This note was originally published at 8am on September 07, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Historically, the claim of consensus has been the first refuge of scoundrels; it is a way to avoid debate by claiming that the matter is already settled.”

-Michael Crichton

In financial markets, consensus is typically what astute stock market operators invest against. That is, if the crowd has a similar view of an asset or asset class, that asset or asset class will typically be priced to perfection. Therefore, savvy analysts and portfolio managers strive to find the nugget of non-insider information that will prove that consensus is wrong, which inevitably leads to a re-pricing of the asset and profits for those that appropriately determined where consensus views were wrong.

Obviously, the key variant macroeconomic view that Hedgeye held coming into 2011 versus consensus was that growth was slowing and would continue to slow. We won’t rehash the thesis, but our view was for sub 1.5% growth in the first two quarters of 2011, while sell side consensus GDP estimates were, based on Bloomberg data, at +3.4% as of early February.

As always, though, the job is to play the game in front of us and while rehashing old victories can be fun, we’ll save those opportunities after the inevitable victories of Yale over Harvard at the Yale / Harvard hockey and football games this year. So two questions to ask into the remainder of the trading year are:

1) What is consensus?

2) What are your best variant views versus consensus?

Yesterday, I noticed a nugget of information that at first suggested to me that market consensus was leaning too far to the negative. Specifically, negative bets on the SP500, as measured by a net outstanding 107,913 futures contract in the week August 30th, were at their highest level since September 2007. My knee jerk reaction, as it relates to determining consensus, was to look at this statistic as a contrarian indicator. History, of course, suggests a different byline.

In fact, as noted above, the last time negative options bets were at this level was September 2007. The next month, October 2007, marked the all time high in the SP500. There are number of studies that provide an explanation as to why this seemingly contrarian indicator is actually not one, but the primary reason is that short sellers, in aggregate, typically invest with better information than market participants broadly. One recent study by Morningstar CMPS on Canadian stocks from 2003 to 2011 showed the following:

“CPMS looked back to 2003 (when it started to record short interest data) and found that a portfolio of the most heavily shorted stocks indeed did poorly and underperformed the S&P/TSX composite total return index by about six percentage points annually, assuming an equal weighting of each of the 15 names and reselecting new names each month.”

Thus, while consensus views are important to determine when contemplating the risk / reward of positions, always be aware of The Scoundrels of Consensus. These critters come in many forms, such as in the form of those who practice the dark art of short selling or even, gasp, in the form of statements from senior executives or government officials.

Typically, of course, I would give little credence to the idea that either government officials or senior company executives have much insight into the global macro environment, or that they would truthfully share their views. At times, though, I do recommend taking the words of The Scoundrels of Consensus at fair value. Some recent statements from European “leaders”, which I’ve outlined below, exemplify this point. To wit:

1. “Under the current structure and with the current membership, the euro does not work. Either the current structure will have to change, or the current membership will have to change.”

- Stephanie Deo, Paul Donovan, and Jacek Rostowski of UBS Bank

2. “The Euro has never had the infrastructure it requires.”

- Herman Van Rompuy, EU President

3. “I regard the huge buy-up of bonds of individual states of the ECB as legally and politically questionable.”

- Christian Wulff, German President

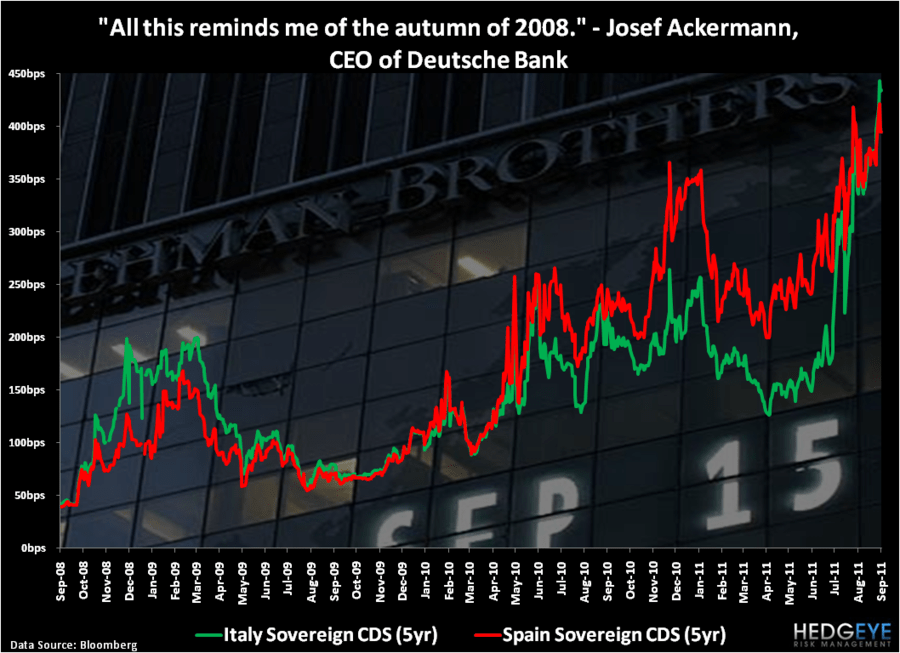

4. “All this reminds one of the autumn of 2008.”

- Josef Ackerman, Deutsche Bank CEO

5. “Dealing with a banking crisis was difficult enough, but at least there were public sector balance sheets on to which the problems could be moved. Once you move into sovereign debt, there is no answer; there’s no backstop.”

- Mervyn King, Governor of the Bank of England

6. “The euro is in danger . . . if we can’t deal with this danger, then the consequences for us in Europe are incalculable.”

- Angela Merkel, Chancellor of Germany

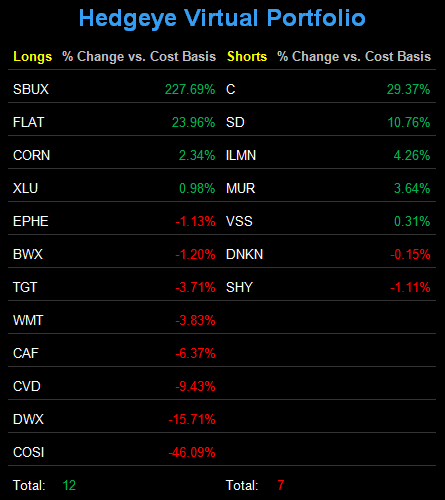

The intention this morning is not to fear monger our subscribers into getting overly negative in the short term. In fact, our most recent moves in the Virtual Portfolio yesterday morning were to cover two shorts : United Kingdom Equities (EWU) and Capital One Financial (COF).

Instead the advice this morning is simply this: be aware and wary of The Scoundrels of Consensus.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research