Notable macro data points, news items, and price action pertaining to the restaurant space.

MACRO

Consumer

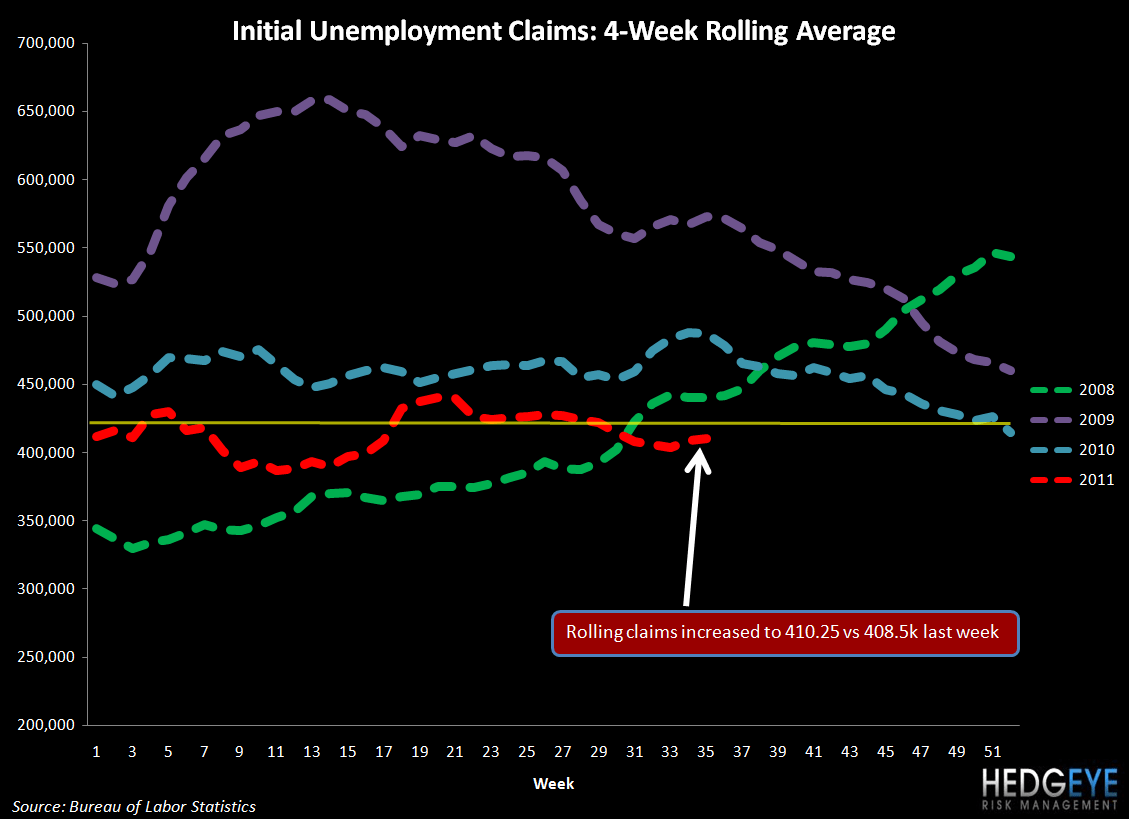

Initial jobless claims came in at 409,000 for the week ended 8/27, a decrease of 12,000 from the week prior at 421,000 (revised). The four-week rolling average ticked up by 1,750 to 410,250, as the chart below illustrates.

Costs

Farm product prices received by farmers rose 1.1% in August. The increase in the overall index is driven by strength in crop and livestock prices; the overall index is 29% higher than a year ago. The recent flood/drought inflicted damages to domestic crop ensure food price inflation will continue well into 2012.

Subsectors

Food retailers have taken the lantern of performance. Food processors continue to perform sluggishly.

QUICK SERVICE

COSI CEO James Hyatt is leaving “for personal reasons”.

WEN CEO Roland Smith is stepping down from his role as President and CEO but will serve as a Senior Advisor to the Company during a transition period with newly announced President and CEO Emil Brolick (effective 9/12).

WEN’s new burgers are being rolled out. A post on grubgrade.com describes two new choices of the D.T. Double. In addition to “The Original”, the newcomers are the “Spicy Chipotle” and the “Garlic Steakhouse”. The Original D.T Double has American cheese and a “signature sauce”. The Spicy Chipotle D.T. Double includes pepper jack cheese and fiery chipotle sauce. The Garlic Steakhouse D.T. Double has Monterey Jack cheese and garlic aioli sauce. These double cheeseburgers are all priced at $2.99.

SONC continues to underperform on multiple durations and did so yesterday on higher volume studies. I’m not a believer that hot dogs are going to keep momentum going for ever - but the company continues to introduce new products. Sonic is adding on to its 100% all-beef hot dog line again this fall, introducing two new hot dogs in the form of the Bacon & Blue Dog and the Kickin’ Coney. Here’s a little more information: Bacon and Blue Dog: It’s a hot dog made with 100% pure beef, covered in crisp bacon, fresh lettuce, ripe tomato and blue cheese dressing on a poppy seed bun (450 Calories, 27 grams fat, 9 grams sat. fat, 17 grams protein.) Kickin’ Coney: A hot dog made with 100% pure beef and topped with chili, cheddar cheese, crispy onions and chipotle BBQ sauce (480 calories, 27 grams fat, 11 grams sat fat, 19 grams protein)

BKC has brought to the U.S. the multi-person meal platform it has been offering in Australia. Coupons distributed nationally this week include one for a $6.99 Meal for Two combo and another for a $9.99 Family Bundlecombo.

CASUAL DINING

New Bennigan’s Franchising Co. chief executive Paul Mangiamele says he’s upbeat on the 80-unit chain’s performance after a successful reboot this summer at Bennigan’s corporate restaurant in Chicago. Same-store sales increases at the flagship unit are running in the low double digits, said Mangiamele, who took over as chief executive in May. Same-store sales for the rest of the system are in the low single digits. – NRN

Howard Penney

Managing Director

Rory Green

Analyst