This note was originally published at 8am on August 24, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“If you must play, decide upon three things at the start: the rules of the game, the stakes, and the quitting time.”

-Chinese Proverb

While it’s both sad and pathetic to watch our said “free market” system come to this, the entire asset management world is being dared to bet on either black or red going into Ben Bernanke’s “event” in Jackson Hole, Wyoming on Friday.

If you must play (going to 70% Cash this week, we have decided not to), you should have already decided on 3 things:

1. RULES: seeing that Japan, Europe, and the US effectively change the rules as we go, this is a tough one! If you have inside information on what Bernanke is going to say, enjoy that and some orange jump suit risk out on your life’s tail.

2. STAKES:

A) bet BLACK on Bernanke and the elixir of another short-term stock market inflation is yours

B) bet RED on no QG3 (Quantitative Guessing III) and there’s a high probability that your P&L doesn’t blow up in 2011

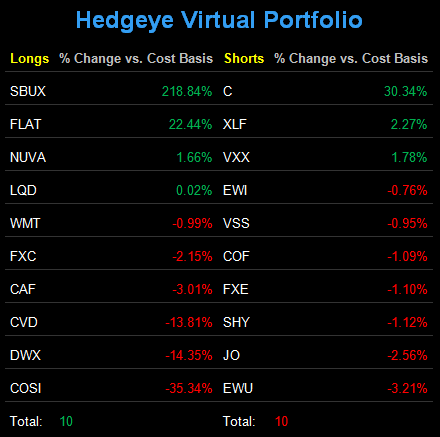

3. QUITTING TIME: don’t bet at all – go to cash and/or tighten up your net exposure like we have (10 LONGS, 10 SHORTS)

I’m not a big fan of blowing up. When I started in the hedge fund business, my first 3 years (2000, 2001, and 2002) were down markets. Not losing money was the name of the game. Since 2008, I haven’t had other people’s money on the pass-line (betting rules are different when the money isn’t yours). I’ve been “all-in” with my own money. Not interested in rolling the bones, Benny – sorry, “bro.”

This is what the ZERO Percent Interest Rate Policy has done to this gargantuan game of Globally Interconnected Risk. Big Government Intervention is designed to debauch your currency and dare you to bet on the stock market. That’s a dumb long-term strategy. Period.

In the past, we’ve also called this 3D-Risk – ZERO percent cost of “risk free” capital does 3 things:

- DARES investors to chase “yield” (stocks over zero percent “risk free” bonds)

- DISGUISES financial risk (think Bank of America’s net interest margins and liquidity gap – both in big trouble)

- DELAYS balance sheet restructuring (uh, got some Greek or Italian banking sausage?)

So… for me at least, the next 3 days will remain The Quitting Time – and I’m totally cool with that. Call me whatever you want to call me in the meantime. It took me a long time and a lot of mistakes to come to grips with this, but doing nothing with my hard earned capital is sometimes the best decision to make.

Back to the Global Macro Grind…

On this day in 2006, the planet Pluto was downgraded by the powers that be in Astronomy to “dwarf planet.” While I’m not an astrology expert, I think that math and physics had something to do with the downgrade. Fancy that.

Shockingly, 5 years later, Japan is getting downgraded this morning from land of Keynesian Nod to something less than getting the nod. On the “news” that Japan is an economic disaster, the Nikkei crashed again (down -20.4% since February 2011) for the umpteenth time since Paul Krugman and the Princeton boys told the Japanese to “PRINT LOTS OF MONEY.”

Nice.

But have no fear, the aliens are here…

On Fareed Zakaria’s GPS a few weeks ago, CNN teased that they were going to “explore the most important topic (the economy) with the most important voices” (Zakaria was interviewing Krugman). And I couldn’t make this up if it tried, but the venerable Keynesian of Nobel’s Social Study Experiment said:

“If we discovered that, you know, space aliens were planning to attack and we needed a massive buildup to counter the space alien threat and really inflation and budget deficits took secondary place to that, this slump would be over in 18 months…”

You know, space aliens, Ben… We need to be thinking cowboys and space aliens down there in Jackson Hole!

God help us. The Quitting Time with failed Keynesian policies is here.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1809-1901, $81.28-89.28, and 1108-1165, respectively. Yesterday was just another Japanese-like rally to lower long-term highs in US Equities. If people are seriously betting on Bernanke BLACK on Friday, I’ll tell you that this Canadian is in Cash and won’t be surprised whatsoever to see those expectations crash.

Best of luck out there today and a special prayer goes out to my brother Ryan and his beautiful family,

KM

Keith R. McCullough

Chief Executive Officer