This note was originally published at 8am on September 06, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Where is the edge? And how do I stay the right distance from the edge?”

-Ray Dalio

That was Ray Dalio’s answer on the key to risk management success (“Mastering The Machine”, by John Cassidy, New Yorker, July 25th 2011). Like he did in 2008, Dalio is beating most of his hedge fund competition in 2011. Hedgeye calls that a repeatable process.

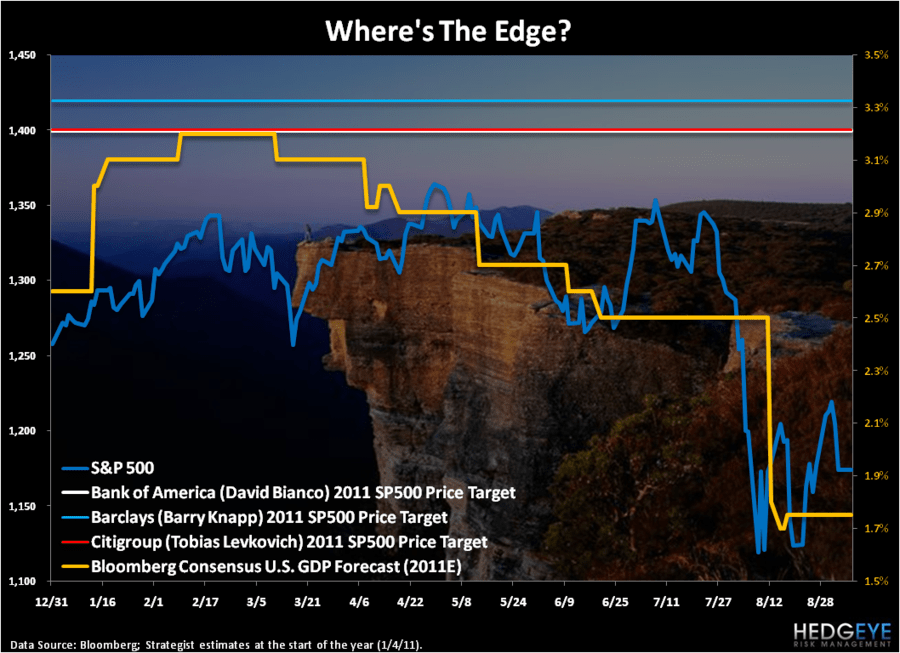

Where was The Edge in 2011? Global Growth Slowing. Period.

While there will be plenty of storytelling and finger pointing about how it was a pig in Europe or a politician in America, that’s pretty much it. If you got Growth Slowing right, you got a lot of other things right.

Growth won’t slow forever. But it didn’t stop slowing in the US on Friday and it doesn’t appear to be slowing in Europe this week either. When growth stops slowing, that will be a critical signal to start thinking about going the other way.

The cover of Barron’s this weekend asked “Where Do We Go From Here?” Good question. But for the answers, Barrons (like many other legacy financials media outlets) continues to use the wrong sources. Why many of these journalists are using the same sources that missed Growth Slowing in 2008 is not clear. Why they don’t use Hedgeye is simple: we are their new competition.

In my Early Look note from August 11thtitled Forecasting Dark (“Weather forecast for tonight: dark.”-George Carlin) I highlighted what Washington/Wall Street continue to use as their source for “blue chip” strategy. At the beginning of 2011 here were some of the higher profile estimates:

Forecasts for 2011 US GDP Growth:

- Bank of America = 3.2%

- Barclays = 3.1%

- Citigroup = 3.1%

Forecasts for 2011 SP500 Returns:

- Bank of America (David Bianco) = 1400 (up +11.4%)

- Barclays (Barry Knapp) = 1420 (up +13.0%)

- Citigroup (Tobias Levkovich) = 1400 (up +11.4%)

As of last week’s train wreck US unemployment report and another -31% estimate cut from the US Government on Q2 2011 GDP, here’s fact versus prior fictions:

- Q1 2011 US GDP Growth = 0.36%

- Q2 2011 US GDP Growth = 0.98%

- SP500 YTD Return = -6.7%

Now, to be fair, there are still some very contrarian views out there. Consider ISI Group’s latest sell-side hire, Bijal Shah, who proclaimed in Barron’s on August 22, 2011, “higher unemployment isn’t necessarily terrible news for equity markets.”

It just was last week.

So (drumroll), after seeing the data, here are your real-time Wall Street revisions from Barron’s this weekend:

- Deutsche Bank (Binky Chada) drops their January 2011 year-end SP500 target from 1550 to 1425

- Goldman Sachs (David Kostin) drops their January 2011 year-end SP500 target from 1450 to 1400

- Credit Suisse (Doug Cliggott) drops their January 2011 year-end SP500 target from 1250 to 1100

Whoa, hold your horses! Is that one major sell-side firm with a price target below the market’s last price? Indeed. This isn’t Doug Cliggott’s first rodeo getting a bearish move right.

So what do we do with all of this incompetence in forecasting?

- Realize that the sell-side hasn’t capitulated yet and cut their estimates to the right level (they will at the bottom)

- Accept that both the US Government and their economic advisors (the sell-side) continues to use the wrong models

- Keep doing what it is that we’ve done to call both the 2008 and 2011 Growth Slowdowns

Not that I’m still keeping track, but on February 3rd, 2011, JP Morgan’s Thomas Lee put out a note titled “Circle of Life”, raising his 2011 EPS target in the SP500 to $97.50 from $94 saying that it “smells like a secular bull market…”

While I’m not certain how to use the scratch-and-sniff model, what we can be certain of is that most of these sell-side strategists quickly revert to calling markets “cheap” when both their earnings and price targets are wrong.

Of course, anything can be deemed “cheap” if you use the wrong growth and earnings estimates…

Who has the right earnings estimates? You can drive a truck through Deutsche Bank and Credit Suisse views on the “E” in PE for 2012:

- Binky Chada says $106

- Doug Cliggott says $81

So, Chada will call the SP500 “cheap” because he is using 11x earnings (1173/$106) and Cliggott will call it more expensive at 14x (1173/$81). Who is right? What’s the right multiple? Who has The Edge?

Don’t worry, those are not the risk management question you need to answer this morning. The answer that you have to perpetually impute is “how do you stay the right distance from the edge.”

To do that, you’ll need a repeatable risk management process as well.

My immediate-term support and resistance levels for Gold, Oil, and the SP500 are now $1818-1903 (bullish but overbought), $83.87-97.34 (bearish), and 1145-1193, respectively. Europe capitulated yesterday. There’s a good chance another immediate-term low in US stocks comes at a higher-low than the prior closing low (1119) and US Treasuries are putting in immediate-term highs.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer