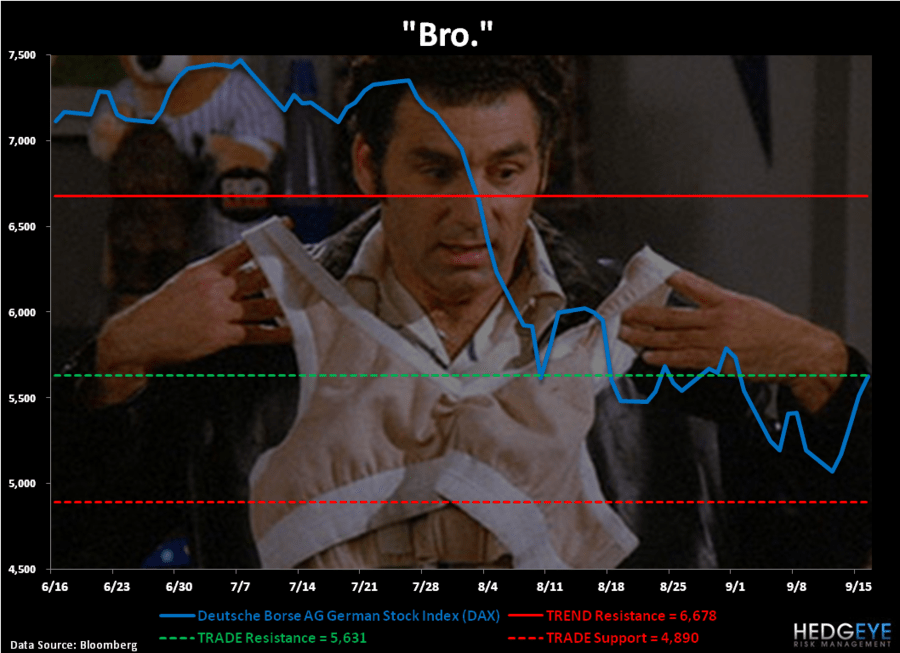

- Germany’s DAX failing to overcome immediate-term TRADE resistance of 5631

- Italy’s MIB Index failing to overcome immediate-term TRADE resistance of 15,014

- Spain’s IBEX failing to overcome immediate-term TRADE resistance of 8437

Bear markets get immediate-term TRADE oversold. Then they bounce. We get that. That’s why we’ve made 2 calls in Q3 of 2011 (August 8thand Monday, September 12th) titled “Short Covering Opportunity.” And yes, these “calls” have time stamps.

Old Wall Street’s Sell-Side or the pop-media that provides it a marketing platform doesn’t really do the time stamp thing. We don’t champion time stamps to rub it in their face. We are explicitly challenging them to be transparent so that we can figure out if they can be additive to the collective risk management process that this industry needs.

Letting $2 Billion Dollar losses in the UBS bonus pool “flow” or blowing clients out of “risk managed” hedge fund products at every capitulation bottom we’ve had in the 2008-2011 period isn’t cool anymore, Bro.

My immediate-term support and resistance ranges for Gold (which just broke its immediate-term TRADE line of $1817 and has no TREND support to $1630), Oil, and the SP500 are now $1, $86.54-90.26, and 1178-1212, respectively.

Best of luck out there today and enjoy your weekend with your families,

KM

Keith R. McCullough

Chief Executive Officer